Acko IPO 2026-27: Valuation, Risks, and DRHP Watchlist

What is the Acko IPO? The Acko IPO is the expected public listing process for Acko General Insurance, likely in 2026-27, with market discussions around a $2-2.5 billion valuation. For investors, the key test is whether strong growth converts into durable underwriting profitability after listing.

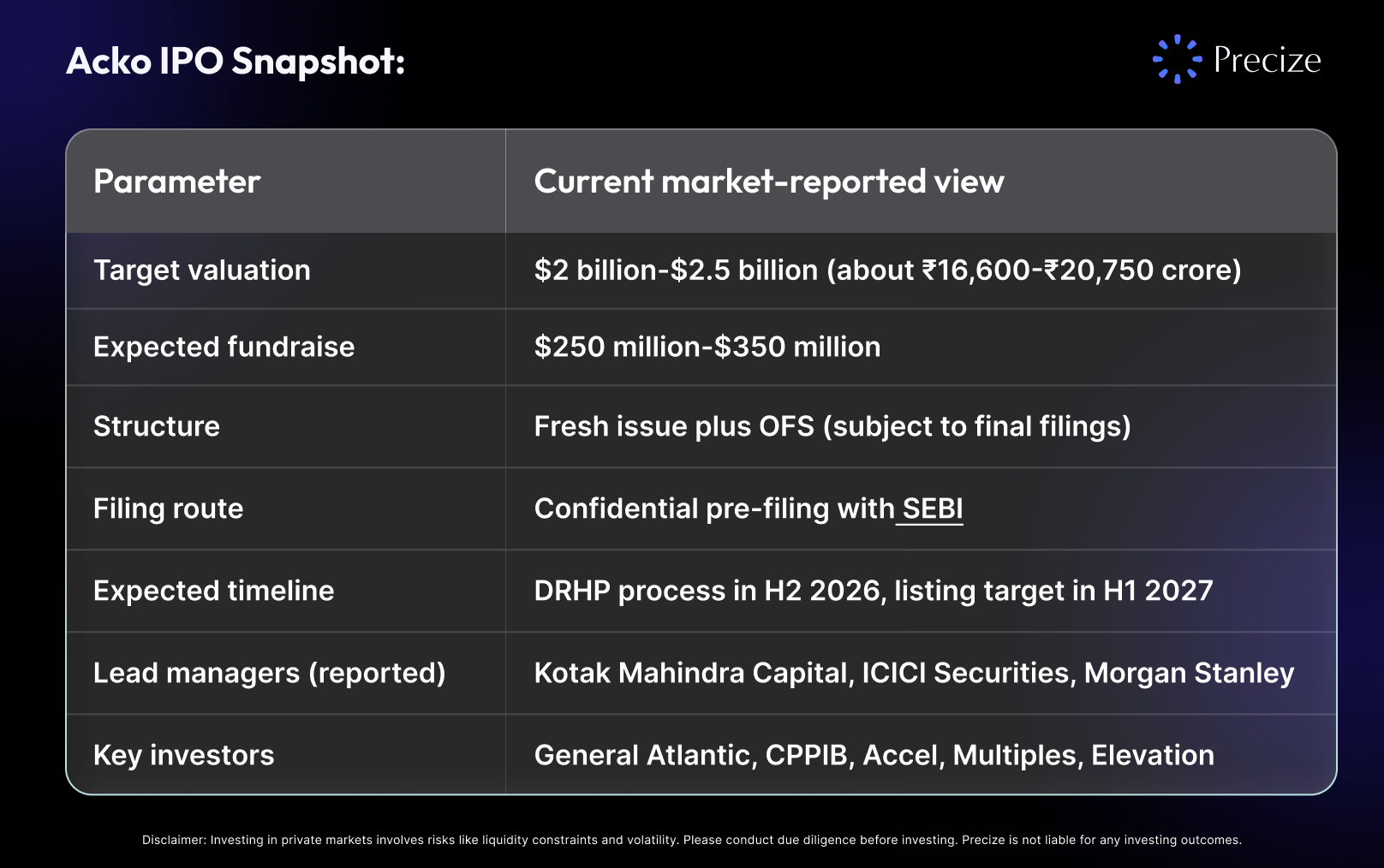

Acko IPO Snapshot: What Is Reported So Far

These numbers can change before launch. Always validate against final documents on SEBI, BSE, and NSE.

What Acko Does, and Why It Is Different

Acko started with a clear bet: avoid the agent-heavy model and build a digital-first insurer. Instead of relying primarily on offline distribution, it has focused on direct channels and embedded partnerships where insurance is sold at the point of need.

This model is central to the Acko General Insurance listing narrative. Embedded distribution through platforms such as Amazon, PhonePe, redBus, and others can lower acquisition friction and improve scale velocity. In theory, this can support better long-term unit economics than a high-commission model.

The company also claims a very large operating scale in customer reach and policy issuance. If sustained, that data base can become an underwriting advantage over time, especially if claim prediction and pricing improve with learning cycles.

Acko Financial Trajectory: The Bull Case Is Real, but Incomplete

The strongest part of the current Acko IPO 2026 story is the combination of growth and improving losses.

Revenue momentum: FY25 revenue is widely reported at ₹2,837 crore, up roughly 35% year on year.

Loss reduction: Net loss reportedly declined from ₹667 crore (FY24) to ₹424 crore (FY25).

Portfolio mix broadening: Motor and health books are both meaningful, reducing single-line concentration risk.

This is what public market investors typically want to see before a growth listing: Expanding top line with improving loss profile. But this is not the same as proven structural profitability. For insurers, gross premium growth alone is never enough. Quality of underwriting and claims experience drive long-term value.

The Acko IPO Valuation Debate: Growth Premium or Early Overpricing?

At a $2-2.5 billion range, Acko IPO valuation metrics imply meaningful optimism on future profitability.

A simple framing:

Why bulls support the premium

High growth relative to broader sector growth.

Digital-native distribution model.

Embedded partnerships that can scale quickly.

Potential data advantage in underwriting and pricing.

Why bears push back

The company remains loss-making.

Claims quality and combined ratio discipline are still under watch.

Growth-phase economics can look strong before mature-cycle pressures appear.

Premium leaves less room for execution errors after listing.

In plain terms, investors are not paying for where Acko is today. They are paying for where it could be in three to five years.

If execution stays strong, this can become a defining digital insurance India IPO case over the next listing cycle.

Acko vs Digit Insurance and Other Listed Benchmarks

Any Acko vs Digit Insurance comparison should be done carefully because business mix, maturity, and listed market conditions differ.

Go Digit Insurance provides a listed reference for investor appetite in digital insurance.

PB Fintech (PolicyBazaar) represents a different, more asset-light platform model.

Traditional listed insurers provide scale and profitability benchmarks, but with different distribution economics.

For the Acko IPO, growth is the headline advantage. Scale and profitability consistency are the gaps investors will test through disclosures and post-listing quarters.

Comparison with Unlisted Peer: Acko vs Care Health Insurance

Any Acko vs Care Health Insurance comparison should be done carefully because business model, product focus, and underwriting maturity differ.

Care Health Insurance represents a pure-play, standalone health insurer with scale in retail health, group business, and wellness-led offerings.

It provides a benchmark for underwriting-led profitability and claims experience, unlike Acko’s tech-first, multi-line approach.

Acko operates as a digital-first, multi-product insurer, while Care Health reflects a focused health insurance model with deeper actuarial track record.

For the Acko IPO, growth remains the headline advantage. However, underwriting consistency and profitability discipline are the gaps investors will evaluate through disclosures and post-listing performance.

Why the SEBI Confidential Filing Matters

The Acko DRHP process reportedly uses a confidential route. That has three practical effects:

The company gets regulatory feedback before full public visibility.

Timing flexibility improves if market conditions weaken.

Institutional demand can be tested quietly before public launch.

For retail participants, the downside is delayed transparency. Until the public document is out, the market has only partial information.

Risks That Can Reprice the Acko IPO Quickly

A high-growth insurance listing can rerate fast in either direction. These are the risks to watch most closely:

1) Profitability timeline risk

Losses are narrowing, but the business is still in the red. If breakeven timing slips, valuation multiples can compress.

2) Underwriting quality risk

Investors should focus on combined ratio trend, claims ratio by segment, and whether growth is being bought at weak margins.

3) Regulatory risk

Digital insurers operate within tight compliance boundaries under IRDAI. Any constraints on expense structure, product mix, or distribution economics can alter trajectory.

4) Platform concentration risk

If a meaningful share of demand depends on external platform partners, pricing renegotiations or strategy shifts can affect customer acquisition economics.

5) OFS mix and capital use risk

If OFS is large relative to fresh issue, less IPO capital enters the company for growth, reserves, and operational scaling.

6) Market sentiment risk

Recent IPO market behaviour in India has shown that growth stories can list with volatility when valuations run ahead of near-term fundamentals.

The Structural Long-Term Opportunity Is Still Significant

The positive long-term thesis is straightforward. India remains under-penetrated in insurance compared with many developed markets, while digital adoption and customer comfort with app-led financial products continue to rise.

That backdrop supports a multi-year runway for digital insurance providers. If Acko can convert distribution scale into stronger underwriting outcomes, it can build durable value beyond headline premium growth.

If you are mapping broader pre-IPO and private-market opportunities alongside public listings, you can also compare ideas through the Precize screener and related market explainers on the Precize blog.

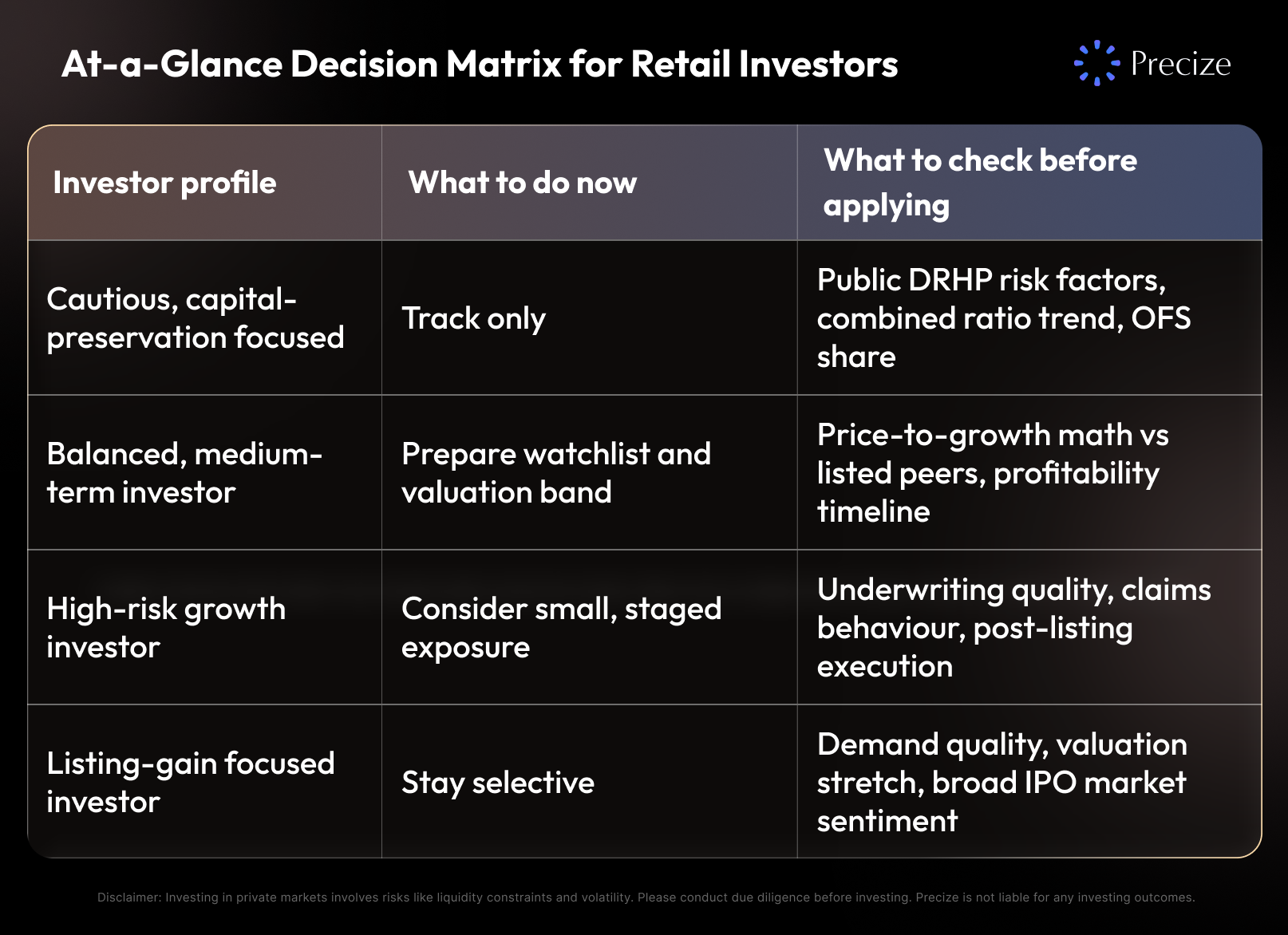

At-a-Glance Decision Matrix for Retail Investors

If you are evaluating the Acko IPO 2026 setup, this quick matrix can help you align action with your risk profile:

This matrix is not a recommendation. It is a process tool to reduce emotional decision-making when IPO headlines become noisy.

Retail Investor Framework: What to Do Before Applying

Do not rush this issue just because it is high-profile. A disciplined checklist works better.

Phase 1: Watch (now to public DRHP)

Track filing progress and timeline updates.

Avoid hard valuation conclusions before full disclosures.

Phase 2: Analyze (once DRHP is public)

Read segment-level claims and combined ratio disclosures.

Check customer acquisition cost trend and renewal behaviour.

Examine related-party disclosures and contingent risk notes.

Compare implied valuation to listed peers on consistent metrics.

Phase 3: Decide (at price band)

Judge fresh issue vs OFS balance.

Evaluate promoter and investor post-issue holding structure.

Size your exposure based on risk tolerance and time horizon.

If you are new to IPO evaluation mechanics, basic investor process questions are covered in the Precize FAQs.

DRHP Verification Checklist Before You Apply

Before committing capital, use the public Acko DRHP as your primary source document and verify these points yourself:

Underwriting quality by segment: Look at combined ratio and claims ratio trends by product line, not only aggregate growth numbers.

Expense discipline: Check whether operating expense trends support a realistic path to profitability at scale.

Capital use clarity: Evaluate fresh issue vs OFS mix and how much new capital actually strengthens the business.

Distribution concentration: Review dependence on key platform partners and sensitivity to contract changes.

Regulatory disclosures: Read regulatory observations and compliance disclosures carefully, especially for fast-scaling insurers.

Related-party and governance notes: Assess disclosures on governance controls, party transactions, and management incentives.

As reference points, monitor official updates from SEBI, exchange disclosures on BSE and NSE, and sector-level regulatory context from IRDAI.

Verdict on the Acko IPO

The Acko IPO is a credible growth story, but not an easy one. The company appears to have real momentum, a differentiated distribution model, and improving financial trend lines. At the same time, the valuation ask implies confidence in future underwriting and profitability execution that is not fully proven yet.

For medium-term investors (three to five years), the listing could be attractive at a sensible price. For short-term listing-gain seekers, the risk-reward may look less compelling if pricing is aggressive.

The right sequence is simple: wait for the public Acko DRHP, evaluate underwriting quality and capital structure carefully, then decide based on valuation discipline.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. Investing in IPOs carries risks, including potential loss of capital. Please consult a qualified financial advisor before making investment decisions. Data points are based on publicly discussed information as of April 2026 and should be verified against the latest official filings.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved