Unlisted Shares vs Listed Shares: Where to focus in 2026

Listed vs Unlisted Shares India: How the two markets differ

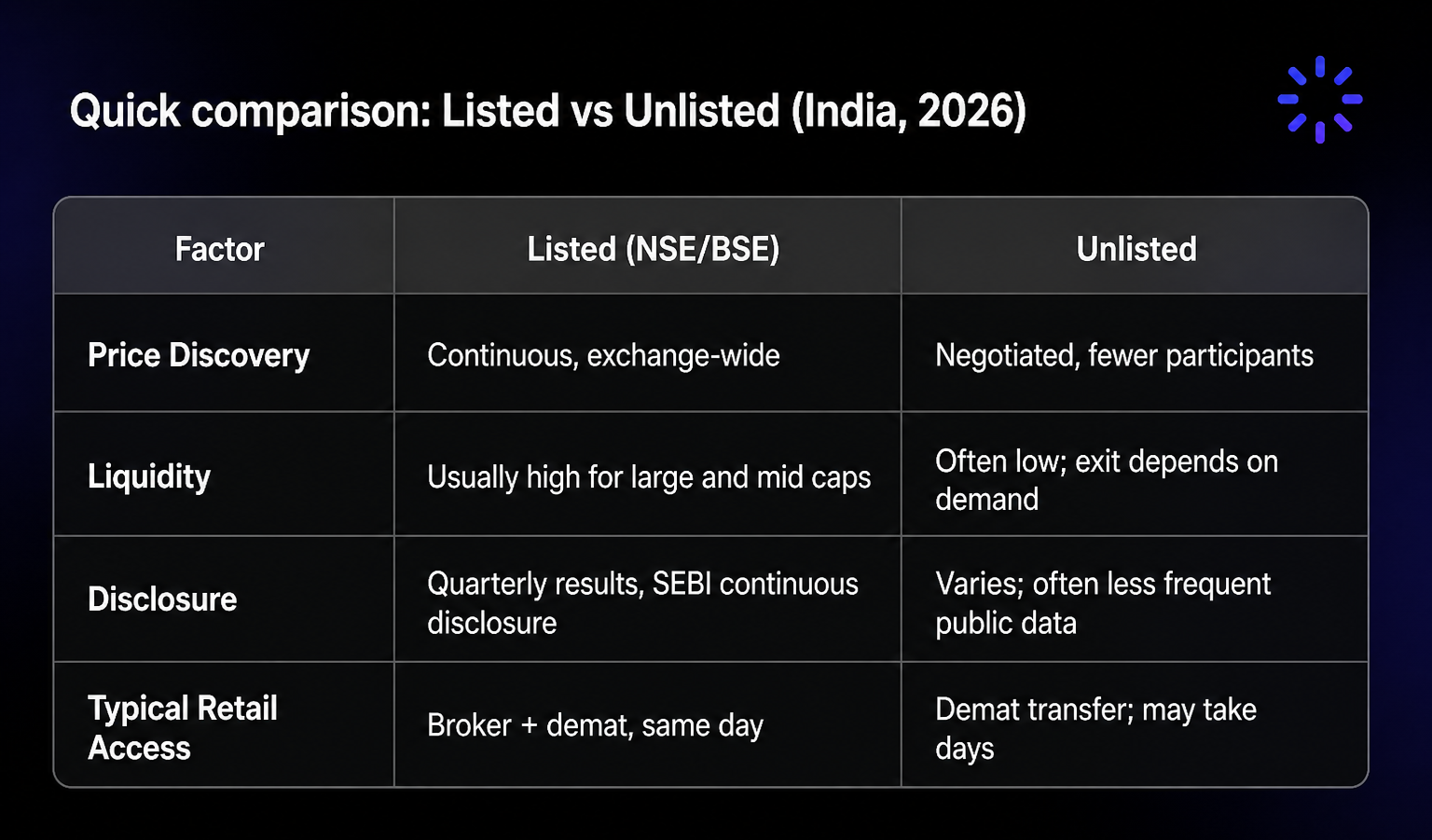

Listed shares are equities of companies that trade on recognised exchanges in India, mainly the National Stock Exchange (NSE) and BSE. Prices are discovered continuously during trading hours. The Securities and Exchange Board of India (SEBI) sets disclosure and conduct rules; for a listed investor’s view of rights and protections, SEBI’s investor resources are a useful baseline. For most retail and institutional investors, buying and selling is straightforward. Newer investors can also use the BSE investor section or the NSE website to understand how exchange-traded stocks are quoted and settled.

Unlisted shares are stakes in companies that are not listed or have chosen not to list yet. That basket includes pre-IPO names, subsidiaries of listed parents, mature private businesses, and backed startups. Deals happen off-exchange, often as demat transfers between parties, with platforms or brokers helping on price and paperwork.

Neither side “wins” by default. They fit different goals. Sensible allocation starts with where you sit on risk, return, and liquidity.

Quick comparison: Listed vs Unlisted (India, 2026)

The case for listed shares in 2026

Earnings are finding a floor

After several quarters of pressure, work such as J.P. Morgan Global Research points to MSCI India earnings growth in roughly the 13–16% range for the 2025–26 calendar year. That matters for listed vs unlisted shares India debates: For large caps—especially in areas helped by GST 2.0, tax relief–led consumption, and infrastructure spending—the setup into the second half of 2026 looks more constructive.

The Nifty 50 is up about 8% year-to-date in 2026, trailing Hong Kong’s Hang Seng (near 20%) and South Korea’s Kospi (close to 30%). Against improving domestic fundamentals, that gap reads more like selective value in Indian large caps than a wholesale bear case.

Liquidity is non-negotiable for many

You can often enter and exit the same day at an exchange-cleared price. That flexibility matters for rebalancing—especially if you also hold concentrated unlisted shares 2026 positions.

With crude volatility, Fed signalling, regional geopolitical noise, and US tariff uncertainty all live variables, a liquid listed sleeve is not a luxury; it is part of how you manage macro shocks.

Rules and data you can model

Listed firms face ongoing disclosure, quarterly numbers, and SEBI oversight. That cuts information gaps and supports frameworks—EPS, P/E, EV/EBITDA, ROE—that systematic investors rely on. For model-driven work, listed markets offer infrastructure that the unlisted share market India typically cannot match day to day.

Unlisted shares 2026: The case for a satellite sleeve

Pre-IPO upside can be real and checkable

The strongest draw for pre-IPO investment 2026 is not theory; it is history. Owners of unlisted NSE-related equity over the last couple of years have seen meaningful repricing (for example, levels around ₹1,950 with strong year-to-date moves into late 2025/early 2026), with IPO chatter rising after SEBI settlement news. Talk of a very large implied listing value illustrates the core idea: get exposure to strong economics before a potential public-market rerating.

When you are comparing names in the unlisted share market India, a systematic starting point is to screen unlisted companies and compare financials and peers before you trade on narrative alone.

Companies stay private longer

More Indian businesses from fintech to defence to sports are scaling before they list. If you only buy listed names, you may miss the early compounding phase. For best unlisted shares India–style opportunities, the first chapter of wealth creation increasingly plays out in private hands.

Themes the listed index underweights

The listed market tilts to financials, IT, energy, and staples. Unlisted exposure in 2026 can add defence and aerospace (for example, suppliers into programmes such as BrahMos, against a large defence budget), semiconductors (e.g. Polymatech), sports franchises (e.g. CSK), regional diagnostics, and exchange-style infrastructure (e.g. NCDEX). These are not small “diversifiers” only they are areas where the public market often lags the real economy.

The honest risk picture

Liquidity — You need a counterparty, a negotiated price, and transfer completion—sometimes days or weeks. This is not where you park money you might need on short notice.

Valuation — Without continuous trading, prices reflect a thin participant set and peer multiples. The deal price today may sit far from “fair value” in either direction.

Governance and disclosure — Unlisted issuers are not on the same continuous-disclosure treadmill. Diligence is on you: Financials, Sector Work, and a clear view on any IPO path. If lock-ins, transfer rules, or tax on unlisted sales are unclear, start with common investor questions on unlisted shares and still confirm details with your adviser.

Tax — Capital gains rules for unlisted shares differ from listed equity in timing and rates. Budgets move policy; a tax adviser should confirm your situation.

Grey-market hype — Not every hot unlisted name lists cleanly. Prices have run ahead of IPOs or opening prints, leaving peak buyers underwater. FOMO pricing is a documented failure mode—discipline matters.

A practical due diligence checklist (unlisted)

Financials — Audited statements where available; track record of revenue, margins, and cash conversion.

Cap table and instruments — Ordinary vs preference; any complex structures that change your economics at exit.

IPO or strategic path — Credible timeline or alternative liquidity (buyback, M&A), not just hope.

Peer valuation — Listed comparables and last round pricing; stress-test if the listing is delayed by years.

Documentation — Demat transfer, contract note, and alignment with what you were told verbally.

Macro: How 2026 tilts the split

Oil near $120 hurts input costs and household budgets for many listed stories. It can, at the same time, support themes such as defence-adjacent unlisted names (defence spending is a different macro channel) and contracted infrastructure revenue.

A hawkish Fed caps the odds of a broad, rate-driven rally in equities; rate-sensitive listed sectors (real estate, some NBFCs, discretionary) feel that. That can strengthen the relative case for unlisted names in structurally inelastic areas—if the thesis stands on its own.

A possible India–US trade deal, if it lands, could lift export-oriented listed sectors (IT, pharma, textiles, select manufacturing). For tactical listed exposure, that is a key catalyst to watch.

Domestically, GST 2.0 and prior income-tax relief can support consumption into H2 2026—helpful for consumer-facing listed names.

A simple allocation frame

Think complementary, not either/or.

Listed (core, roughly 60–80% of equity): Quality large caps in banking, IT, healthcare, and staples to ride the earnings normalisation. Use liquidity to tilt around the trade deal, Fed path, and oil. Mid and small caps can work in pockets but need sector conviction.

Unlisted (satellite, about 5–20% of equity, risk-dependent): Only where you can explain the investment without relying on “IPO will save me.” The IPO is a possible exit, not the thesis. Prefer moats, management, and capital allocation—think small private-equity sleeves. Funds and family offices evaluating larger tickets may also compare how institutional access to private markets fits their mandate rules and minimums differ from retail flows.

Sizing: A single unlisted line rarely deserves more than about 2–5% of total equity; illiquidity plus concentration is how serious damage happens.

Unlisted themes worth work in 2026

Market infrastructure — Exchanges, depositories, and clearing in a growing capital market. NSE is the headline; agricultural derivatives via NCDEX can be underdiscussed as ag modernises.

Defence and aerospace — Government is pushing more work to private players. Order book, balance sheet, and a credible path to listing can pair growth with discipline.

Regional healthcare — Diagnostics and specialty manufacturing outside top metros can be profitable, recurring, and cheaper than listed comps.

Fintech and lending — Select unlisted NBFCs, especially with strong listed parents, can offer credit growth at private-market pricing.

Bottom line

In 2026, the straight answer is both on purpose.

Listed markets give most investors the liquidity, transparency, and flexibility that should anchor a portfolio. The earnings path and a possible US–India trade outcome can make H2 2026 a window to add quality listed names on weakness.

Unlisted exposure can open India’s next wave of compounders only if you treat it like rigorous private investing: research, time horizon, and emotional control. It is not a shortcut around listed returns; it is a different risk–reward contract.

The investors who have done well in both places rarely mistook hype for analysis.

Research and next steps on Precize

Private markets reward the same habit as public markets: Clarity before commitment. On Precize, you can explore unlisted companies with screening and research suited to India’s unlisted universe then decide whether a name belongs in your satellite sleeve. Questions on process, eligibility, or account setup are best handled through Precize Care. To stay updated on the unlisted companies join Precize Community.

Disclaimer: This article reflects the author’s analytical views only and is not investment advice. Do your own diligence or speak to a SEBI-registered investment adviser before acting. Past performance of listed or unlisted instruments does not predict future results. Tax treatment of unlisted shares depends on your situation consult a qualified tax professional.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved