MSEI trading volume April 2026: The liquidity inflection point

On April 1, 2026, the Metropolitan Stock Exchange of India (MSEI) - active in equities, derivatives, currency, and debt, but long a quiet third exchange next to the NSE and BSE - recorded a sharp one-day jump in traded quantity and rupee value. Institutions and retail readers alike are asking whether this is a lasting step-change or a maker-driven spike.

MSEI trading volume April 2026: The headline numbers

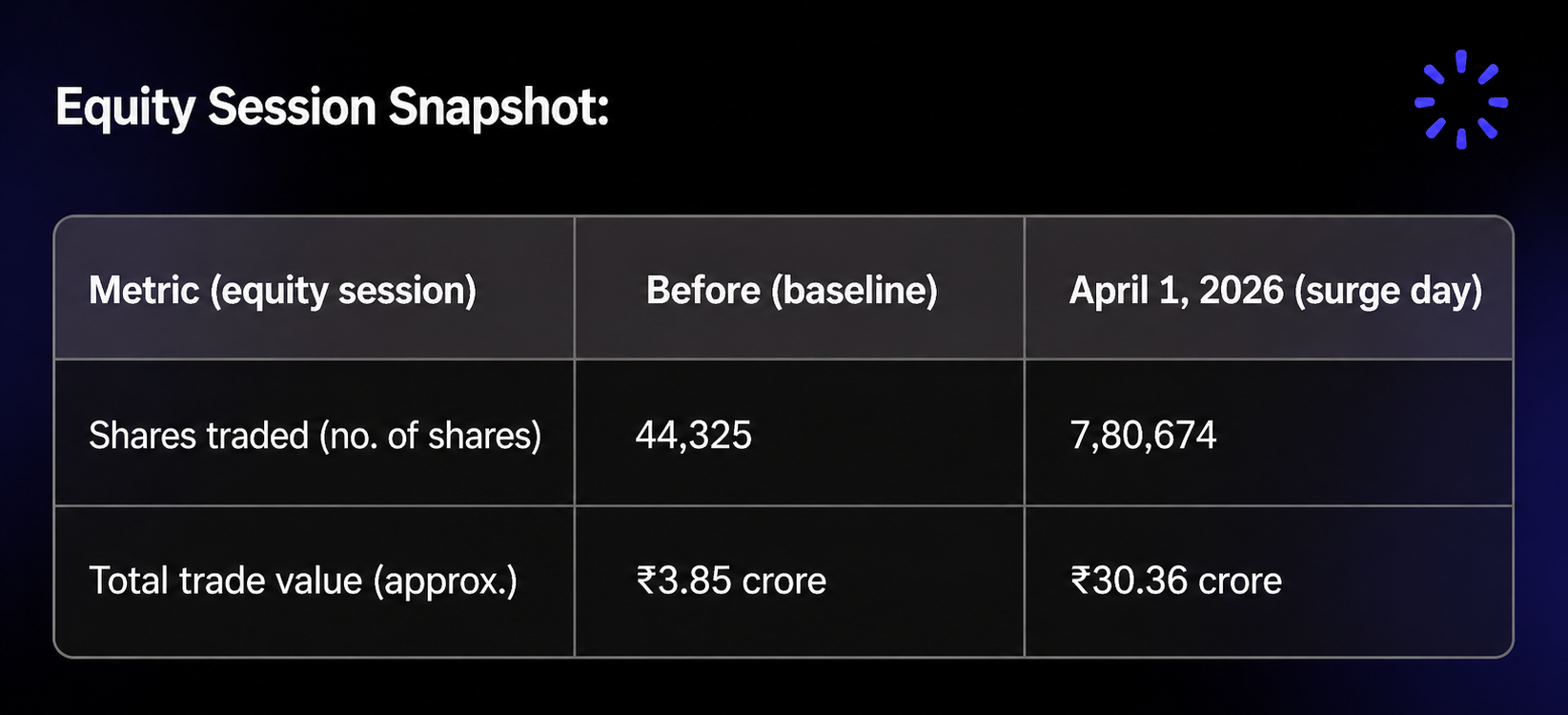

The most direct way to see why MSEI trading volume in April 2026 mattered is to compare the day of the surge with the prior baseline (as reported in exchange data and follow-on commentary).

Volume rose by a large multiple—often described in round terms as an ~18x jump in share count. Turnover moved up roughly 8x in rupee terms. Those two facts sit together: You can have a big multiple in shares and a smaller multiple in rupees when average trade sizes and prices shift alongside participant behaviour.

For analysts, the signal is less “markets were hot” and more “trading density changed fast.” When an exchange has run at a low base for a long time, a single-day move of this scale usually points to a defined catalyst—not a slow drift in retail enthusiasm.

What is MSEI (and why liquidity is the product)?

The Metropolitan Stock Exchange of India (MSEI) operates as a stock exchange under India’s market framework, alongside the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE). It offers multiple segments, but equity turnover and ecosystem depth are where exchanges are most often ranked in public discussion.

An exchange is not only technology and regulation; it is also liquidity. Without tight spreads and reliable depth, brokers, proprietary desks, and arbitrage players have less reason to route flow. That is why structural programmes such as market making matter: They are designed to change participation and quoting behaviour, not just marketing visibility.

Why market makers shifted MSEI trading volume in April 2026

The primary catalyst described for the April activity is the activation of market makers on MSEI’s equity segment. Market makers commit to continuous bid and offer quotes, which tends to:

Tighten spreads, reducing impact cost for others hitting the book.

Stabilise visible depth, so participants can size orders with more confidence.

Seed a network effect: better quotes can attract more intermediaries, which can in turn attract HFT and arbitrage interest if the flow persists.

MSEI has positioned the initiative as a structural effort rather than a one-day promotion. The open question always is whether day-one prints turn into a sustained average for trade value and diversity of participants, or whether activity concentrates around market-making obligations in ways that look strong on the tape but do not yet reflect broad, organic demand.

MSEI Financials: 9MFY26 and Operating Leverage

The April 1 session does not sit in a vacuum. In 9MFY26 financial highlights (as cited in prior analysis of the exchange’s trajectory), the direction of travel in losses mattered as much as any single day’s turnover:

EBITDA loss narrowed sharply year-over-year: From ₹23.08 crore in 9MFY25 to ₹5.32 crore in 9MFY26 (roughly 78% improvement in loss magnitude).

PAT loss also narrowed: From ₹27.04 crore to ₹11.68 crore (about 57% improvement).

Exchange economics often show high operating leverage: Fixed technology, compliance, and infrastructure costs are heavy, while incremental trading and clearing fees can fall through at high margin once scale is credible. That is why a ₹30 crore (order of magnitude) daily trade value handle is discussed as a milestone: if similar levels become routine, they support the path toward covering fixed costs and, eventually, profitability but if volumes mean-revert, the financial story reverts with them.

Always cross-check these figures in the latest official filings and presentations, as exchange reporting can update with new periods.

MSEI vs NSE and BSE: The moat is real

NSE and BSE still hold the bulk of listed liquidity, listing preference, and ecosystem habit in Indian cash and derivatives markets. For MSEI, “technically able to trade” is not the same as “default venue for new listings and flow.”

A balanced read of MSEI trading volume in April 2026 is therefore:

Positive signal: The exchange can execute a liquidity programme and move observed turnover quickly.

Unsolved question: Can MSEI hold a higher average trade value and broaden its participant base over quarters, not hours?

Risks to keep in mind include maker-led volume that may not yet reflect diverse end-investor demand, and the long time and trust required to narrow a structural gap with incumbents.

If you follow MSEI in the unlisted market

Unlisted and pre-IPO style access is not the same as buying a large liquid listed name. Pricing can be negotiated, disclosures may differ from what you see in a top-tier listed company, and liquidity in the unlisted market has its own rules.

If you are evaluating MSEI unlisted interest or any unlisted name use a disciplined process: Compare claims to primary sources, understand fees and counterparty risk, and keep questions handy for your advisor or platform. The Precize screener is one way to explore unlisted companies and research context; for process and eligibility questions, the FAQs are a useful stop. If you need help on a specific case, Precize Care is the right channel for support.

How to read MSEI trading volume without overfitting one day

A single session can be important and still be misleading if you treat it as a forecast. Here is a practical way to keep MSEI trading volume in April 2026 in perspective.

Separate “record day” from “new regime.” Records happen when a rule changes, a programme launches, or a large participant begins routing flow. The right follow-up question is always: What is the moving average over the next 20–60 trading days? If the average steps up and stays up, you are learning something about structure. If the series spikes once and drifts back, you learned something about activation, not necessarily about durability.

Compare like with like. Equity turnover should be compared across similar sessions (same segment, same holiday calendar effects, and ideally similar macro days). If you mix currency or debt anecdotes into an equity headline, you can confuse yourself quickly.

Watch rupees, not only shares. Share multiples can look enormous when the prior base is tiny. Trade value in rupees often tracks closer to economic activity on the tape, though it still needs context from average trade size and who is trading.

Anchor claims to primary sources. Screenshots, tweets, and forum posts age badly. For exchange statistics, daily reports and official releases beat secondary summaries when you need precision.

Keep exchange liquidity distinct from unlisted ticket risk. If you own or are considering MSEI unlisted exposure, the exchange improving its listed ecosystem can matter for sentiment and long-term narrative, but your personal outcome still depends on entry valuation, documentation, and secondary liquidity in the unlisted channel—not on one day’s on-exchange turnover alone.

This disciplined lens matches how Precize approaches education: Specific numbers, clear risks, and no substitute for verifying facts yourself when you allocate capital. Learn more on the Precize blog or explore names with the Precize screener.

Conclusion: A possible turning point—if the average proves it

MSEI trading volume in April 2026 is best read as evidence of execution: the exchange activated a market-making programme and saw rupee turnover move to a level that was unusual relative to its own history. That supports a narrow claim: MSEI can engineer a liquidity event when it deploys the right market structure.

The broader claim of a durable third pole next to the NSE and BSE requires repeated evidence: higher average trade value, staying power in depth and spreads, and ecosystem participation beyond a single-day print. If those do not follow, the story remains a turning-point attempt rather than a turning point in fact.

To stay updated on the MSEI and other unlisted companies join our community.

What to watch next

For the next quarter, the more useful chart is not the one peak day but the rolling average of daily trade value and how often the market prints above the old baseline. If a band near ₹30 crore (or higher) becomes a floor rather than a spike, the investment narrative for the exchange’s trading franchise—and for how the market prices MSEI-related risk—becomes materially easier to support with data.

For more market and unlisted education, see the Precize blog. If this article was useful, you can share it with other investors through the Precize referral program.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment, legal, or tax advice. It is not a recommendation to buy, sell, or hold any security, including MSEI or Metropolitan Stock Exchange of India–related instruments or unlisted interests in them. Investing and trading involve risk of loss; unlisted shares can be illiquid and harder to price than listed stocks. Figures and dates are summarised from public exchange materials and commentary as of the article date - verify every number in MSEI official reports, circulars, and filings before you rely on them. Precize is not a stock exchange and is not regulated by SEBI as an exchange. Precize Care can help with platform questions, not personalised investment advice. Consult a qualified financial adviser before making investment decisions.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved