Understanding Tax Implications on Buyback of Unlisted Shares

Running a private company in India and planning a buy-back of shares from investors may seem straightforward, but one important consideration is the tax on buy-back of shares of an unlisted company. This topic often causes confusion for business owners and shareholders, as the rules for unlisted companies differ from those for listed companies.

In this blog, you’ll walk through what a buyback of shares really means, and how the tax rules apply specifically to unlisted companies. You’ll also find out how the tax is calculated, the difference between buyback tax in listed vs. unlisted companies, and the pros and cons of buyback for unlisted firms.

Keep scrolling to learn properly!

Quick Overview

From 1 Oct 2024, the buyback amount is treated as a deemed dividend and taxed in the hands of shareholders at their income slab rate.

Shareholders cannot claim the cost of acquisition as a deduction, but it is treated as a capital loss for set-off against future capital gains.

Listed and unlisted companies now follow the same tax treatment for buybacks post-October 2024.

Platforms like Precize allow you to access unlisted shares, pre-IPO opportunities, and global trade finance options to build a diversified portfolio.

What is Buyback of Shares?

A buyback of shares simply means a company purchasing its own shares from its existing shareholders, often at a price higher than the original issue value or fair market value. Once these shares are bought back, they are cancelled, which reduces both the company’s share capital and the number of shares in circulation.

In India, the rules for buybacks are clearly laid out in the law. The main provision is Section 68 of the Companies Act, 2013, which allows a company to go ahead with a buyback if its articles of association permit it.

For listed companies, the process is guided by the SEBI (Buy-Back of Securities) Regulations, 2018, but for unlisted companies, the safeguards and procedures under the Companies Act still apply.

At the same time, Section 70 of the Act explains situations where a buyback is not allowed, such as when the company has pending defaults or tries to carry out the buyback through its subsidiary or an investment entity.

Once the concept of buyback is clear, the next step is to know the tax rules that apply, especially for unlisted companies.

Tax on Buyback of Shares of an Unlisted Company

When it comes to the tax on buyback of shares of an unlisted company, the rules are different depending on the date of the buyback. Here’s how the tax treatment works:

From 1 October 2024, India changed how buybacks are taxed. For any buyback done on or after 1 Oct 2024, the entire amount you receive from the company is treated as a deemed dividend in your hands under section 2(22)(f) and is taxed at your applicable slab rate.

No deductions are allowed against this income (section 57 updated). For capital-gains purposes, the “consideration” for the shares bought back is deemed nil, so you record a capital loss equal to your cost of acquisition (which you can set off/carry forward as per the capital-loss rules).

Companies must deduct TDS on such dividends (section 194 for residents; section 195 for non-residents, subject to treaty), but the old company-level buyback tax does not apply to buybacks on/after 1 Oct 2024.

After looking at the tax framework, let’s explore how the calculation of buyback tax is carried out in the case of unlisted companies.

Calculation of Buyback Tax in Unlisted Companies

When an unlisted company carries out a buyback, the tax used to be calculated on the distributed income, which is the variance between the buyback price and the initial issue price of the shares

Formula: Distributed Income = Buyback Price – Issue Price

For example, if the company had originally issued shares at ₹50 and later bought them back at ₹650, the distributed income per share would be ₹600.

[So, while the formula for calculating distributed income explains how the buyback tax worked earlier, after October 2024, the tax burden has shifted directly to the shareholder, making the calculation simpler but changing who bears the tax.]

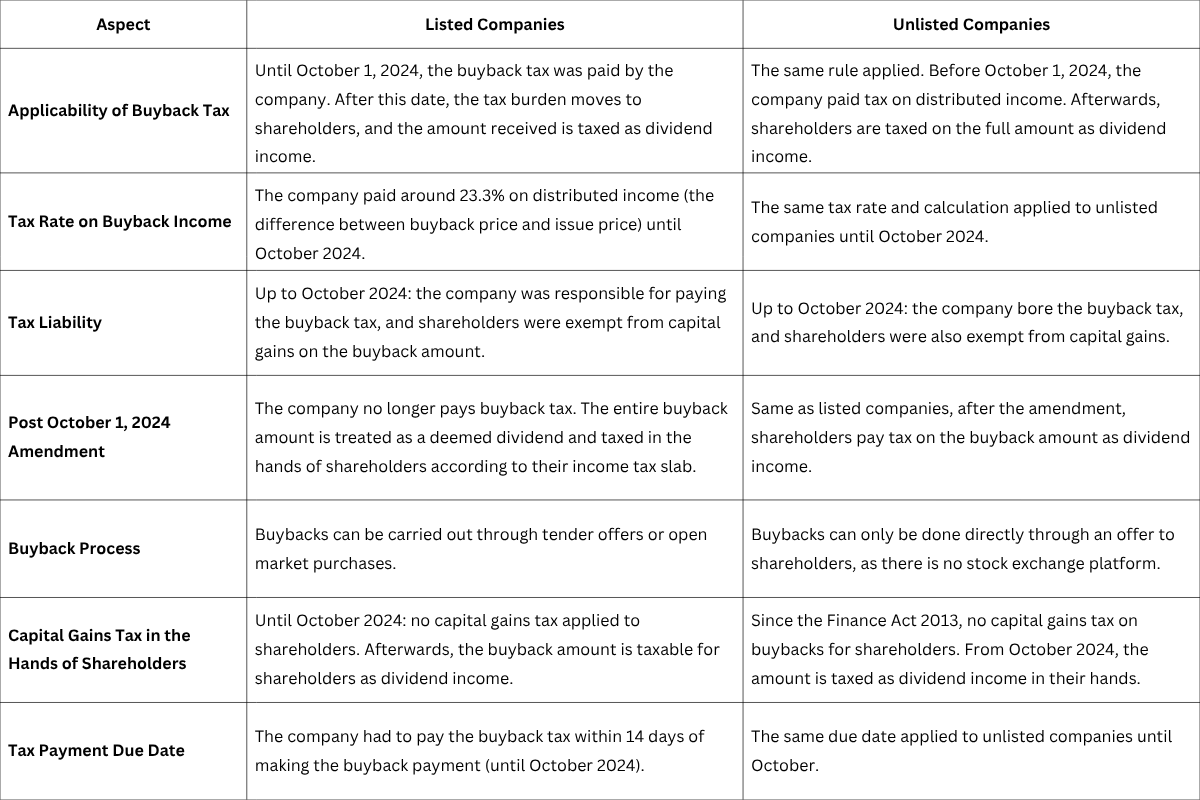

With the calculation process clear, let’s look at the key differences in buyback tax treatment between listed and unlisted companies.

Difference Between Buyback Tax in Listed vs. Unlisted Companies

The way the buyback tax is applied is not the same for listed and unlisted companies, though after October 1, 2024, both follow a similar rule where the tax liability shifts to shareholders. Here is how the treatment differs:

(Source: Tax Rate on Buyback Income)

Before wrapping up, it’s useful to weigh the potential benefits against the risks of a share buyback for unlisted companies.

Advantages & Disadvantages of Buyback for Unlisted Companies

Buyback of shares can offer several benefits to unlisted companies, but it also comes with certain challenges and risks. Understanding both sides helps you see the real impact of a buyback on the company as well as its shareholders.

Advantages

Buybacks can create several benefits for unlisted companies when managed well. Some of the key advantages include:

1. Better Use of Surplus Cash

Instead of leaving idle money in low-yield investments, unlisted companies often use buybacks to return cash to shareholders, a more efficient use of resources.

2. Stronger Financial Ratios

By reducing the number of shares in circulation, buybacks improve metrics like Earnings Per Share (EPS) and Return on Equity (ROE), which can enhance the company’s perceived financial health.

3. Positive Signal to Stakeholders

A buyback can send a message that management views the company as undervalued or confident about its future, helping build trust among shareholders or future investors.

4. Defense Against Hostile Takeovers

Unlisted companies can shrink the floating stock base, making it harder for unwanted shareholders or entities to gain control.

Disadvantages

At the same time, buybacks also come with certain challenges and risks that companies and shareholders should be aware of, such as:

1. Reduces Liquidity and Cash Reserves

Using substantial cash for buybacks means companies might lack funds during downturns or for urgent strategic needs.

2. Short-Term Focus Risk

It can create an artificial boost in EPS without actual business growth, potentially misleading stakeholders if the company isn't fundamentally strong.

3. Risk of Overvaluation

If shares are not truly undervalued, buybacks can destroy value rather than add it.

4. Missed Investment Opportunities

Funds used for buybacks could otherwise go into innovation, expansion, or debt reduction, potentially limiting future growth.

5. Potential Control Issues

There’s a risk that promoters could misuse buybacks to consolidate control or marginalize minority shareholders.

Conclusion

You’ve now seen how buybacks work for unlisted companies, the legal framework behind them, the tax rules before and after October 1, 2024, and the advantages and disadvantages that come with them.

The key takeaway is that the tax responsibility has shifted over time, from companies earlier paying buyback tax under Section 115QA, to shareholders now being taxed on the full buyback amount as a deemed dividend.

As you follow these changes, it’s also worth looking at platforms that give you access to broader opportunities in the private market.

Precize helps by facilitating investments in private companies, where you can buy and sell unlisted shares and even pre-IPO shares.

Along with this, Precize also offers access to unique global finance opportunities, giving you the ability to diversify with alternative fixed-income investments.

Reserve your access with Precize today and explore a more diversified portfolio!

FAQs

1. Do shareholders pay tax on the amount they receive from a buyback?

No, the money you received from a buyback during that period was completely exempt from tax in your hands. The tax liability rested only with the company, not the shareholders.

2. Can you adjust capital losses from the buyback?

You could not claim the cost of acquisition of those shares as a deduction against buyback proceeds. However, the difference was treated as a deemed capital loss, which you were allowed to set off against your future capital gains.

Disclaimer

The purpose of this article is to provide general insights and information; it is not a substitute for professional guidance on financial, tax, or legal matters. Tax laws and regulations can change, and their effect may differ based on individual situations. It is recommended to consult a professional before making any financial or tax-related decisions.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved