NSE IPO OFS: India's Most Awaited Listing

What Is the NSE IPO OFS?

Offer for Sale (OFS) in an IPO setting usually means selling shareholders tender stock into the public offer, while the company itself does not raise new money from a fresh issue in that same tranche (unless the final structure adds a fresh leg, which is not what reporters are emphasizing today).

A simple mental model: liquidity for existing owners, not a capital raise to build new factories. That shifts what you evaluate:

Who is selling and how much will float over time

Governance and regulatory history

Valuation at which the book clears versus earnings quality and capital allocation

Snippet-style definition: An NSE IPO via OFS is a proposed listing where eligible existing shareholders may sell stock to public investors under SEBI rules and the final prospectus, while NSE, as described in press, does not sell new shares to raise funds in that same tranche.

For the regulatory text behind minimum holding periods and related conditions, start from SEBI (including SEBI regulations) and the eventual DRHP disclosures rather than summary articles alone.

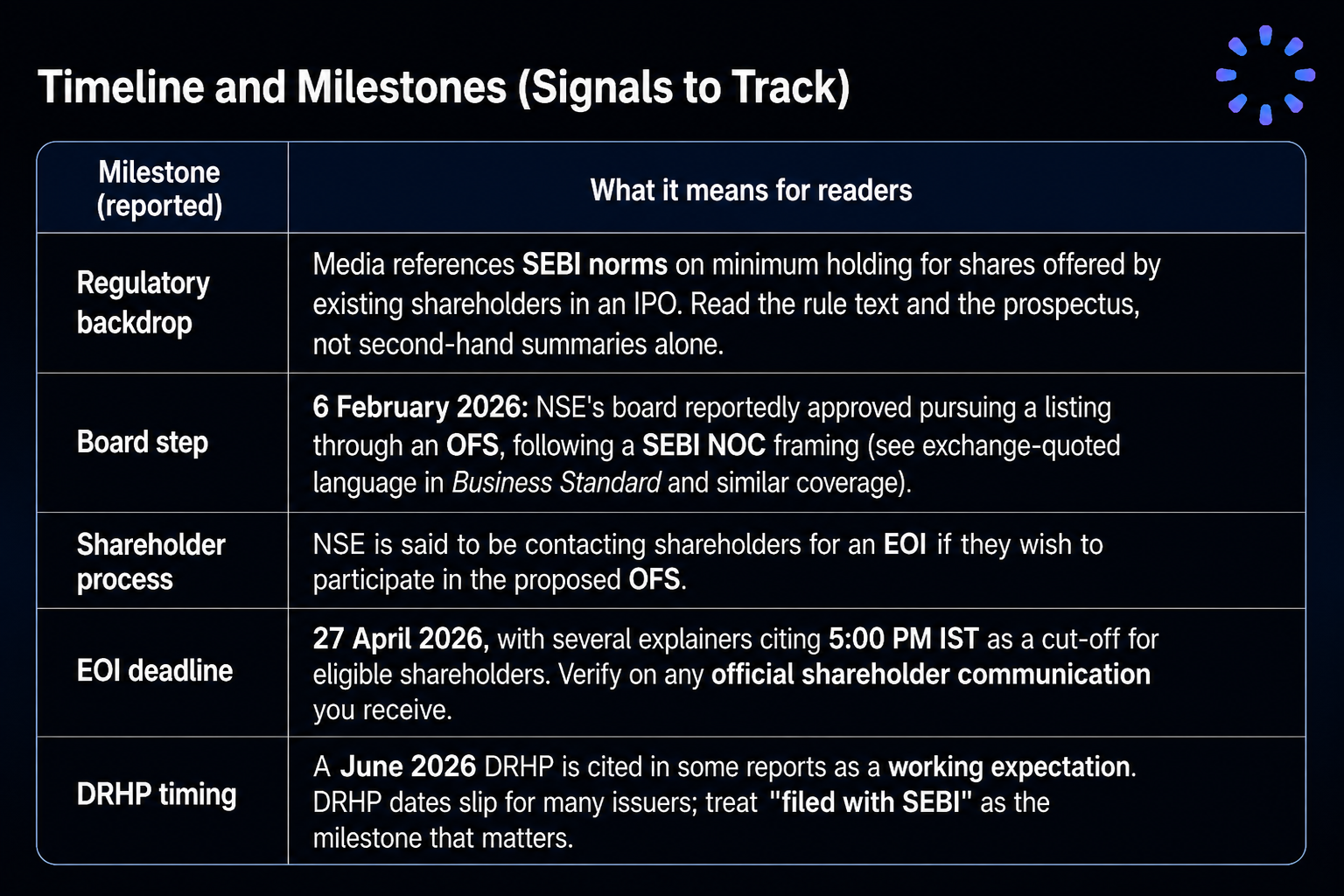

Timeline and Milestones (Signals to Track)

Public reporting moves fast. Use this section as a checklist of signals, not a guarantee.

One reliable habit: bookmark NSE corporate disclosures and SEBI filing pages once the DRHP exists.

Why NSE Is Likely Going the OFS Route

NSE is widely described as a mature, profitable market infrastructure company. In that situation, a listing is often less about survival capital and more about liquidity, transparency, and orderly exits for long-held private stakes.

An OFS-led structure also frames the debate for markets: attention moves to valuation, governance, and post-listing float, rather than "what new project will IPO proceeds fund?"

For recent profitability and regulatory charge context on the exchange itself (a separate topic from the offer structure), see Precize's analysis of NSE FY26 results and regulatory headwinds.

Eligibility: Who Can Participate in the OFS

This is where many retail readers get surprised.

Only shareholders who meet holding conditions can participate in the OFS selling process. Reporting often cites a continuous holding reference date of 15 June 2025, with additional conditions that shares be fully paid-up and free from encumbrances (for example, pledges).

Why SEBI cares: Without a holding window, late buyers could treat the unlisted market like a fast pass into a structured exit, which can work against stable cap tables around a listing.

Practical translation: If you bought after the cut-off date described in reporting, assume you are not in the "sell into the OFS" cohort unless your records and the DRHP say otherwise.

Selling shareholders in the OFS process are not supposed to turn around and subscribe to the IPO as buyers. The design aims to separate distribution from fresh demand, not to allow a sell-and-immediately-buy-back loop around the same window.

Can You Buy NSE Shares Now to Participate in the OFS?

No, not in the sense most people hope. Buying unlisted shares now does not create OFS eligibility if you missed the continuous-holding window described in press and expected in filings.

That does not mean unlisted NSE shares are meaningless. It means the investment case for buying today should not be anchored on "I will sell in the OFS" unless your holding history matches prospectus rules. If you are evaluating pre-IPO mechanics more broadly, read unlisted shares vs listed shares in India on Precize, then cross-check any name-specific rules in official documents.

What About Retail Participation in the IPO Later?

When an issue opens for public bidding, retail mechanics (UPI ASBA, categories, quotas) only become fully knowable from the RHP and final issue structure.

For now, keep two lanes separate:

OFS / EOI stage: for eligible existing shareholders to signal willingness to sell, not for random retail buyers to "join the OFS club" by purchasing unlisted shares yesterday.

IPO bidding later: a separate retail process if the issuer includes retail tranches in the final structure.

For intermediaries and process design (for example, reported banker roles), treat companion explainers as orientation, not a substitute for filings. Browse Precize IPO and markets insights for related reading as documents appear.

NSE IPO OFS Price Expectations: How to Read the Headlines

You will see very large rupee issue sizes and trillion-level valuation chatter in press and informal grey-market conversations. Use those numbers as context, not personal price targets. IPO GMP (grey market premium) chatter is sentiment, not a floor or ceiling for the listing price.

Until the DRHP and bookbuilding process:

Issue size and price band remain indicative at best.

Unlisted transaction prints can embed IPO optimism or liquidity discounts that do not equal the listing price.

A listed NSE is less "hyper-growth startup" and more "public-market accountability for core infrastructure," with returns tied to earnings, regulation, capital allocation, and how much scarcity value the market assigns.

Valuation risk: If the listing clears at a level the broader market refuses to sustain, downside exists even for a high-quality franchise.

Why the NSE Listing Still Matters for India Markets

NSE sits at the centre of market plumbing: listings, surveillance, indices, clearing and settlement linkages, and depth in derivatives. A public float changes disclosure cadence, index inclusion debates over time, and how global investors size India market infrastructure exposure.

Bankers and people familiar with the process discuss a very large IPO valuation range at the headline level. Again, those figures are a reminder that this is a systemically important listing where governance and regulatory history will be debated loudly, not a prompt to anchor a personal fair value on a headline alone.

Key Risks to Keep in Mind

Valuation risk: Unlisted markets can embed IPO expectations. If the listing clears at a valuation the market refuses to sustain, downside exists.

Process risk: EOIs, bookbuilding, and final sold quantities can differ from early headlines. Headline ₹20,000 crore stories are not contracts.

Liquidity and lock-ins: Reporting discusses lock-in concepts for certain unsold or remaining positions. Read the DRHP for the exact mechanism; do not assume you can exit instantly.

Governance memory: NSE's history includes serious regulatory episodes (including the co-location matter). Markets sometimes re-price governance risk at listing even when issues are largely in the past.

Conclusion

The NSE IPO OFS is shaping up to be one of the most significant capital market events in India's financial history. With board approval in place, investor outreach underway, and press citing deal sizes north of ₹20,000 crore, momentum is visible in headlines. Whether you are a retail investor, a pre-IPO participant, or a markets observer, the durable signal will be filings, not social threads.

Stay focused on DRHP updates and SEBI news. Those steps are what tell you the NSE IPO is moving from narrative to numbers.

Disclaimer: This article is informational, not investment, legal, or tax advice. Dates, sizes, and rules can change. Treat official letters to shareholders, the Draft Red Herring Prospectus (DRHP), and the final Red Herring Prospectus (RHP) as the only binding references.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved