Ultimate Guide to Term Deposit: Features, Benefits, and Types

Starting to save is easy, picking where to park cash isn’t. Rate cards, payout choices, and break penalties can be confusing, so many default to the first deposit option available. A term deposit locks in your principal and rate for a specified tenure, making returns and cash flow predictable.

In FY25, bank deposits grew about 10–11% as savers moved to term deposits with 1–3 year rates at their peak. You can lock in from 7 days to 10 years, with typical tickets of ₹5,000–₹10,000 and interest either credited monthly/quarterly or rolled up to maturity. This fits safety-first savers, income planners, and near-term goals.

This blog covers how term deposits work, including interest credit vs. reinvest options, common tenures and ticket sizes, types to choose from, and a quick comparison framework to help you pick the right one.

Key Takeaways:

Term deposit meaning: You lock a fixed sum at a fixed rate for a set tenure; returns are predictable and set by compounding and payout mode.

Core rules: Compare effective yield (rate + compounding), check break penalties and partial closure, and know OD/lien options for cash without closing.

Types to pick: Cumulative vs non-cumulative, bank vs corporate, tax-saving 5-year, senior slabs, NRE/NRO/FCNR, and sweep/RD—match to goal, safety, and cash-flow needs.

How to choose: Stack offers on yield, break costs, issuer strength/DICGC, payout fit, tax/TDS, online ease, and tenure alignment.

Core Features and Rules of a Term Deposit

A term deposit sets a fixed rate for a fixed tenure, where your actual return depends on the compounding frequency and payout mode. Access to the deposit depends on the premature break rules or the availability of a loan/OD against it.

Administration covers nomination and joint modes, auto-renewal, and partial closure where offered, plus issuer fees and tax handling (TDS, 15G/15H). Some more key features include:

1. Interest rates, compounding, and EAY

Compare the effective annual yield, not just the headline rate. Compounding frequency and payout mode change the real return.

Rate card: Issuer quotes a nominal annual rate (e.g., 7.25%).

Compounding: Monthly, quarterly, half-yearly, or annual; more frequent compounding → higher EAY.

EAY formula: EAY = (1 + r/n)ⁿ − 1. Example: 7.25% with quarterly compounding ≈ 7.49%.

Displayed vs realised: Non-cumulative pays out interest and reduces compounding; cumulative reinvests and lifts maturity value.

Rate step-ups: Senior citizen or tenure slabs may add 0.25–0.75 percentage points; check rules.

2. Payout options

Pick a payout that matches your cash-flow needs. Reinvest when growth matters more than interim income.

Monthly / Quarterly / Half-yearly / Annual: Interest credits to bank on schedule; principal repaid at maturity.

On-maturity (cumulative): Interest compounds and pays with principal at the end.

Mandate changes: Many issuers allow changes only at renewal; confirm before booking.

3. Liquidity and premature withdrawal

Access depends on lock-in periods and penalty design. Break calculations usually use the run period, not the original tenure.

Lock-in window: Breaks may be disallowed for the first 7–90 days.

Penalty: Often 0.5–1.5 percentage points below the applicable run-period rate.

Run-period basis: Booked 24 months at 7.5% but exit at 11 months → paid at 11-month rate minus penalty.

Processing time: Banks 1–3 working days; corporate issuers can take longer.

Partial closure: Offered by select banks; minimum chunk size applies.

4. Loan or overdraft against a deposit

Raise cash without breaking the deposit by taking an OD against it. Pricing is a spread over your deposit rate.

LTV: Commonly 75–90% of principal; limits on cumulative FDs rise as interest accrues.

Pricing: Bank FDs often offer a card rate plus 1–2%; corporate FDs may route through NBFCs.

Turnaround: Same day within the same bank; T+1–T+3 for external or corporate deposits.

Charges: Processing, lien marking, and closure fees; ask for a schedule.

5. Nomination, joint modes, renewal, and closure

Set these at the opening to avoid friction later. Keep nominee, contact, and maturity instructions current.

Nomination: Single or multiple with percentages; update after life events.

Joint holding: Either or both survivors ease access, all holders must sign for changes.

Auto-renewal: Same tenure and payout by default unless you instruct otherwise.

Partial closure (where offered): Interest recalculated on the broken portion only.

Maturity instructions: Bank credit, renew principal only, or renew principal + interest.

6. Charges and operational fees

Small fees can erode net yield when you transact often. Read the tariff once before funding.

Premature break fee: Embedded via reduced rate or charged explicitly.

Duplicate advice/statement: Per request; often waived online.

Lien marking/removal: Fees apply for OD setup and closure.

Change requests: Bank change, name correction, revalidation, courier dispatch.

7. Tax basics

Interest is taxable at your slab; TDS affects cash flow, not total liability. File the right forms early to avoid unwanted deductions.

Interest as income: Taxed on accrual or credit per issuer policy.

TDS: Deducted when issuer thresholds are crossed in the year.

Form 15G/15H: Submit at the start of the year if eligible to avoid TDS.

Split planning: Multiple holders or PANs may alter TDS incidence but not slab taxation.

Also Read: Introduction to Types and Features of Fixed Income Investments

Popular Benefits and Use Cases of a Term Deposit

Term deposits protect your principal and give you predictable cash flows. You can use them to generate monthly or quarterly income, fund short-term goals, or park cash between investments with minimal effort.

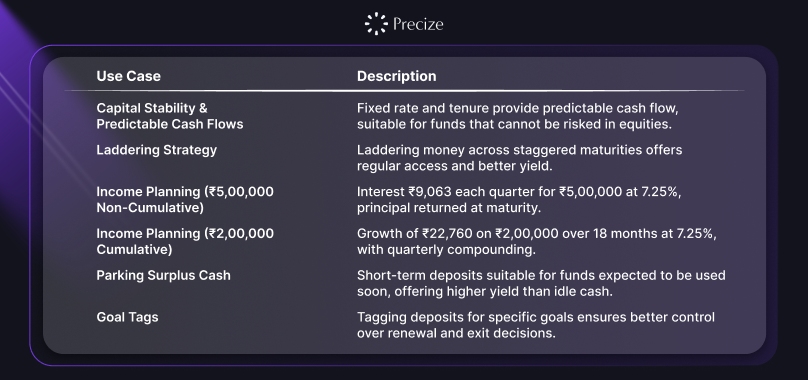

Capital Stability and Predictable Cash Flows

A fixed rate and fixed tenure remove return uncertainty. Cash hits your bank on a set schedule or at maturity.

Principal safety focus: Suits funds you cannot risk in equities.

Cash-flow control: Pick monthly/quarterly payouts for income, or cumulative to grow a lump sum.

Low admin: Standing instructions handle credits; keep the deposit advice for records.

Laddering Strategy

Splitting money across staggered maturities blends access with yield. A maturing rung can refill cash needs or be rolled at new rates.

Simple three-rung plan: 6, 12, and 18 months with equal amounts.

Rolling approach: On each maturity, reuse funds for a fresh 18-month rung if you don’t need cash.

Why it works: Regular access without breaking other deposits and losing rate.

Income Planning Examples

Payout mode decides whether you receive income during the term or at the end. Use these quick numbers as a guide.

₹5,00,000 non-cumulative at 7.25% (quarterly): Approx ₹9,063 interest each quarter; principal returns at maturity.

₹2,00,000 cumulative for 18 months at 7.25% (quarterly compounding): Maturity ≈ ₹2,22,760; growth ≈ ₹22,760.

Tip: Match payout dates to EMIs, rent, or school fees for smoother budgeting.

Parking Surplus Cash

Short tenures suit funds you expect to use soon. They reduce break penalties and keep options open.

When to pick short terms: Upcoming expenses within 3–6 months, or while waiting for an investment window.

Vs current/savings: Higher yield than idle balances; check notice periods and break rules.

Sweep link: If available, auto-sweep can move idle balances into short deposits and back on demand.

Goal Tags

Tie each deposit to a purpose so renewal and exit decisions stay simple. Write the goal in the deposit note if the bank allows it.

12-month fees: Quarterly payout to match the fee schedule.

Wedding in 2 years: Cumulative deposit that matures before the date.

Emergency buffer tranche: Several short rungs so one deposit matures every few months.

Looking beyond deposits? With Precize, you can add private equity through pre-IPO shares and private credit via short 30–60 day trade finance deals. Explore live opportunities and put idle cash to work with clear timelines.

Different Types of Term Deposits — What to Pick and Why

Picking the right term deposit comes down to what you need, growth or income, higher safety or higher yield, tax breaks, NRI repatriation, and day-to-day flexibility.

Below, we compare key variants, including cumulative vs. non-cumulative, bank vs. corporate, tax-saving 5-year plans, senior slabs, and sweep/RD options, so that you can match a product to your goal.

1. Cumulative vs Non-Cumulative

Pick between growth and periodic income. Cumulative reinvests interest while non-cumulative pays it out on a schedule.

Cumulative (growth): Interest compounds; you receive a lump sum at maturity. Suits goals with a date (fees in 18 months, wedding in 2 years).

Non-cumulative (income): Interest pays monthly/quarterly/half-yearly/annual; principal returns at maturity. Suits retirees or anyone planning regular cash flow.

Tax timing: Tax applies in the year interest accrues/credits; payout mode changes cash flow, not liability.

Break impact: Early closure on cumulative lowers realised yield; on non-cumulative, you keep payouts already received but rate may reset to the run period.

2. Standard Bank FD vs Corporate FD

Choose between stronger protection and higher yield. Bank FDs prioritise safety; corporate FDs aim to pay more for extra issuer risk.

Safety: Bank FDs carry DICGC cover up to ₹5 lakh per bank per depositor; corporate FDs rely on issuer strength and rating.

Yield: Corporate FDs usually quote higher rates for similar tenures; check rating, covenants, and past servicing.

Liquidity: Bank breaks are faster; corporate breaks can take longer and carry stricter penalties.

Use case: Emergency buffers and core cash suit bank FDs; surplus funds with strict issuer filters can consider corporate FDs.

3. Tax-saving 5-year deposit

Use this when you need an 80C deduction and can lock in for five years. It trades flexibility for a tax claim.

Lock-in: Premature break is not allowed except on death; loans/OD against deposit are typically not permitted.

Tax: You claim up to the 80C limit on principal, but interest is taxable at slab.

Payouts: Many banks offer cumulative and non-cumulative; pick per cash-flow need.

Fit: Good for salaried savers short of the 80C limit who want a bank product over market-linked options.

4. Senior Citizen / Super-Senior Variants

If you are eligible, take the rate add-on. Banks and issuers often run special slabs for 60+, sometimes higher for 80+.

Rate add-on: Commonly +0.25% to +0.75% over the card rate; confirm scheme window and caps.

Documents: Age proof at opening; nominee capture recommended.

Flex: Some schemes offer softer break penalties; read conditions.

Fit: Income planners who prefer non-cumulative payouts and guaranteed schedules.

5. NRE/NRO and FCNR deposits (for NRIs)

Match currency and repatriation needs. NRE and FCNR are fully repatriable while NRO has limits and Indian tax on interest.

Currency and tax:

NRE (INR): Repatriable principal + interest; interest tax-free in India for NRIs.

NRO (INR): Repatriation restricted; interest taxable in India.

FCNR (foreign currency): Repatriable; no INR FX risk on principal; interest tax-free in India for NRIs.

Rates and tenures: NRE/NRO follow INR rate cycles; FCNR follows the currency’s curve and bank funding costs.

Fit: Hold INR cash in NRE for higher INR rates; hold home-currency savings in FCNR to avoid FX swings.

6. Sweep / Auto-Sweep and Recurring Deposits

You may use sweep to earn more on idle balances. Use recurring deposits to build a corpus with fixed monthly instalments.

Sweep/auto-sweep: Savings balance above a threshold moves into short FDs and back on demand; you get FD-like rates on idle cash.

Recurring deposit (RD): You fix a monthly amount and tenure; interest compounds, and the sum pays at maturity.

Liquidity: Sweep breaks automatically when you debit the account; RD breaks attract penalties.

Fit: Sweep for day-to-day buffers; RD for disciplined saving when you can’t fund a lump-sum FD today.

Also Read: Personal Finance Guide: Importance, Core Areas & Essential Services

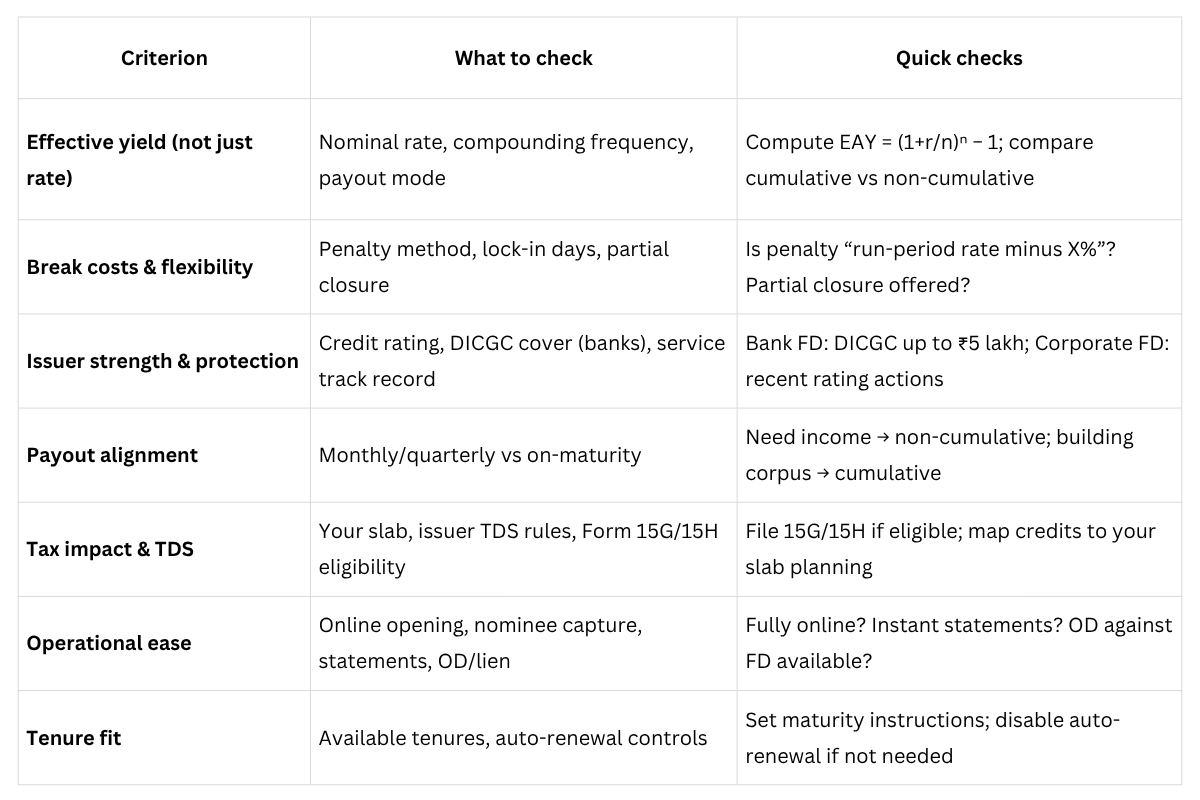

We’ll now stack offers by effective yield, break costs, issuer strength, payout alignment, tax treatment, ease of use, and tenure fit to make a clear choice.

Comparing Term Deposit Offers

Picking a term deposit isn’t just about the highest advertised rate. You need to see the effective yield after compounding and payout choices, check how costly it is to break early, and weigh the issuer’s strength and protections.

Let’s look at some quick checks to remember while picking a term deposit:

Also Read: Yield to Maturity (YTM): Components, Formula, Calculation & Pros

Challenges and Risks of Term Deposits to Keep in Mind

Term deposits may seem straightforward, but small details can significantly impact your results. Pay close attention to interest rate moves, early-break penalties, the issuer’s strength, and clauses that control access, renewals, and maturity handling.

The sections below highlight the key risks and how to manage them

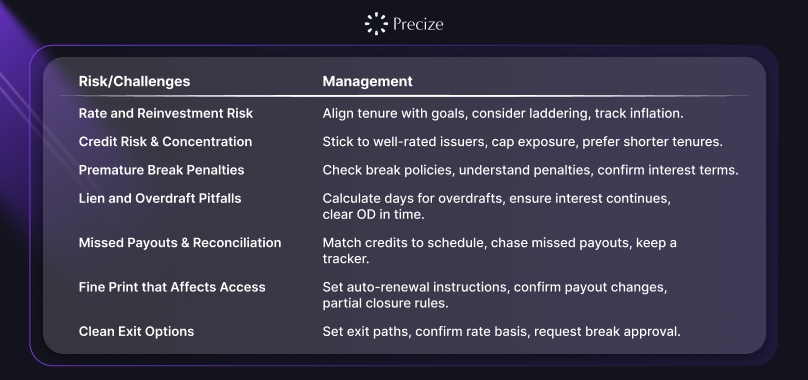

1. Rate and Reinvestment Risk

Falling rates at maturity can lower your next deposit’s return. Rising rates after you book a long tenure create opportunity cost until maturity.

Align tenure with goal dates to limit reinvestment timing risk.

Consider laddering so a portion re-prices sooner if rates move.

Track inflation to judge your real return after tax.

2. Credit Risk and Concentration

Bank FDs carry DICGC protection up to ₹5 lakh per bank per depositor. Corporate deposits depend on issuer strength and rating.

Stick to well rated issuers and scan recent rating actions.

Cap exposure per issuer and per group to avoid concentration.

Prefer shorter tenures when issuer transparency is limited.

3. Premature Break Penalties and Realised Yield

Early exit usually pays interest at the run period rate minus a penalty. The result can cut your annualised return sharply.

Method: If you booked 24 months at 7.5% and break at 11 months, the issuer may pay the 11-month card rate minus 1%.

Worked example: Principal ₹2,00,000. Run period 11 months. Run-period rate 6.5%. Penalty 1%. Payable rate 5.5%. Approx interest ≈ ₹2,00,000 × 5.5% × 11/12 ≈ ₹10,083.

Check if the issuer uses simple or compounded interest for breaks and whether any lock-in applies.

4. Lien and Overdraft Pitfalls

An overdraft against the deposit avoids a break but incurs additional costs. A lien can also block closure until the dues are cleared.

Pricing often sits at the deposit rate plus a spread. Calculate total days outstanding.

Confirm if interest on a cumulative FD continues to compound during the lien.

Clear the OD and obtain lien removal well before maturity to avoid delays.

5. Missed Payouts and Reconciliation

Operational errors can occur and often go unnoticed. Follow these points to avoid misses.

Match bank credits to the schedule and tick them off against the deposit advice.

Chase any missed payout within the same cycle so the issuer can reverse or credit promptly.

Keep deposit numbers, start dates, and maturity dates in a simple tracker.

6. Fine Print that Affects Access

Small clauses can change your experience more than the headline rate.

Auto-renewal can roll funds without notice if you do not set instructions.

Many issuers let you change payout mode only at renewal.

Partial closure is limited to select bank FDs and only in defined chunks.

7. Clean Exit Options

Set the exit path before you fund the deposit.

For early exit, place a break request and confirm the rate basis and penalty before approval.

For OD use, close the outstanding amount, get a no-dues update, then remove the lien.

Before maturity, set instructions to credit to bank, renew principal only, or renew principal and interest, and confirm the grace period.

Also Read: What is Repo Rate and Reverse Repo Rate: Importance and Differences

Conclusion

Term deposits give you capital stability and clean cash flows when you need certainty. If you’re also weighing options beyond bank rates, consider how a demat-backed plan and alternative fixed-tenor products can sit together.

Pre-IPO holdings reside in your demat account for long-term goals, while Precize’s global trade finance deals target fixed returns over short 30–60 day cycles and are managed on-platform. That mix can keep core money safe and put surplus cash to work with clear timelines.

At Precize, you can explore research-led opportunities across pre-IPO shares and short-cycle trade finance, start from ₹10,000, and track everything in one place.

Reserve access to buy and sell unlisted shares with Precize, India’s leading platform for pre-IPO investing.

FAQs

Q: How do banks actually calculate daily interest on a term deposit?

A: Most banks accrue interest on the end-of-day principal using the agreed rate and compounding schedule; credits post monthly/quarterly or at maturity. If you open mid-month, “broken-period” interest still accrues from day one. Statements show accruals even if cash isn’t paid out yet.

Q: What happens if my deposit matures on a weekend or bank holiday?

A: The deposit typically rolls to the next working day without action from you. Many banks pay interest for the extra days at the contracted rate until payout or renewal. Always set maturity instructions early so funds don’t auto-renew by default.

Q: Can I shift a term deposit from one bank/branch to another without breaking it?

A: Inter-bank transfers aren’t supported; you must close and rebook, which can trigger penalties and rate changes. Within the same bank, some branches allow a simple record move, but the deposit itself usually stays as is. Check if your goal date or payout mode would be affected.

Q: How does DICGC work if I hold multiple accounts or joint deposits?

A: Cover is ₹5 lakh per bank per depositor per ownership category (e.g., single, joint A+B, joint B+C). Spreading across different branches of the same bank doesn’t add cover; using another bank or a different ownership category can. Corporate deposits are outside DICGC.

Q: What if my PAN/Aadhaar or bank account changes during the tenure?

A: Update KYC and bank details with the issuer well before payout dates so TDS and credits map correctly. If TDS was cut under an old PAN or paid to a closed account, you can reconcile via revised details and your tax return, but it may delay refunds and credits.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved