Unlisted Equity Shares Cost, Sale and Capital Gains Tax

Calculating the value of unlisted shares often feels confusing because there is no ready market price to rely on. Yet, getting it right is important since it directly affects taxation and capital gains. The challenge many face is knowing exactly how to calculate the unlisted equity share cost of acquisition and determine the correct sale value.

In this blog, you will learn what unlisted equity shares are, why the cost of acquisition and sale value matter, valuation methods, and the steps to calculate both. We will also cover common mistakes to avoid.

Let’s get into it!

What Are Unlisted Equity Shares?

Unlisted equity shares are shares of a company that are not traded on any stock exchange. Unlike listed shares, they don’t have a public market price, which can make understanding their value a bit tricky.

These shares are usually held by company founders, employees, or a select group of people. Since unlisted shares are not openly traded, their price depends on the company’s internal valuation, agreements between shareholders, or tax rules set by the government.

Before exploring numbers, it helps to understand why calculating the correct cost of acquisition and sale value is crucial once you hold unlisted shares.

Why Calculating Cost of Acquisition and Sale Value Matters

Calculating the cost of acquisition and sale value of unlisted shares is essential for understanding your taxable gains, ensuring compliance with Indian tax laws, and maintaining clear financial records. The following are the key reasons why this calculation matters:

1. Start with Compliance

The government requires you to calculate the cost of acquisition and the sale value to determine the correct taxable gain or loss for your transactions. This ensures you stay compliant with Indian tax laws.

2. Report Capital Gains Accurately

Having accurate numbers helps you report your capital gains and losses correctly in your income tax return, avoiding mistakes or penalties.

3. Separate Short-Term and Long-Term Gains

Knowing the correct cost of acquisition helps classify gains as short-term or long-term according to the holding period rules set by the Indian tax department.

4. Handle Multiple Purchase Dates or Prices

If the shares were acquired at different times or prices, proper calculation allows you to use methods like FIFO or average cost for fair reporting.

5. Maintain Clear Records

Keeping clear calculations and records is important for audits or future reference, especially if there are disputes or questions from tax authorities.

After knowing why precise calculation matters, understanding the valuation methods will help you determine the right figures for your unlisted shares.

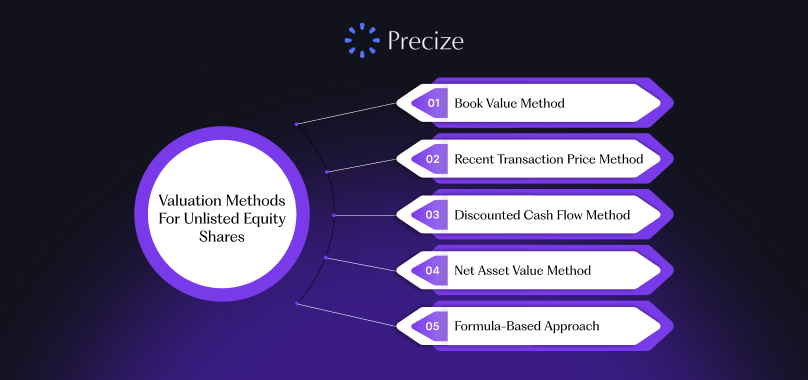

Valuation Methods for Unlisted Equity Shares

Since unlisted equity shares do not have a public market price, you need to use specific methods to determine their value. Here are the common approaches used in India:

1. Book Value Method

This method calculates the company’s value by subtracting total liabilities from total assets as recorded in the company’s books.

Formula: Company Value = Book Value of Assets − Book Value of Liabilities

Ensure that the asset values are updated regularly to reflect their true worth. This method works well when the company’s books accurately represent the real value of its assets.

Example: If a company has assets worth ₹10 crore and liabilities of ₹6 crore, the company’s value using this method is ₹4 crore.

2. Recent Transaction Price Method

If the shares were sold recently between unrelated parties in a fair transaction, that price can be used as the current value of the shares. This method is only useful if recent transaction data, usually within the past year, is available.

3. Discounted Cash Flow (DCF) Method

The DCF method estimates the value of a company by predicting its future profits and discounting them to present value using a rate that reflects risk and the time value of money.

This method requires detailed financial forecasts and works best for companies with stable earnings.

4. Net Asset Value (NAV) Method

NAV calculates the company’s value using the current market value of all assets minus liabilities. You can include or exclude intangible assets such as goodwill.

This method is particularly useful when asset prices are easily verifiable in the market.

Example: If the current market value of assets is ₹12 crore and liabilities are ₹7 crore, the NAV is ₹5 crore.

5. Formula-Based Approach (Tax Valuation)

For tax purposes under Indian rules (Rule 11UA), unlisted shares can be valued using either the NAV method or the Discounted Cash Flow method.

A qualified merchant banker usually does this valuation and ensures compliance with tax regulations.

After assessing the value of your unlisted shares, it’s important to calculate the cost of acquisition to understand your taxable gains clearly.

How to Calculate the Cost of Acquisition of Unlisted Equity Shares

To determine the correct capital gains tax on unlisted equity shares, it’s important to calculate the cost of acquisition accurately. Here are the key steps to follow:

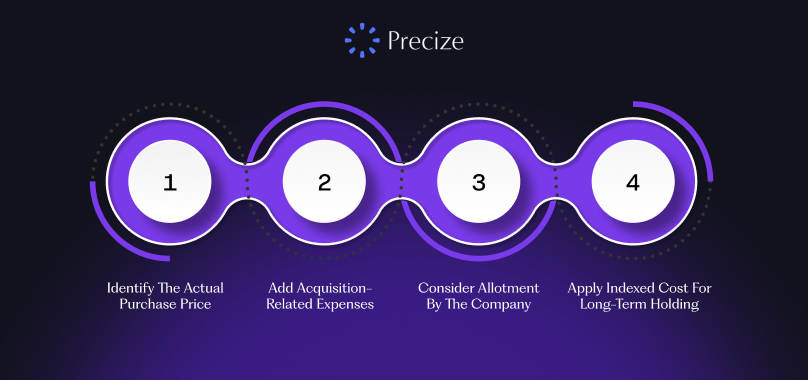

1. Steps to Calculate Cost of Acquisition

Identify the Actual Purchase Price: Start with the total amount you paid to acquire the unlisted shares. Multiply the price per share by the number of shares you purchased to get the base cost.

Add Acquisition-Related Expenses: Include any expenses directly associated with buying the shares, like brokerage fees, stamp duty, or legal costs. These expenses increase the total acquisition cost.

Consider Allotment by the Company (If Applicable): If the company allotted shares to you through a rights issue or as bonus shares, the acquisition cost may vary. For bonus shares, the cost is usually nil, while for rights shares, it is the amount you paid to acquire them.

Apply Indexed Cost for Long-Term Holding: If you hold unlisted shares for more than 24 months, they are treated as long-term assets. You can adjust the acquisition cost using the Cost Inflation Index (CII) to account for inflation, which reduces taxable gains.

2. Examples for Short-Term and Long-Term Holding

Short-Term Holding (Less than 24 Months)

Suppose you bought 100 unlisted shares for ₹10,000, including expenses, and sell them within a year for ₹15,000. The cost of acquisition remains ₹10,000.

Short-Term Capital Gain: ₹15,000 – ₹10,000 = ₹5,000, taxed according to your income tax slab.

Long-Term Holding (More than 24 Months)

If you purchased 100 shares for ₹10,000 two and a half years ago, and the Cost Inflation Index (CII) for the purchase year is 322 and for the sale year is 331:

Indexed Cost of Acquisition = 10,000 × (331 ÷ 322) = ₹10,280

If sold for ₹15,000, the long-term capital gain is ₹15,000 – ₹10,280 = ₹4,720, taxed at 12.5% without the indexation benefit.

Note: The Cost Inflation Index (CII) is published annually by the Income Tax Department to adjust asset prices for inflation.

With the acquisition cost clarified, you can now accurately calculate the sale value of unlisted equity shares.

How to Calculate Sale Consideration of Unlisted Equity Shares

When selling unlisted equity shares, calculating the sale consideration accurately is crucial for determining capital gains tax. In India, unlisted shares are those not traded on stock exchanges like NSE or BSE. Here is a 4-step process for calculating sale consideration, applicable for both short-term and long-term holdings.

Step 1: Identify the Actual Sale Price

Start by noting the price at which you are selling the shares. This is the price agreed between you and the buyer.

Step 2: Determine the Fair Market Value (FMV)

The FMV is the price at which shares would reasonably be sold between knowledgeable and willing buyers and sellers.

For unlisted shares, FMV is usually estimated by a merchant banker or calculated based on company valuation methods since there is no public market price.

If the actual sale price is below FMV, Section 50CA of the Income Tax Act states that FMV will be considered as the sale consideration for tax purposes.

Step 3: Compare Actual Sale Price with FMV

For tax calculation, the sale consideration is the higher of:

The actual sale price, or

The FMV on the date of transfer.

Step 4: Calculate Capital Gains

The type of capital gain depends on your holding period:

Short-Term Capital Gains (STCG)

STCG Formula: STCG = Sale Consideration − Cost of Acquisition − Any transfer-related expenses

Transfer-related expenses may include legal fees, documentation charges, valuation fees, or transaction facilitation costs.

Long-Term Capital Gains (LTCG)

First, calculate the Indexed Cost of Acquisition to adjust for inflation using the Cost Inflation Index (CII): Indexed Cost = Cost of Acquisition × (CII of sale year ÷ CII of purchase year)

LTCG Formula: LTCG = Sale Consideration − Indexed Cost of Acquisition − Any brokerage or related expenses

Example: Short-Term Capital Gains (STCG)

If you sell shares within 1 year, the profit is treated as short-term capital gain.

Let’s say, you bought 500 shares at ₹100 each in January 2025, total cost = ₹50,000

Sold in October 2025 for ₹140 per share → Actual sale value = ₹70,000

STCG: 70,000 − 50,000 = ₹20,000

This ₹20,000 is your return, and it is taxed at 20% as short-term capital gains.

Example: Long-Term Capital Gains (LTCG)

If you sell shares after 1 year, the profit is treated as long-term capital gain.

Let’s take the same example as above (STCG), but with different tenure.

Shares purchased in January 2025, sold in March 2026.

Purchase value = ₹50,000

Sale value = ₹70,000

LTCG = ₹20,000

Long-term capital gains are taxed at 12.5%, only if your total LTCG exceeds ₹1.25 lakh in a financial year.

If your total LTCG is below this limit, no tax is payable.

Simple Explanation:

Capital gains are the profit you make when you sell shares for more than you paid.

Capital Gain = Selling Price − Purchase Price

The tax you pay depends on how long you held the shares.

With the sale consideration figured out, keeping an eye on common errors can help you prevent unnecessary tax issues.

Common Mistakes to Avoid When Calculating Cost and Sale of Unlisted Shares

Errors in calculating the cost of acquisition or sale proceeds of unlisted shares can lead to wrong tax reporting and potential penalties. Here are the key mistakes to watch out for:

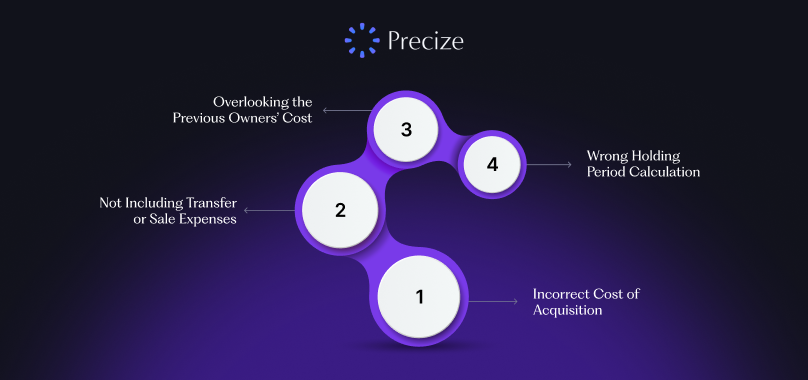

1. Incorrect Cost of Acquisition

Your cost should always include the actual price paid for the shares, along with any expenses directly related to the purchase. Using a wrong or estimated cost without proper evidence can create issues during tax assessments.

2. Not Including Transfer or Sale Expenses

Expenses directly incurred during the transfer or sale, such as brokerage or legal fees, must be deducted from the sale consideration. Overlooking these costs can unnecessarily raise the tax amount.

3. Wrong Holding Period Calculation

Whether your gains are classified as short-term/long-term depends on the holding period. Miscalculating this period can lead to the wrong tax rate being applied.

4. Overlooking the Previous Owners’ Cost in Certain Transfers

If you acquired shares through inheritance, gift, or company mergers/amalgamations, the acquisition cost is based on what the previous owner paid. Ignoring this can result in incorrect tax computation.

Conclusion

By now, you’ve seen how important it is to calculate the cost of acquisition and sale consideration of unlisted equity shares accurately. Keeping track of valuation methods, holding periods, and related expenses helps you avoid mistakes and ensures your capital gains are calculated correctly for tax purposes.

With Precize, you can easily handle transactions in private companies, including pre-IPO shares.

Reserve your access with Precize to take control of your unlisted shares today!

FAQs

1. Is Indexation Benefit Available for Unlisted Shares?

Yes, for long-term holdings, you can apply the CII to adjust the acquisition cost. This helps reduce taxable gains and ensures fair calculation of long-term capital gains tax.

2. What Happens if Shares Are Received by Gift or Inheritance?

When shares are received as a gift or through inheritance, the cost of acquisition is usually taken as the same as that of the previous owner. Tax rules may vary depending on the type of transfer.

3. Where Can You Find the CII Values?

The Income Tax Department releases the CII values for each financial year. These values are used to calculate the indexed cost of acquisition for long-term capital gains.

Disclaimer

This blog aims to explain key concepts and methods related to the valuation and taxation of unlisted equity shares in India. While every effort has been made to ensure accuracy, the content is for informational purposes only and does not replace professional guidance. Tax laws & regulations are subject to change, and your personal financial situation may require tailored advice. Always seek guidance from a certified tax consultant or financial expert before making decisions related to unlisted shares or capital gains.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved