Demat Account Types in India: Choose, Open & Manage Yours

Handling your shares shouldn’t feel complicated, yet many investors get confused by all the options available. The truth is, choosing the right Demat account can make your life much easier, letting you manage your securities smoothly and securely.

That’s why understanding the different Demat account types is so important; each type is designed for different needs, and picking the right one can save you time, effort, and hassle.

In this blog, we’ll walk you through what a Demat account is, why it’s important, and the types you can choose from. You’ll also get a simple step-by-step guide to opening a Demat account in India, tips on common mistakes to avoid, and practical advice on managing your account smoothly so you always stay in control.

Let’s get into it!

Overview

Demat accounts hold your shares and securities in digital form, making management safe and convenient.

There are four main types: Regular, BSDA, Repatriable, and Non-Repatriable, each suited to different needs.

Keep KYC updated, monitor your account, and maintain transaction records for smooth account management.

Avoid common mistakes like confusing Demat with trading accounts or choosing a DP only for “free” offers.

What Is a Demat Account?

A Demat account, or dematerialized account, is where you hold all your shares, bonds, and other securities in digital form instead of keeping physical certificates. It makes managing and transferring them much easier and safer. With a Demat account, you can see and handle all your securities in one place without any hassle. It’s the simplest way to keep your shares organized in India.

Now, let’s explore why having one is essential for managing your securities effectively.

Importance of Having a Demat Account

A Demat account makes managing your shares simple, secure, and convenient. Here are the key benefits you should know:

Safe and Secure Storage: Your shares are held in digital form, protecting them from loss, theft, or damage that can happen with physical certificates.

Effortless Transfer of Shares: Transferring shares, whether selling or gifting, is quick and easy, requiring minimal paperwork.

Quick and Convenient Access: You can view your entire portfolio in one place, making it simple to monitor and manage your holdings.

Streamlined Corporate Benefits: Dividends, bonuses, and rights issues are credited directly to your account, saving you from following up with physical documents.

Easy Pledging for Loans: Shares in a Demat account can be pledged digitally, simplifying the loan process.

Cost and Time Savings: You save on stamp duty and handling charges, and transactions are settled faster, usually within a couple of days.

With the benefits of a Demat account clear, the next step is to look at the main types you can open and how each serves different purposes.

4 Different Types of Demat Accounts

In India, there are four main types of Demat accounts, each designed to suit different needs based on your residency, how you use your account, and the size of your holdings. Familiarity with these options makes it easier to choose the appropriate account.

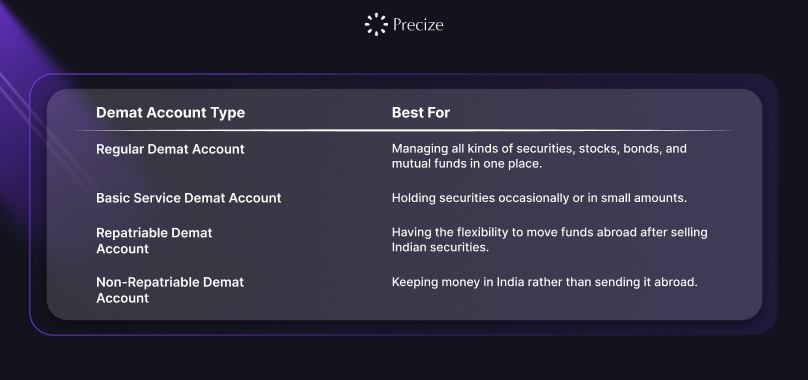

1. Regular Demat Account

A Regular Demat Account is for Indian residents who want to hold shares, bonds, ETFs, and other securities in digital form. It is the most common type of account and is offered by most banks and brokers.

Best For

You should consider this account if you want to manage all kinds of securities, stocks, bonds, and mutual funds in one place.

Advantages:

No restrictions on the value or number of holdings.

Easy digital access to all your securities.

Widely available with most providers.

Supports a variety of securities.

Disadvantages

Annual Maintenance Charges (AMC) apply.

Fees are charged even if the account is unused.

Not suitable if you are an NRI.

2. Basic Service Demat Account (BSDA)

A BSDA is ideal if you keep a small portfolio. The low-to-no maintenance fee slabs for BSDA have changed from "zero up to ₹50,000; low up to ₹2 lakh" to "zero up to ₹4 lakh; low up to ₹10 lakh" after September 2024. This account provides the essential features of a Demat account at a budget-friendly cost.

Best For

You should consider a BSDA if you hold securities occasionally or in small amounts.

Advantages

Very low or no maintenance fees (zero up to ₹50,000; low up to ₹2 lakh).

Perfect for beginners entering the market.

Offers essential functions at a lower cost.

Disadvantages

Limited services beyond the basics.

Automatically convert to a regular account if your holdings exceed ₹2 lakh.

Not available for NRIs or corporate accounts.

3. Repatriable Demat Account

This account is designed for NRIs who want to hold and manage Indian securities while living abroad. It allows you to transfer funds easily between India and your foreign account and must be linked to an NRE (Non-Resident External) account.

Best For

You should choose this account if you want the flexibility to move funds abroad after selling Indian securities.

Advantages

Quick and easy transfer of funds overseas.

Simple management of Indian and foreign assets.

Fully compliant with FEMA rules.

Disadvantages

Requires strict documentation (NRE account, proof of NRI status).

Often has higher charges than regular accounts.

Not available for Indian residents.

4. Non-Repatriable Demat Account

Also meant for NRIs, this account keeps your funds in India and does not allow transfers abroad. It is linked to a Non-Resident Ordinary (NRO) account and works well if you want to retain earnings in India.

Best For

You should choose this account if you want to keep your money in India rather than sending it abroad.

Advantages

Smooth management of your Indian income and assets.

Simplified compliance for holding Indian securities.

Disadvantages

Funds cannot be transferred outside India.

Regular maintenance charges may apply.

Must be linked to an NRO account.

So, you know why a Demat account is important, let’s see how you can get yours set up quickly and easily.

Step-by-Step Process to Open a Demat Account in India

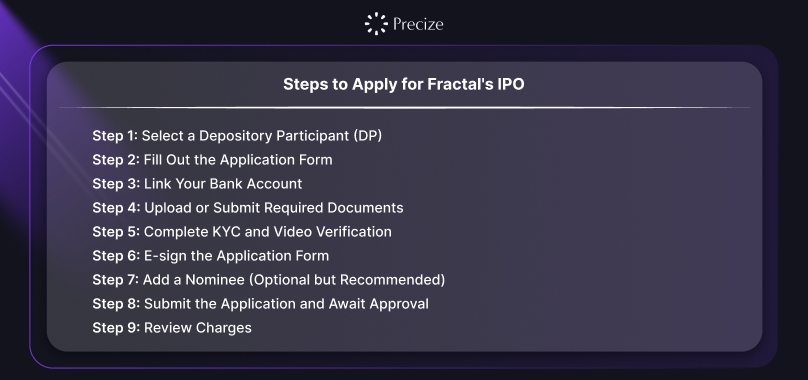

Setting up a Demat account in India is a straightforward process if you follow the steps carefully. Here are the 9 steps to open a demat account:

Step 1: Select a Depository Participant (DP)

Start by choosing a DP, which could be a bank, brokerage firm, or financial institution.

In India, only SEBI-registered entities linked with CDSL or NSDL can act as Depository Participant (DP).

Choosing a well-known bank or broker ensures your shares are held safely and securely.

Step 2: Fill Out the Application Form

Visit the DP’s branch or website and complete the application form.

You’ll provide details like your name, mobile number, PAN, and email.

This ensures your personal information matches official records.

Step 3: Link Your Bank Account

Add your savings or current account details, including account number and IFSC code.

This allows any dividends, refunds, or payments from share sales to be credited directly to your account.

Step 4: Upload or Submit Required Documents

You’ll need to provide:

PAN card (proof of identity)

Aadhaar card or passport (proof of address)

Passport-size photograph

Cancelled cheque or recent bank statement/passbook

The DP verifies these documents to comply with SEBI and RBI regulations, keeping the process secure and protecting against misuse.

Step 5: Complete KYC and Video Verification

SEBI requires all financial accounts to complete KYC. You can do e-KYC using your Aadhaar (via OTP) or record a short video for face verification if asked.

This step confirms your identity and prevents fraud.

Step 6: E-sign the Application Form

Review your details and sign electronically, usually by entering an OTP sent to your Aadhaar-linked mobile number. This makes the process fast, paperless, and legally valid.

Step 7: Add a Nominee (Optional but Recommended)

You can nominate someone who will receive your holdings in case of an unexpected event. This ensures your shares are safely transferred to your family.

Step 8: Submit the Application and Await Approval

Once your documents and application are submitted, the DP verifies everything.

If all details are correct, your account is activated, usually within a few hours to a couple of days.

You’ll receive your Demat account number and login details via email or SMS.

Step 9: Review Charges

Check for account opening fees, annual maintenance charges, or transaction costs. These vary across DPs, so knowing them upfront helps you avoid surprises later.

Following the correct process ensures a smooth account opening, but being mindful of common mistakes will keep your account secure and efficient.

Common Mistakes to Avoid While Choosing a Demat Account

When selecting a Demat account, avoiding certain mistakes can save you time, money, and future hassles. Here is what you should focus on:

Confusing a Demat Account with a Trading Account: A Demat account only holds your securities digitally. To buy or sell them, you also need a trading account. Without both, transactions cannot be completed efficiently.

Not Verifying Broker Credibility: Choose a reliable, SEBI-registered DP with a good track record, secure systems, and responsive customer support.

Blindly Opting for “Free” Accounts: Don’t select a DP just because it has no account opening fee. Look at overall service quality, platform usability, and other costs before deciding.

With these mistakes out of the way, it’s time to focus on best practices that help you stay on top of your Demat account.

Best Practices for Managing Your Demat Account

To keep your Demat account secure and running smoothly, here are some key best practices that haven’t been covered in earlier sections:

Maintain Proper Transaction Records: Keep a record of all your transactions. This helps you reconcile your holdings and is useful for any tax or financial documentation.

Regularly Check Your Account Statements: Go through your Demat account statements and transaction alerts regularly. This helps you spot any unauthorized activity or errors early and stay informed about your holdings.

Set Strong Security Measures: Use a strong password with letters, numbers, and special characters. Change it regularly and enable Two-Factor Authentication (2FA) to protect your account from unauthorized access.

Keep Your Account Active: Even if you’re not using your account frequently, log in from time to time. Inactive accounts can be more vulnerable to fraud.

Be Cautious of Fraudulent Communications: Avoid clicking on unknown links or using unverified apps. Always verify messages or notifications related to your Demat account before acting on them.

Conclusion

Now that you’ve explored the different Demat account types and learned how to manage them effectively, you’re well-equipped to make informed choices that suit your needs. Having the right account, keeping your documents updated, and following best practices ensures your holdings are secure and easily accessible whenever you need them.

To take your portfolio a step further, consider platforms like Precize. It offers access to private equity opportunities in India, giving you a chance to diversify beyond traditional securities and strengthen your overall portfolio.

Reserve Access for a diversified portfolio with Precize today!

FAQs

1. How long does it take for a new Demat account to become active in India?

Typically, a new Demat account is activated within a few hours to a couple of days after submitting all documents and completing KYC verification. The exact timeline may vary depending on the DP and the completeness of your application. Once active, you’ll receive your account number and login credentials via email or SMS.

2. Can Non-Resident Indians hold multiple Demat accounts in India?

Yes, NRIs can hold both Repatriable and Non-Repatriable Demat accounts in India, but each account type must follow its specific rules. Repatriable accounts allow funds to be sent abroad, while Non-Repatriable accounts keep money within India. NRIs should choose accounts based on their financial goals and fund transfer requirements.

3. Are there any restrictions on the types of securities I can hold in a Demat account?

Generally, you can hold a wide range of securities in a Demat account, including shares, bonds, ETFs, and mutual funds. However, some specialized securities or derivatives may require additional account types or approvals from your DP, so it’s important to confirm availability before planning your portfolio.

4. What should I do if I forget my Demat account login credentials?

If you forget your login credentials, you should immediately contact your DP or use their online recovery process. Most DPs provide options to reset your password securely via registered mobile numbers or email, ensuring your account remains protected from unauthorized access.

Disclaimer

This blog is intended to provide general information about the different Demat account types in India and how they function. It is not meant to serve as financial, legal, or professional advice. While we have made every effort to ensure the content is accurate, rules and regulations regarding Demat accounts, SEBI, and NRIs may change over time. Always confirm details with your Depository Participant (DP) or a professional before making any decisions related to opening or managing a Demat account.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved