NCDEX FY26 Results Show a ₹41 Cr Loss Despite a ₹770 Cr Capital Raise - Key Insights for Investors

For investors tracking exchange businesses and NCDEX unlisted shares, the company is no longer a simple agri-commodity exchange story. FY26 shows three forces moving at once: weak operating performance, a stronger capital base, and a push into new products that could reduce dependence on suspended agricultural futures.

NCDEX FY26 Results: The Headline Numbers

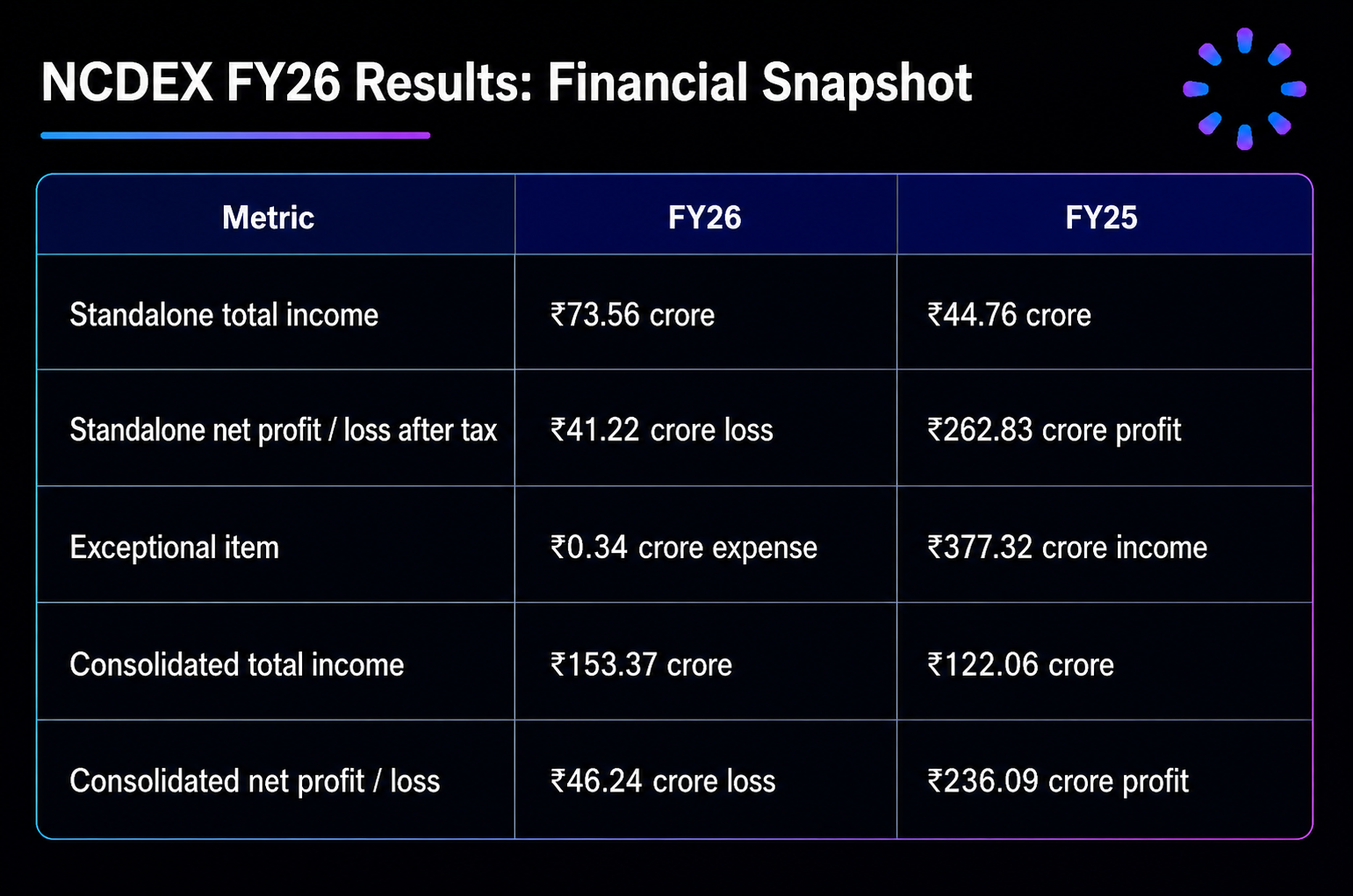

The National Commodity and Derivatives Exchange (NCDEX) FY26 results show improvement in income, but the core operating picture remained difficult. Put another way, the NCDEX financial results 2026 point to balance-sheet resilience rather than earnings recovery.

On a standalone basis, NCDEX reported total income of ₹73.56 crore in FY26, up from ₹44.76 crore in FY25. At first glance, that looks like strong top-line growth. However, the exchange still reported a net loss after tax of ₹41.22 crore in FY26.

The comparison with FY25 needs care. In FY25, NCDEX reported a profit of ₹262.83 crore, but that number was driven mainly by exceptional income of ₹377.32 crore. In FY26, the exceptional item moved the other way, with a small exceptional expense of ₹34 lakh.

That means the year-on-year swing is not simply a collapse from profit to loss. FY25 was unusually supported by a one-time exceptional gain, while FY26 reflects the harder reality of restricted commodity trading revenue.

For retail investors who compare exchanges as businesses, the key point is simple: NCDEX still has market infrastructure value, but FY26 earnings do not yet show a clean recovery.

If you track unlisted companies and exchange-related opportunities, the Precize screener can help you compare available private-market names, financial trends, and sector exposure before investing.

Why the SEBI Commodity Suspension Still Dominates the Story

The biggest issue in the NCDEX investment case is not accounting. It is regulation.

SEBI's suspension of trading in several major agricultural commodity derivatives, including commodities such as chana and mustard seed, has been extended to 31 March 2027. These contracts matter because NCDEX has historically been closely linked to India's agri-commodity derivatives market.

When important contracts cannot trade, exchange economics weaken. Trading volume falls, transaction income suffers, and fixed costs such as technology, compliance, staff, and infrastructure do not fall at the same pace.

That is why the FY26 report points to operating losses and negative operating cash flows. The exchange is still functioning, but its most important revenue engine remains partly constrained.

For investors, this makes the suspension timeline the central catalyst. If major agri contracts resume after March 2027, NCDEX may regain part of its historical trading base. If the suspension continues or activity shifts elsewhere, the exchange will need new products and new segments to carry more weight.

You can review broader investor questions around private-market investing and regulatory risk in the Precize FAQs.

Why NCDEX Still Qualifies as a Going Concern

Despite the losses, the auditor's going-concern assessment is important. In plain English, "going concern" means the company is expected to continue operating and meet its liabilities over the near term.

NCDEX's case rests on three supports.

First, the exchange has maintained the required net worth under regulatory guidelines. That matters because exchanges operate in a regulated market infrastructure role, not as ordinary trading businesses.

Second, NCDEX has enough liquidity to meet liabilities over the coming year, based on the source financials. This reduces near-term solvency risk even though operations remain under pressure.

Third, the ₹770 crore preferential allotment in October 2025 materially strengthened the balance sheet. After the raise, reserves stood at about ₹1,275.40 crore, giving NCDEX room to invest in technology, risk systems, market development, and new product lines.

Public reporting around the fundraise also points to a broader strategy: NCDEX wants to evolve from a mainly agri-commodity exchange into a multi-asset market infrastructure platform. That plan will take time, but the capital raise gives management a larger runway.

The Role of Subsidiaries in NCDEX's Consolidated Results

The consolidated NCDEX FY26 results show that subsidiaries remain part of the cushion, even though the group reported a loss.

The group, including subsidiaries such as NCCL and NCDEX e-Markets Limited (NEML), reported total income of ₹153.37 crore and a net loss of ₹46.24 crore in FY26, based on the source draft.

NEML remained profitable, contributing ₹8.95 crore of net profit to the consolidated numbers. That does not offset the entire group loss, but it does show that NCDEX is not dependent on one operating line alone.

For investors, this distinction matters. Standalone exchange performance reflects the pressure on the core exchange business. Consolidated performance shows the broader group, including businesses that may have different revenue drivers and risk profiles.

Still, subsidiaries are a buffer, not a full solution. A durable recovery likely needs improvement in the core exchange franchise, successful product diversification, or both.

RAINMUMBAI: India's First Exchange-Traded Rainfall Derivative

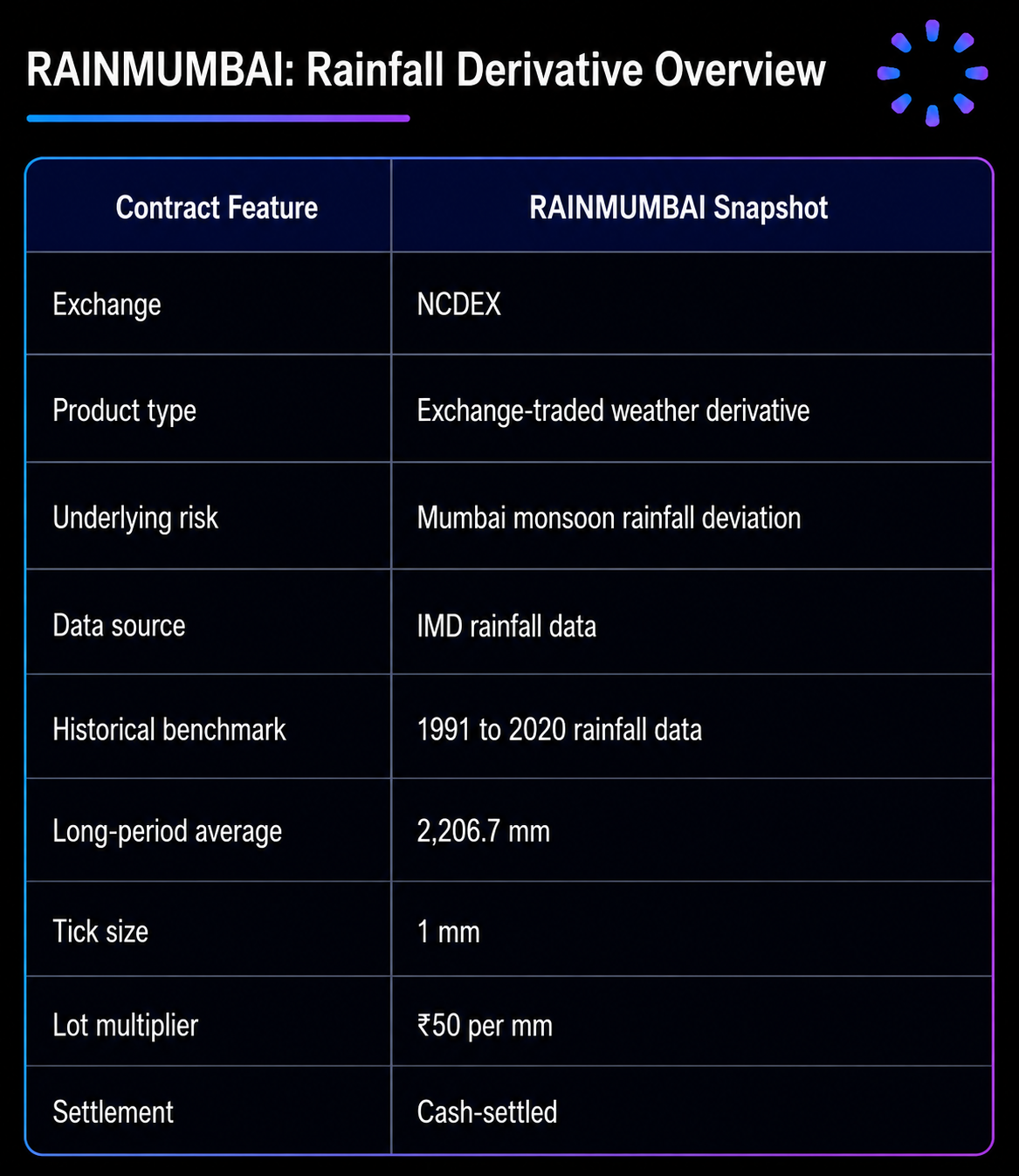

The most important strategic development after FY26 was the launch of NCDEX RAINMUMBAI, India's first exchange-traded weather derivatives contract based on rainfall.

RAINMUMBAI is designed to help market participants hedge financial losses linked to Mumbai monsoon rainfall. It is built around rainfall deviations from Mumbai's long-period average during the June to September monsoon season.

According to public reports, the contract uses official rainfall data from the India Meteorological Department (IMD), including Mumbai observation points such as Santacruz and Colaba. It is cash-settled, which means participants do not deliver or receive any physical commodity. The payoff depends on the rainfall index.

This product is important because it moves NCDEX beyond traditional agri-commodity price risk. For India, rainfall derivatives on a regulated exchange are new. Weather risk affects farmers, insurers, lenders, transport operators, power companies, and urban businesses. A listed, regulated derivative can make that risk more measurable and tradable.

What's Next After RAINMUMBAI?

Public statements around the launch suggest NCDEX is already planning additional weather-risk contracts, including a North-East monsoon rainfall derivative and a heat index contract. Managing Director Arun Raste has also noted that while global exchanges such as CME offer heat and snowfall indices, NCDEX is positioning RAINMUMBAI as a global first in exchange-traded rainfall derivatives.

If these follow-through products launch with similar IMD-backed data and cash settlement, they could broaden NCDEX's non-agri catalogue and give hedgers more regional climate-risk tools. The commercial test will still be liquidity, not innovation alone.

Who Could Use RAINMUMBAI?

RAINMUMBAI is not only a farmer-focused product. Its larger promise is in climate-risk management for businesses exposed to monsoon variability.

Potential users include:

Banks and lenders: Heavy rainfall or weak rainfall can affect borrowers, crop output, cash flows, and repayment behaviour.

Power companies: Hydropower generation and electricity demand can both shift with rainfall patterns.

Transport and logistics companies: Heavy Mumbai rains can disrupt movement, delivery times, and operating costs.

Taxi and mobility platforms: Urban flooding can affect rides, route efficiency, driver availability, and customer demand.

Commodity participants: Rainfall affects crop supply, quality, storage, and mandi activity.

The product also has broader signalling value. Climate risk is becoming a financial risk, not just an environmental topic. If NCDEX can build liquidity in weather derivatives, it could create a differentiated market segment in India.

However, the word "if" matters. New derivatives need trust, education, market makers, hedgers, speculators, and enough daily liquidity. A product can be innovative and still take years to become commercially meaningful.

Deferred Tax Assets: What They Signal

NCDEX recognized ₹43.35 crore in deferred tax assets in FY26, based on the source draft. A deferred tax asset usually reflects tax benefits that a company expects to use in future periods, often against future taxable profits.

In plain terms, management is indicating that its approved business plan supports a return to taxable profitability over time.

Investors should treat this as a signal of confidence, not proof of recovery. Deferred tax assets depend on future profits. If operating performance remains weak for longer than expected, assumptions may need review.

That makes the next two years important. Investors should watch whether NCDEX can convert its stronger balance sheet and new product launches into recurring income.

What Investors Should Watch Next

The investment case for NCDEX now depends on execution across several moving parts.

The first factor is the SEBI suspension timeline. A resumption of key agri-commodity contracts after March 2027 could be the clearest catalyst for trading volumes and fee income.

The second factor is new product liquidity. RAINMUMBAI is a landmark launch, but investors should track traded volumes, open interest, participant mix, and repeat institutional use.

The third factor is capital deployment. The ₹770 crore raise gives NCDEX resources, but the market will eventually judge whether those funds produce durable growth.

The fourth factor is multi-asset expansion. Public reporting around the fundraise points to NCDEX's broader ambitions beyond its legacy agri-commodity base. Any progress in equity, weather, or other risk-management products could change the valuation narrative.

The fifth factor is subsidiary performance. NEML's profitability helped cushion the group in FY26. Continued subsidiary strength can reduce pressure on the standalone exchange, but it cannot fully replace a recovery in core exchange economics.

You can read more market explainers and private-company analysis on the Precize blog.

Analyst View on NCDEX FY26 Results: A Preparation Phase

The NCDEX FY26 results do not show a turnaround yet. They show a company preparing for one.

The current earnings profile remains weak because the exchange is still dealing with suspended agri-commodity contracts. But the balance sheet is stronger after the ₹770 crore raise, the group still has profitable subsidiary support, and RAINMUMBAI shows that NCDEX is trying to build new markets rather than waiting passively for regulatory conditions to improve.

For investors, the right question is not whether FY26 was a good year. It was not, from a profitability perspective. The better question is whether NCDEX can use FY26's capital base and FY27 product launches to rebuild relevance before or alongside the possible return of suspended commodities.

That makes NCDEX a long-term market-infrastructure watchlist name, not a near-term earnings momentum story.

Bottom Line

The NCDEX FY26 results show a difficult operating year, but not a passive company. Losses remain real, and the SEBI suspension of agri futures is still the main overhang. At the same time, the ₹770 crore capital infusion and the RAINMUMBAI launch give NCDEX tools to prepare for a broader recovery.

For investors, NCDEX is a watchlist case built around regulatory normalization, product diversification, and balance-sheet-backed execution. The clearest catalyst remains the potential lifting of commodity suspensions in 2027. Until then, RAINMUMBAI and other new products will show whether NCDEX can build growth beyond its traditional agri-commodity base.

FAQs on NCDEX FY26 Results and RAINMUMBAI

1. Why Did NCDEX Report a Loss in FY26?

NCDEX reported a loss mainly because major agri-commodity contracts remain suspended, reducing the exchange's core trading revenue opportunity. FY25 profit was also boosted by a large exceptional income item, so the year-on-year comparison looks sharper than the underlying operating trend.

2. Is NCDEX Financially Weak After the FY26 Loss?

The FY26 loss is a concern, but the balance sheet appears stronger after the ₹770 crore preferential allotment. The auditor's going-concern view, regulatory net-worth compliance, and available liquidity suggest the near-term issue is profitability, not immediate survival.

3. What Is RAINMUMBAI?

RAINMUMBAI is NCDEX's exchange-traded rainfall derivatives contract linked to Mumbai monsoon rainfall. It uses IMD rainfall data and cash settlement to help participants hedge financial exposure to rainfall deviations.

4. Why Does the SEBI Commodity Suspension Matter So Much for NCDEX?

NCDEX has historically depended heavily on agricultural commodity derivatives. When key contracts such as chana and mustard seed are suspended, trading activity and fee income can fall while fixed costs remain.

5. What Should Investors Track in NCDEX After FY26?

Investors should track the March 2027 suspension deadline, RAINMUMBAI trading volumes, open interest, new product launches, subsidiary profitability, and how the ₹770 crore capital raise is deployed.

If you want to compare NCDEX with other exchange and infrastructure names in the private market, use the Precize screener to review available unlisted opportunities and financial trends before investing. If you need help understanding the process contact Precize Care. Stay updated with NCDEX and other unlisted companies through our Precize Community. If this article was useful, you can share it with other investors through the Precize Referral Program.

Disclaimer: This content is for informational purposes only and does not constitute investment advice. Investing in unlisted shares involves risks including illiquidity and potential loss of capital. Consult a qualified financial advisor before making investment decisions. Precize is not a stock exchange and is not regulated by SEBI.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved