OnEMI Technology IPO Analysis: Kissht, Mass-Market Credit, and What Filings Show

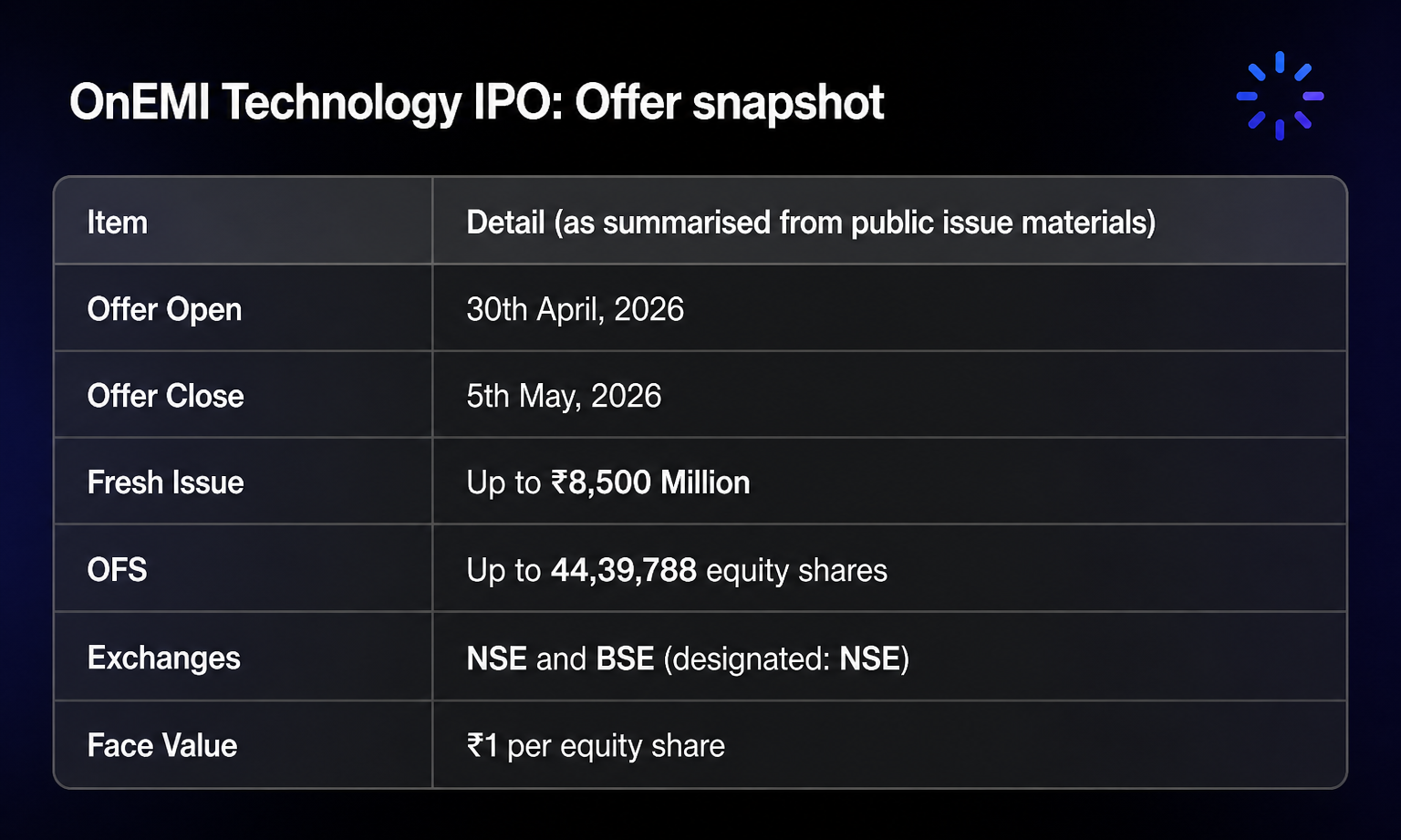

The OnEMI Technology IPO is the mainboard story behind the Kissht app-led lending franchise: The offer opens 30 April 2026, closes 5 May 2026, and combines a fresh issue of up to ₹8,500 million with an Offer For Sale (OFS) of up to 4,439,788 equity shares. NSE is the designated exchange, with a BSE listing alongside.

Quick glossary: AUM is assets under management (loans the platform manages or books, per filing definitions); PAT is profit after tax; OFS means existing investors sell shares; Gross NPA is stage-3 loans as a share of the book; PCR is how much of that stress is already provided for.

What is the OnEMI Technology IPO?

The OnEMI Technology IPO is a new listing for OnEMI Technology Solutions Limited, the company that operates the Kissht digital lending brand. Proceeds include fresh capital (up to ₹8,500 million) mainly to strengthen group funding for lending growth, plus an OFS tranche where selling shareholders monetize part of their holdings. The issue is intended for NSE and BSE; treat every number here as a summary until you confirm the final RHP and basis of allotment rules.

OnEMI Technology IPO: Offer snapshot

You are buying into a tech-led retail lender with a large registered user funnel and a mostly unsecured on-book story. The fresh issue matters for capital and growth; the OFS tells you existing owners are also taking liquidity off the table at the offer price.

What OnEMI (Kissht) actually sells

OnEMI Technology Solutions Limited runs a technology-enabled lending stack, with Kissht as the primary consumer-facing brand. The positioning is mass market: Households in roughly the ₹5 lakh–₹15 lakh annual income band (filings describe this band in lakhs of rupees per year), where formal credit penetration is still uneven.

As of 31 December 2025, filings cite about 63.73 million registered users and 11.17 million customers served. Distribution is deliberately multi-channel: digital acquisition, merchant tie-ups, and models such as credit QR that push origination closer to the checkout moment.

For investors, the product question is simple: Is this a scalable underwriting and collections machine with durable unit economics, or mainly a growth story riding benign credit cycles? The answer sits in vintage curves, funding cost, regulatory treatment of fees, and stress behaviour, not in headline user counts alone.

Financial Snapshot: Growth, Returns, and the Balance Sheet Story

Scale and growth

AUM ended 31 December 2025 at ₹59,557.53 million (about ₹5,956 crore if you prefer crore units).

AUM CAGR from 31 March 2023 to 31 March 2025 is stated at 79.53%. Fast CAGR from a smaller base often normalises as denominators rise, so track incremental growth and margins quarter to quarter after listing.

Profitability and returns

PAT for the nine months ended 31 December 2025: ₹1,992.69 million (about ₹199.3 crore).

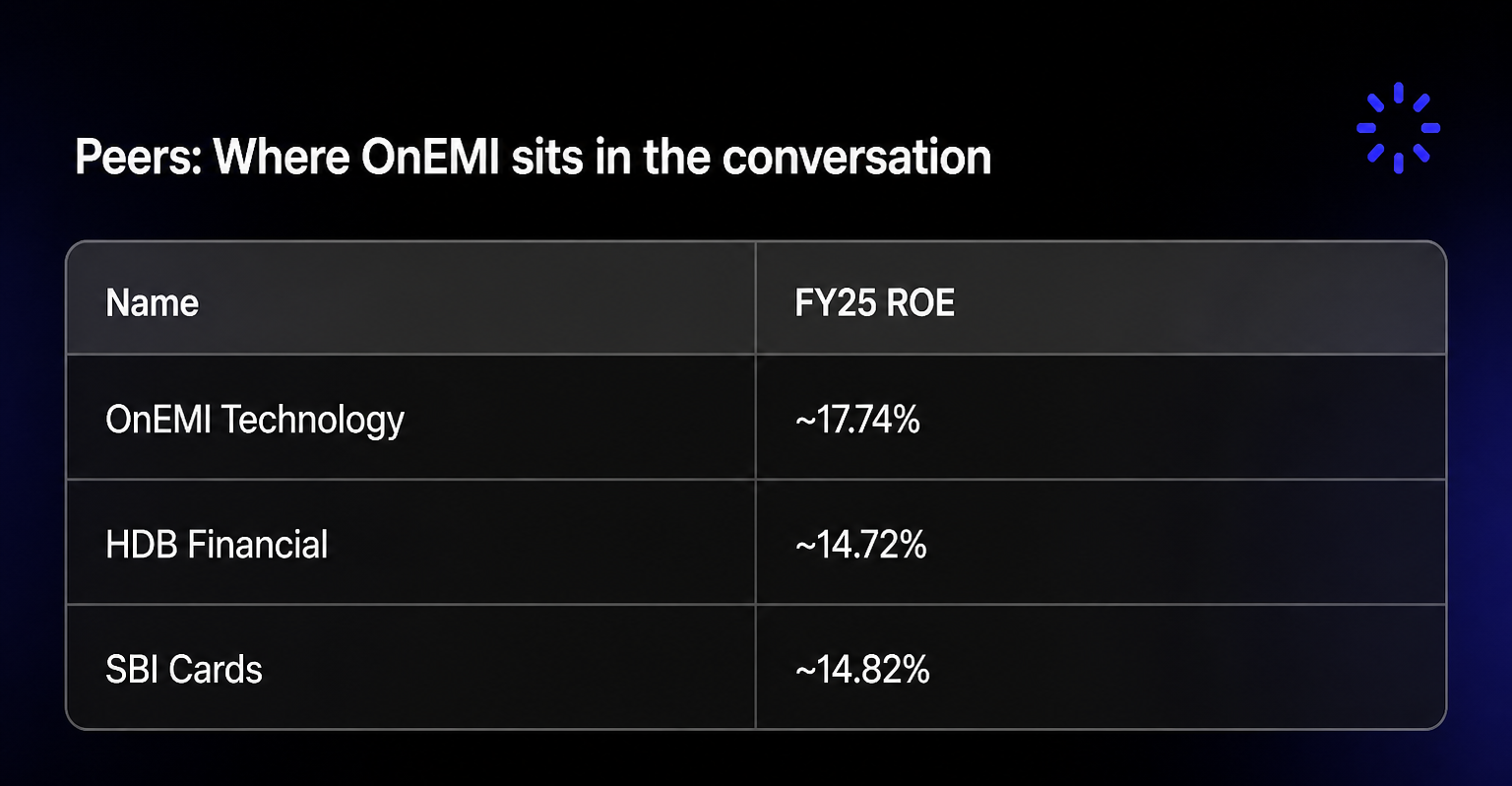

ROE is quoted at 23.51% on an annualised basis for that nine-month window. FY25 ROE in company peer disclosure is about 17.74%.

Asset quality

Gross NPA: 2.90% as of 31 December 2025.

PCR: 86.88% on the same date.

Those NPA and coverage prints look healthy relative to many retail lenders, but unsecured books can deteriorate quickly when employment and discretionary spend weaken, so read them alongside stage-2 trends, restructuring policy, and funding mix in the RHP.

Peers: Where OnEMI sits in the conversation

Listed NBFC and card names such as Bajaj Finance, HDB Financial, and SBI Cards are natural comparators for return ratios and valuation chatter, even though business mix differs.

Bajaj Finance remains the benchmark diversified retail lender by scale and market depth; OnEMI’s pitch is narrower: digital-first origination, sub-₹10 lakh ticket focus in practice for much of the book, and platform control from marketing to collections. Do not assume peer ROE alone implies peer multiples; risk weight, funding, and product mix must align.

Strengths that show up in filings

End-to-end tech: Cloud-native stack with in-house workflow across origination, underwriting, disbursement, and servicing, including model-driven credit decisions.

LAP as a diversifier: Loans against property were about 5.77% of AUM by December 2025, still small but directionally relevant if secured share rises over time.

Capital markets and brand cues: Vertex Growth Fund shows up in the cap table story, and Sachin Ramesh Tendulkar is linked to the brand as ambassador, which helps top-of-funnel recall but does not replace credit discipline.

Risks to weigh before you anchor a fair value

Unsecured dominance: About 94.23% of AUM is unsecured personal loans. That is expected for Kissht’s positioning, but it is also the first loss sleeve when liquidity tightens for households.

Operating cash flow: Rapid on-book expansion can produce negative operating cash flows in phases; that is not automatically “bad,” but it means you should read funding sources, ALM, and covenants carefully in the RHP.

Regulation and conduct risk: RBI rules on digital lending, pricing transparency, first-loss guarantees by LSPs, and collection conduct can move fees, growth, and distribution economics. Monitor circulars on RBI alongside SEBI listing conditions.

Concentration in growth: Very high historical CAGR invites mean reversion; your model should stress slower origination, wider credit costs, and higher funding rates.

Use of proceeds: Why the fresh issue matters

The fresh issue (up to ₹8,500 million) is described as being used in part to bolster capital at the lending subsidiary (Si Creva is named in this storyline as the regulated lending vehicle that needs equity headroom). Translate that into investor language: more Tier-1 style capacity to grow AUM and absorb regulatory buffers, assuming board and RBI approvals follow the stated plan.

Bottom line: A growth lender with a risk-first homework list

The OnEMI Technology IPO packages a high-growth Indian digital lending narrative with strong disclosed return ratios and NPA metrics that, on static data, look investment-grade relative to many fintech peers. The edge is distribution plus data-rich underwriting in a credit-thin income segment; the offset is unsecured dominance and regulatory path risk.

If you participate, build your view in three layers: (1) RHP numbers and assumptions, (2) peer multiples with mix-adjusted ROE, and (3) a stress case for unemployment and rates. For ongoing education on IPOs and investor rights, browse the Precize blog and FAQs; if you need platform help, use Precize Care.

To stay updated on the unlisted companies, join our community. For more market and unlisted education, see the Precize blog. If this article was useful, you can share it with other investors through the Precize referral program.

Disclaimer: This content is for informational purposes only and does not constitute investment advice. Investing in equities and IPOs involves risk of loss, including loss of capital. Read the RHP carefully, verify all figures against primary documents, and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results. Precize is not a stock exchange and is not regulated by SEBI.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved