How to Minimize Income Tax in New Regime

Tax season can often feel like a burden, but what if you could take control and minimize your tax liability under the new income tax regime? Whether you’re a salaried professional or a business owner, everyone wants to save some extra cash. The good news is, with a bit of planning, you can.

Since the introduction of the new income tax regime, many tax-saving opportunities have changed, but there are still ways for you to minimize your tax payments. In this blog, we’ll explore how to save income tax in the new regime, with practical strategies to help you optimize your finances and keep more of what you earn.

Key Takeaways

The new income tax regime offers lower tax rates but removes most exemptions and deductions.

Tax-saving strategies include optimizing income distribution, investing in tax-free options, and using tax-saving instruments like NPS.

Section 87A Rebate and certain allowances still offer tax relief under the new regime.

Avoid mistakes like ignoring tax-free income sources or failing to claim available rebates.

Tax-efficient planning is key: Diversify, invest for the long-term, and review your tax situation annually.

Understanding the New Tax Regime (Effective FY 2025–26)

The new income tax regime, introduced in 2020, was designed to offer lower tax rates and simplify the tax process by removing many exemptions and deductions. However, the tax structure has undergone significant updates in 2025, reintroducing certain benefits to make the system more appealing.

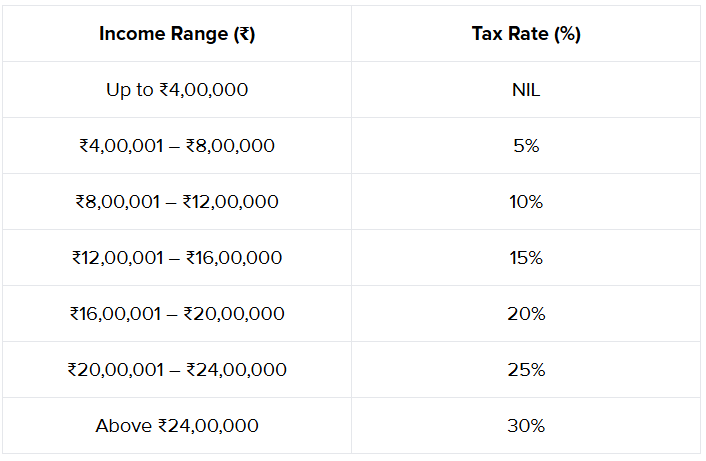

Updated Income Tax Slabs for FY 2025-26 (Assessment Year 2026-27)

Key Features of the Updated Tax Regime

Default Tax Regime: As per the Finance Act 2025, the new tax regime is now the default for taxpayers. However, individuals still have the option to choose the old tax regime if they find it more beneficial.

Section 87A Rebate: Increased to ₹60,000 for those with taxable income up to ₹12 lakh, making tax-free income more accessible.

Standard Deduction: Salaried individuals can continue to claim a standard deduction of ₹75,000, further reducing taxable income.

Employer Contributions to NPS: Employer contributions to the National Pension Scheme (NPS) are still deductible, allowing you to reduce your taxable income while saving for retirement.

Choosing the Right Tax Regime

Taxpayers can choose between the old and new regimes every financial year. While the new regime offers lower rates, it eliminates many exemptions and deductions available under the old system. The right choice depends on your individual financial situation, available exemptions, and how much you can benefit from the deductions under the old tax regime.

Now that you understand the basics of the new tax regime, let’s dive into how to save income tax under this system and what strategies you can use.

Strategies to Save Income Tax in the New Regime

The new tax regime may not offer the same deductions as the old one, but there are still effective strategies you can use to minimize your tax liability.

Let’s explore some of the best strategies to save income tax under the new regime.

1. Utilize the Tax Slabs Efficiently

One of the easiest ways to minimize your tax is by optimizing the income distribution within the tax slabs. The new regime comes with multiple tax slabs, and the key is to distribute your income wisely to stay in the lower brackets as much as possible.

How to do it:

Split your income between spouse or family members (if applicable) to stay below higher tax slabs.

Timing income realization effectively to avoid crossing the threshold of a higher tax slab.

Now that you know how to optimize your income within the slabs, let’s look at some tax-free income sources that can help you save even more.

2. Tax-Free Income Sources

Certain income sources are tax-free under the new regime, meaning you don’t have to worry about tax deductions on them.

Here are some examples:

Interest from Municipal Bonds

Income from PPF (Public Provident Fund)

Dividend from Indian Companies (up to a certain limit)

These tax-free income sources reduce your taxable income and help you save on tax while providing consistent returns.

Now that you know about tax-free sources, let’s explore tax-saving instruments that can still offer relief even under the new regime.

3. Tax-Saving Investments (Even in the New Regime)

While the new regime does away with most traditional tax-saving options, there are still a few investment routes that can reduce your taxable income. These options are not available in the old regime but can still provide substantial benefits:

National Pension Scheme (NPS): NPS remains one of the most effective tools for tax saving under the new regime. Under Section 80CCD(2), employer contributions to NPS are deductible, and these are not impacted by the shift to the new tax regime.

For government employees, employer contributions are deductible up to 14% of basic pay.

For others, employer contributions are deductible up to 10% of basic pay.

These contributions are beneficial and can help reduce your taxable income without impacting the simplicity of the new regime’s tax structure.

Please Note: If you are contributing individually to NPS, Section 80CCD(1B) provides an additional deduction of up to ₹2 lakh for your contributions. This is only applicable in the old tax regime, and under the new tax regime, you cannot claim this deduction for individual NPS contributions.

Voluntary Contributions to EPF (Employees’ Provident Fund): In addition to the mandatory contributions to EPF, you can also make voluntary contributions. These extra contributions are eligible for tax benefits under Section 80C of the Income Tax Act.

How it works: You can contribute more than the mandatory 12% of your basic salary to your EPF, and this extra amount is eligible for tax deduction, up to a maximum of ₹1.5 lakh per year under Section 80C.

Why it's beneficial: Voluntary contributions not only help you build a larger retirement corpus but also reduce your taxable income, making it a great way to save on taxes while securing your future.

The interest earned on EPF contributions is also tax-free, which adds to the overall benefit.

Tax-saving instruments can play a key role in lowering your taxable income. Next, let’s talk about rebates and exemptions that you can claim even in the new tax regime.

4. Standard Deduction

Under the new regime, salaried employees are allowed a standard deduction of ₹75,000 (up from ₹50,000 under the old regime). This deduction applies directly to your salary income and helps reduce your taxable income without the need for additional investments or documentation. It’s a straightforward way to save on taxes.

5. Home Loan Interest for Let-Out Property (Section 24)

Interest on home loans for let-out properties continues to be deductible without any upper limit under the new regime, providing a significant benefit for property owners who earn rental income. This allows you to reduce your taxable income by claiming a deduction on the full interest paid on your loan.

6. Section 87A Rebate

Under Section 87A, taxpayers with taxable income of less than ₹12 lakh are eligible for a rebate of up to ₹60,000. This rebate can effectively reduce your overall tax liability to zero, offering a huge advantage for low-income earners.

With the right strategies, you can definitely reduce your taxable income under the new tax regime. It’s important to plan ahead, utilize these benefits, and consider long-term tax-saving investments to optimize your financial situation. Now, let’s look at mistakes to avoid when filing your taxes in the new regime.

Also Read: Understanding the HRA Exemption in the New Tax Regime

Avoid Common Tax Mistakes in the New Regime

While it’s important to save taxes, it’s equally crucial to avoid common mistakes that could backfire:

1. Skipping Research on Tax Regimes

Not understanding the new tax regime thoroughly can lead you to make the wrong choice. Many taxpayers still opt for the old regime without evaluating the new one properly, which may not always be the best option.

2. Not Timing Your Income Properly

In the new regime, timing your income effectively can make a significant difference. For example, deferring income to a later financial year could keep you in a lower tax slab, reducing your tax liability.

3. Ignoring Tax-Free Sources of Income

Many people overlook tax-free income sources like municipal bonds and dividends from tax-exempt companies. These can help reduce your taxable income, but many taxpayers forget to include them in their planning.

4. Failing to Claim Exemptions and Rebates

Even under the new regime, some exemptions (like Section 87A) and rebates are still available. Not claiming them can unnecessarily increase your tax burden.

5. Underestimating the Impact of Fees and Charges

Ignoring the impact of brokerage fees, administrative charges, and other expenses can lead to higher-than-expected tax liabilities. Always consider these costs when calculating your potential savings.

With these tax-saving strategies and common mistakes in mind, let’s now focus on how you can make tax-efficient financial planning for the future.

Tax-Optimized Financial Planning for the Future

Planning ahead is important to reduce your taxes in the long run. Tax-efficient financial planning allows you to make the most of your investments, protect your wealth, and minimize your tax liabilities.

Let's discuss how you can build a tax-optimized portfolio for the future.

1. Diversify Your Investments

Balance your portfolio with a mix of stocks and bonds. Include tax-saving options like PPF or NPS for stability and tax benefits.

2. Invest for the Long-Term

Investing in ELSS or NPS helps you build wealth and save on taxes over the long run, giving you both growth and tax relief.

3. Review Your Tax Situation Annually

Check your finances every year to make sure you’re on track with your tax-saving plans. Tax laws change, so staying updated can help you save more.

By building a tax-efficient portfolio and keeping these strategies in mind, you can minimize your income tax and maximize your returns.

Conclusion

The new income tax regime might seem complex at first, but with the right approach, you can save income tax efficiently. By understanding the new tax slabs, using tax-free income sources, investing in tax-saving instruments, and claiming rebates, you can significantly reduce your tax burden.

The key is to plan early, stay informed, and ensure you’re taking full advantage of the options available to you under the new regime.

Tax planning is important, but so is building long-term wealth. At Precize, we help you access exclusive alternative investments like unlisted pre-IPO shares and private credit deals that can complement your tax strategy and grow your portfolio.

Start investing with Precize today and take a smarter step toward financial efficiency in 2025.

FAQs

What are the key differences between the old and new tax regimes?

The new tax regime provides lower tax rates but eliminates many exemptions and deductions that were available under the old system.

Can I claim deductions under both tax regimes?

No, you must choose either the old or the new regime, and deductions are available only under the old regime.

How do I decide which tax regime is better for me?

The choice depends on your income, available exemptions, and deductions. Use a tax calculator or consult a professional to make an informed decision.

What are the common tax-saving instruments available in the new regime?

NPS and voluntary EPF contributions are popular choices for saving taxes under the new regime.

Can I save taxes on my rental income in the new regime?

Yes, some allowances like HRA can still provide relief on rental income, depending on your circumstances.

Disclaimer

This blog is for informational purposes only and not to be considered as professional tax or financial advice. Always consult with a qualified tax advisor to understand the best tax-saving strategies for your specific financial situation. Precize is not responsible for any financial decisions made based on this information.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved