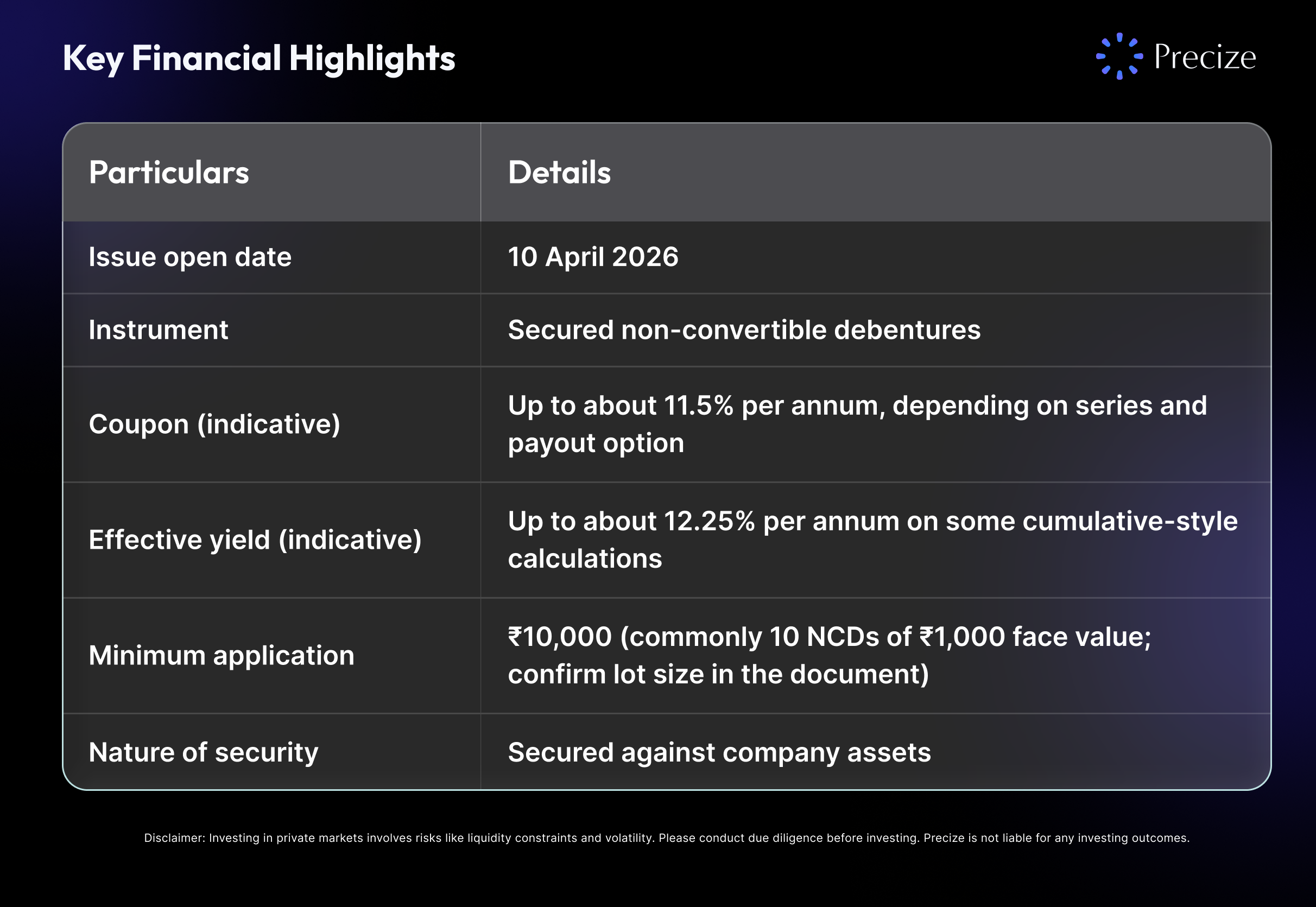

ICL Fincorp NCD April 2026: Issue Details, Yield up to 12.25%, and Investor Checklist

ICL Fincorp's April 2026 non-convertible debenture (NCD) issue is drawing retail attention because it is secured, opens in April 2026, and advertises an effective yield of up to about 12.25% per year alongside a coupon of up to about 11.5%, depending on the series and option you pick. This guide explains what that means, what to verify in the official offer document, and how this kind of instrument compares to bank fixed deposits and debt mutual funds.

Last updated: 20 April 2026. Numbers such as issue close date, exact series names, ISINs, and credit rating notches can change with the final prospectus. Treat this article as educational context, not investment advice.

At a glance: ICL Fincorp NCD April 2026

What is an NCD?

A non-convertible debenture is a bond-like instrument issued by a company. You lend money to the issuer for a fixed tenure. The company pays interest on a schedule (or compounds it, depending on the series) and repays principal at maturity. NCDs do not convert into equity, unlike some convertible instruments. Returns are contractual, not profit-linked like shares, but credit risk remains: if the issuer runs into deep financial stress, interest and principal timelines can be affected. That is why regulators, exchanges, and rating agencies matter for transparency.

For how market infrastructure treats debt listings at a high level, see the SEBI investor portal and the Reserve Bank of India for background on non-banking finance companies (NBFCs) that operate under RBI rules.

What is ICL Fincorp?

ICL Fincorp (full form often written as Industrial Credit Limited Fincorp) is an NBFC with a lending footprint that, in public descriptions, leans on gold loans, MSME finance, and vehicle finance, with a strong South India presence. Like other NBFCs, it is regulated in India under the RBI framework for non-bank lenders.

If you are comparing unlisted or pre-IPO equity with listed or unlisted debt, remember they solve different problems. Equity is ownership and long-term growth (with volatility); NCDs are contractual cash flows with issuer and liquidity risk. Precize hosts a company profile for deeper context on the business: ICL Fincorp Limited. Use that profile as a starting point, then cross-read audited financials, rating rationales, and the NCD offer document.

What is the ICL Fincorp NCD issue (April 2026)?

Public NCD issues are typically split into series (for example, Series A, B, C) with different tenures (such as 24 months, 36 months, 60 months, and so on), annual vs. cumulative interest, and sometimes step-up or call features. The April 2026 ICL Fincorp marketing focuses on two headline numbers: coupon up to about 11.5% and effective yield up to about 12.25%.

What you should pull from the final prospectus before you apply:

Exact tenures for each series (in months and years).

Interest payment dates for non-cumulative options, and how cumulative interest is compounded for cumulative options.

Issue closure date and any early closure clause.

ISIN for each series (you will need this for demat records and secondary market quotes if listed).

Credit rating from a SEBI-registered agency, including long-term and short-term notches, outlook, and rating rationale PDF.

Debenture trustee name and their role if covenants are breached.

Security cover and what assets actually sit in the security package.

If you want a simple mental model, secured means there is a defined idea of recourse to assets, not that the investment is risk-free. Security helps recovery mechanics in stress scenarios, but timely payment still depends on the issuer’s cash flows and governance.

Why is this NCD trending now?

Retail investors are actively hunting yield after years of modest returns on very safe cash instruments. When headline FD rates for many banks sit closer to high single digits, a secured NCD marketed at low double digits naturally gets shared in newsletters, forums, and wealth desks.

Three forces usually drive attention:

Absolute yield looks attractive next to very low-risk FDs.

The word secured sounds reassuring (read the fine print on what is secured and how the cover is tested).

NBFC NCDs are a familiar path for issuers to diversify funding, so repeat issuers sometimes build a track record you can study (still not a guarantee of the next issue).

Keep the discipline: higher stated yield usually prices credit and liquidity risk. If it did not, every investor would arbitrage it away in hours.

How to evaluate any NCD

1. Credit rating and rationale:

Check the latest rating letter for this issue, not an old press clipping. Read the outlook (stable, positive, negative) and the rationale section: it usually names risks like asset quality, concentration, funding mix, or regulatory changes. Ratings can be affirmed, upgraded, or downgraded after issue, which affects secondary prices and sentiment.

2. Secured vs unsecured:

Secured NCDs spell out asset cover tests, charging mechanisms, and trustee powers. Ask a simple question: If cash flow tightens, what actually happens step by step? If you cannot answer that from the document, pause.

3. Company financials and asset quality:

For NBFCs, retail investors often skim GNPA/NNPA, capital ratios, borrower concentration, and trend lines, not single-point hero metrics. Compare year-on-year movement, not one glossy chart.

4. Liquidity and your holding period:

Even listed NCDs can trade thinly. If you may need the money urgently, assume you cannot sell at a fair price immediately. Size positions for hold-to-maturity unless you actively trade credit.

5. Yield vs risk:

If two instruments look similar on paper but one pays much more, the market is usually telling you something about perceived risk, call options, subordination, or complexity. Your job is to read, not to hope.

Tax, TDS, and record-keeping

Interest on corporate bonds and debentures is typically treated as income in your hands under the rules that apply to your residency status and the instrument type. Banks and issuers may deduct TDS where thresholds and rules trigger. Rules change with Finance Acts, so treat this section as orientation, not tax advice. For your personal situation, speak with a qualified chartered accountant.

How to apply

Most public NCDs today flow through ASBA from your bank or demat routes described in the prospectus. Typical steps:

Read the offer document end-to-end.

Choose a series that matches your tenure and cash flow needs.

Apply through the channel named in the document (bank ASBA / broker/issuer pathway).

Track allotment and refunds timelines on the exchange or registrar updates.

For official issue-related disclosures, also watch the BSE or NSE debt issue pages when the issue goes live, for example, the BSE debt market section (use the live search for ICL Fincorp when available).

Conclusion

The ICL Fincorp NCD April 2026 issue is a useful case study in how Indian retail markets price yield against credit and liquidity. The headline rates are eye-catching, but the real work is document-led: security description, rating rationale, series-level cash flows, and an honest match with your risk budget.

Investors following ICL Fincorp and other pre-IPO companies reserve access with Precize to track 150+ other companies with a detailed research report, all in one place. Platforms like Precize add value by giving you access to private companies, enabling you to buy and sell unlisted and pre-IPO shares seamlessly.

The company has launched a fresh Non-Convertible Debenture (NCD) issue that opened on April 10, 2026, offering retail investors an effective yield of up to 12.25% per annum.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved