Understanding Working Capital Gap and Its Limitations

India’s GDP grew 7.8% year-over-year in FY25/26, yet many businesses still face cash shortages and funding bottlenecks. MSMEs, which contribute 30% of GDP and 45% of exports, often operate with a significant working capital gap, which affects their daily operations and financial stability.

A working capital gap occurs when short-term liabilities exceed short-term assets, creating a cash flow mismatch. This gap can lead to production delays, stalled deliveries, and administrative difficulties. For retail participants exploring pre-IPO opportunities or institutional analysts reviewing private credit deals, understanding this gap reveals hidden operational risks and financial constraints.

In this blog, you’ll learn what causes working capital gaps, their limitations, and practical strategies businesses use to maintain liquidity and operational stability.

Key Highlights

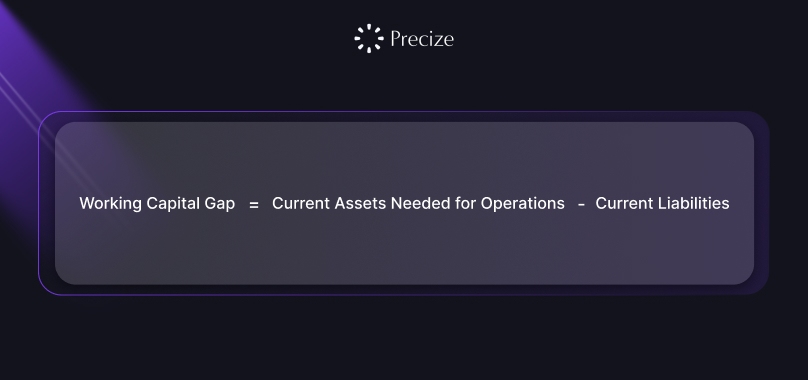

Working Capital Gap: The difference between current assets and liabilities needed for daily operations.

Key Causes: Delayed customer payments, strict supplier terms, high inventory, operational inefficiencies, and market volatility.

Measurement Methods: Operating cycle, cash conversion cycle, balance sheet analysis, fund flow tracking, and liquidity ratios.

Management Strategies: Optimise receivables, negotiate supplier terms, control expenses, implement digital workflows, and use short-term financing.

Operational Impact: Production delays, disrupted deliveries, higher borrowing costs, limited scalability, and reduced customer trust.

What is Working Capital Gap?

The Working Capital Gap refers to the shortfall between a company’s current assets and its current liabilities, which are required to fund its day-to-day operations. In simpler terms, it’s the period during which a company needs cash to bridge the difference between paying suppliers and receiving payments from customers.

Formula:

Example: If a company needs ₹50 lakh to maintain inventory and receivables, but only has ₹30 lakh in short-term payables, the gap is ₹20 lakh.

Now that you know what the working capital gap truly represents, it becomes easier to explore why this gap appears in the first place. That brings us to the next part.

Factors Contributing to a Working Capital Gap

A company’s working capital gap doesn’t arise randomly. It results from a combination of operational, financial, and market dynamics that affect the timing of cash inflows and outflows. Understanding these factors is crucial for anticipating liquidity pressures and planning short-term financing effectively.

Long Credit Periods to Customers: Extending credit helps attract and retain clients, but it delays cash inflows, increasing the working capital gap.

Short Credit Periods from Suppliers: When suppliers demand faster payments, businesses must release cash quickly, creating immediate liquidity pressure.

High Inventory Levels: Excess inventory ties up cash in storage, logistics, and insurance costs, rather than being available for operational needs.

Seasonal Fluctuations: Industries with cyclical demand, such as textiles, FMCG, or tourism, face irregular cash cycles, which widens the working capital gap during peak seasons.

Rapid Growth: Fast expansion necessitates higher expenditures on raw materials, staffing, marketing, and infrastructure, temporarily widening the cash gap.

Workflow Inefficiencies: Poor procurement planning, inaccurate demand forecasting, or inconsistent customer management stretches working capital cycles and increases financing costs.

Also Read: Types, Uses and Benefits of Working Capital

These factors determine how efficiently cash moves through a business. Identifying and managing them proactively reduces reliance on external financing, lowers costs, and ensures smooth operations. With these factors in mind, let’s proceed to the limitations companies encounter when managing their working capital gap.

Limitations of Working Capital Gap Management

Even with proactive strategies, companies face inherent challenges in managing working capital. These limitations affect liquidity, workflow efficiency, and overall financial stability. Below are the key constraints that businesses commonly encounter, along with specific examples that illustrate their impact.

1. Unpredictable Customer Payments

Delayed payments, billing disputes, and inconsistent CRM entries can create sudden cash shortages, making short-term planning unreliable.

Example: An Indian IT services company delivering a project milestone may wait 45-60 days for payment from a large corporate client. During this period, the firm may rely on internal cash to cover salaries and vendor payments.

Impact: Businesses may struggle to maintain smooth operations during these gaps, particularly in sectors with tight margins.

2. Dependency on Supplier Terms

Companies rarely have complete control over supplier credit policies, especially smaller Indian firms negotiating with large vendors. Stringent supplier terms can compress the cash cycle.

Example: A SaaS startup that pays cloud hosting and software licencing fees upfront, while clients are billed quarterly, may experience cash flow strain.

Impact: Reliance on supplier flexibility introduces risk, as unfavourable changes can worsen the working capital gap immediately.

3. Limited Access to Short-Term Funding

MSMEs and smaller firms often face difficulties in accessing low-cost, short-term working capital loans or lines of credit. Traditional banks may impose high collateral requirements or slow processing times.

Example: An IT services firm expanding into new enterprise accounts may need short-term capital to onboard staff and invest in infrastructure. Slow bank approvals can delay project execution, affecting timelines and cash flow.

Impact: Restricted access to financing increases vulnerability to operational shocks and can amplify liquidity pressure.

4. Administrative Overload and Manual Processes

Manual reconciliations, paper-based approvals, and fragmented reporting hinder decision-making and often cause miscalculations of capital requirements.

Example: A SaaS or IT firm relying on Excel sheets to track hundreds of invoices may misalign receivables and payables, inadvertently widening the gap.

Impact: Inefficient processes reduce responsiveness, making it harder to adjust to sudden cash flow changes.

5. Market Volatility and External Shocks

Seasonal demand shifts, client budget changes, or industry-wide disruptions can upset even well-planned cash cycles.

Example: An IT services company may face delayed contract renewals or unexpected client budget cuts, resulting in temporary cash shortages despite maintaining disciplined internal operations.

Impact: Even firms with disciplined internal processes can experience liquidity stress, highlighting the importance of contingency planning.

Together, these limitations highlight why managing the working capital gap is both a financial and operational priority for Indian SaaS and IT firms. Proactive monitoring, process automation, and flexible financing are crucial for maintaining liquidity and sustaining growth.

Now that you understand the limitations, the next logical step is to learn how businesses identify and precisely calculate the gap.

Methods for Identifying and Calculating the Working Capital Gap

Companies typically measure working capital gaps using structured financial methods that help assess liquidity, workflow efficiency, and cash flow health. Each approach offers a distinct perspective on how cash flows through a business and identifies areas where shortfalls may occur.

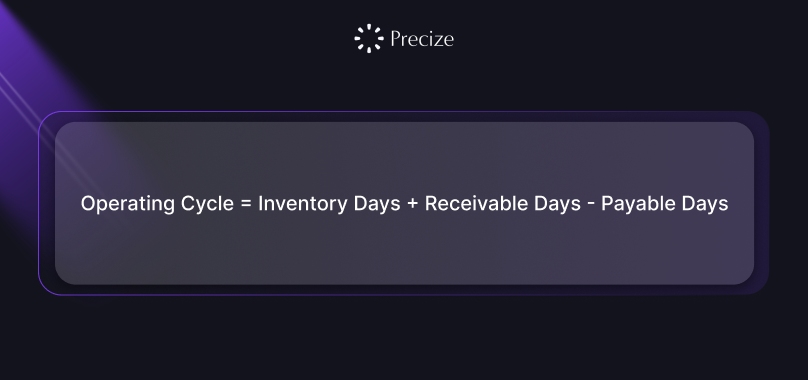

1. Operating Cycle Method

The operating cycle shows how long cash remains invested in day-to-day operations. For SaaS and IT services, it reflects project milestone payments, licence purchases, and cloud resource expenses relative to client collections.

Formula:

Components:

Inventory Days: Average number of days your resources or licences are held.

Receivable Days: Average time it takes to collect payments from clients.

Payable Days: Average time you take to pay vendors.

Represents: The total duration your cash remains invested in operations before returning as liquid funds.

Relevance: By looking at the operating cycle, you can see how long a company’s cash stays tied up in operations. Longer cycles may indicate higher working capital requirements, which could affect short-term liquidity.

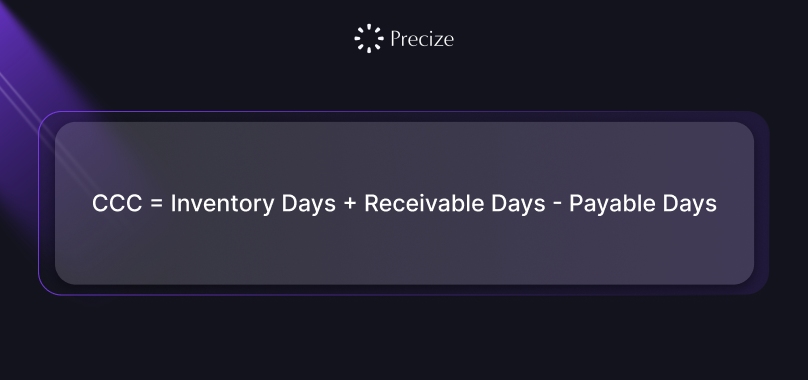

2. Cash Conversion Cycle (CCC)

The operating cycle shows how long cash remains invested in day-to-day operations. For SaaS and IT services, it reflects project milestone payments, licence purchases, and cloud resource expenses relative to client collections.

Formula:

Components:

Inventory Days: Average number of days your resources or licences are held.

Receivable Days: Average time it takes to collect payments from clients.

Payable Days: Average time you take to pay vendors.

Represents: How quickly your invested resources are converted back into cash.

Relevance: The CCC shows how efficiently a company turns resources into cash. A shorter cycle suggests faster liquidity generation and lower reliance on external financing.

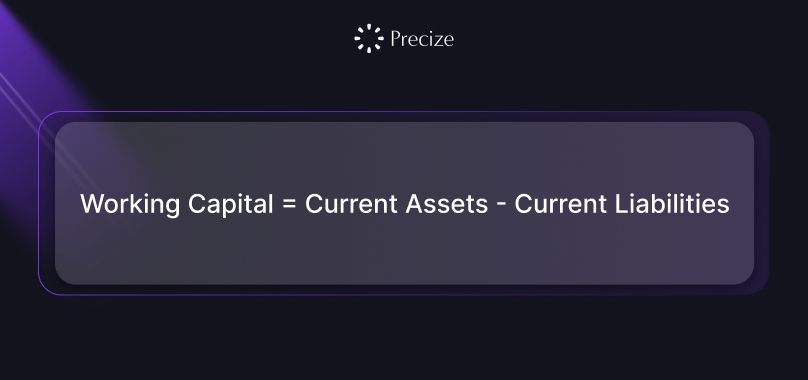

3. Balance Sheet Analysis

Comparing current assets and liabilities provides a snapshot of short-term liquidity. This simple method helps spot funding gaps that require immediate attention.

Formula:

Components:

Current Assets: Cash, accounts receivable, and short-term investments available to fund operations.

Current Liabilities: Accounts payable, accrued expenses, and short-term debt you need to settle.

Represents: The surplus or shortfall of your short-term assets relative to liabilities, showing whether you have enough liquidity to cover immediate obligations.

Relevance: Comparing current assets and liabilities helps you spot immediate liquidity gaps. This tells you whether the company can comfortably meet its short-term obligations.

4. Fund Flow Analysis

Fund flow analysis tracks cash inflows and outflows over time. For IT and SaaS companies, it uncovers temporary gaps caused by delayed client payments or upfront vendor expenditures.

Formula:

Components:

Cash Inflows: Payments received from clients, investors, or other operational sources.

Cash Outflows: Expenses such as payroll, vendor payments, and operational costs.

Represents: The mismatches between cash coming in and cash going out, showing where temporary shortfalls may occur.

Relevance: Tracking cash inflows and outflows reveals periods of temporary shortage. It highlights potential operational bottlenecks that might impact the company’s ability to sustain operations smoothly.

5. Ratio Analysis

Ratios provide a quick view of liquidity efficiency and working capital utilisation. They allow easy comparison across companies.

Formulas & Components:

Current Ratio:

Represents: Your ability to cover short-term obligations with available assets.

Quick Ratio:

Represents: Immediate liquidity available without relying on inventory sales.

Working Capital Turnover Ratio:

Represents: How efficiently you are using your working capital to generate revenue.

Relevance: Liquidity and efficiency ratios provide a quick view of a company's financial health. They let you compare companies, identify potential risks, and make more informed investment decisions.

Each of these methods gives you a clear perspective on where cash is tied up and for how long. However, identifying the gap is only the first step; actionable strategies are required to bridge it effectively, which we will explore in the next section.

Also Read: Gross Working Capital: Importance, Formula, & Example, Difference from Net Working Capital

Strategies to Manage and Mitigate Working Capital Gaps

A company that actively manages its working capital is better positioned to maintain steady cash flow, reduce reliance on external borrowing, and sustain operations during volatile periods. Understanding these strategies can help you evaluate which companies are more likely to deliver consistent returns and withstand short-term financial pressures.

1. Tightening Receivables Management

Faster and predictable collections reduce the gap between revenue recognition and actual cash availability. Companies implement this using automated reminders, early payment discounts, and clean, up-to-date CRM systems.

Why it matters to you: Firms with effective receivables management are less likely to face cash crunches, making their financial performance more predictable and less risky for your investments.

2. Negotiating Better Supplier Terms

Extending payable periods while maintaining good supplier relationships aligns cash inflows with outflows. Favourable supplier terms reduce the need for short-term borrowing.

Why it matters to you: Companies that manage supplier payments strategically demonstrate stronger liquidity control, which can be an important signal of operational stability for investors.

3. Inventory Optimisation

By using demand forecasting, just-in-time practices, or resource planning, companies minimise excess inventory or unused software and licences, freeing up cash without disrupting operations.

Why it matters to you: Efficient inventory management indicates that the company is using capital wisely, reducing risks of operational bottlenecks and improving the potential for steady returns.

4. Digital Workflows to Reduce Administrative Load

Automated invoicing, integrated financial reporting, and digital approvals reduce errors and speed up decision-making.

Why it matters to you: Companies leveraging digital workflows can respond faster to cash flow fluctuations, ensuring smoother operations and signalling better financial governance.

5. Expense Controls

Prioritising high-return expenditures while trimming non-essential costs preserves working capital and ensures funds are available for critical operations or growth initiatives.

Why it matters to you: Companies with disciplined expense management are more resilient, giving you confidence that your investment is being handled prudently.

6. Short-Term Financing Options

Structured solutions, such as trade finance, invoice discounting, or supply chain financing, provide quick liquidity when internal cash is insufficient.

Why it matters to you: Access to short-term financing ensures companies can bridge temporary cash gaps without disrupting operations, protecting your investment value.

Failing to manage working capital gaps can lead to operational disruptions, delayed payments, and increased borrowing costs. By analysing how companies implement these strategies, you can make more informed investment decisions, assess liquidity risk, and more accurately gauge their long-term financial stability.

Impact of Working Capital Gap on Business Operations

A persistent working capital gap can significantly disrupt a company’s day-to-day operations and long-term growth. For investors, understanding these operational impacts helps gauge the company’s liquidity risk and resilience.

Production Slowdowns: Insufficient cash to procure raw materials or resources can halt production or delay project execution.

Delayed Deliveries: Limited liquidity may disrupt the supply chain, causing delayed shipments or service fulfilment, which can affect revenue timing.

Higher Borrowing Costs: Companies relying on short-term emergency funding incur additional interest and fees, reducing profitability and overall financial efficiency.

Reduced Scalability: Cash constraints make it difficult to take on large orders, expand capacity, or invest in growth initiatives.

Loss of Customer Trust: Delays in delivery or service fulfilment can erode client confidence and damage the brand, with long-term revenue implications.

Understanding the consequences makes the importance of solutions even more relevant. And that brings us to practical options companies use to strengthen their working capital cycle.

Solutions to Address and Overcome Working Capital Gaps

Companies use a combination of financial and operational solutions to close working capital gaps. The right approach depends on business size, industry, and growth plans. Understanding these solutions helps evaluate a company’s liquidity management and operational resilience.

Invoice Discounting: Receivables are converted into upfront cash, giving businesses faster access to funds without waiting for client payments. This ensures smoother cash flow and reduces short-term liquidity pressure.

Supply Chain Financing: Suppliers receive prompt payment while buyers settle later, aligning cash inflows and outflows efficiently. This helps maintain operational continuity without straining internal cash reserves.

Trade Finance: For businesses dealing with international suppliers or clients, trade finance bridges gaps in global supply cycles and mitigates cross-border payment delays, ensuring uninterrupted operations.

Credit Lines and Short-Term Funding: Banks and NBFCs offer flexible working capital support customised to operational cycles, enabling companies to cover temporary cash shortfalls without disrupting day-to-day operations.

Automation Tools: Digital solutions such as cleaner CRM data, automated reminders, and integrated dashboards reduce manual effort, improve accuracy, and accelerate decision-making, enabling proactive working capital management.

Solutions like these enable businesses to maintain continuity, optimise cash cycles, and reduce operational risks. Let’s now summarise the complete picture, tying it back to your exploration journey.

Conclusion

Understanding the working capital gap shows how businesses manage short-term operations. It helps retail investors, analysts, and advisors assess a company’s discipline, resilience, and scalability. As more Indian companies adopt structured solutions such as supply chain finance and trade finance, this knowledge enables better-informed decisions in the private market.

If you’re looking for deeper insights beyond basic financial metrics, Precize offers access to private equity and private credit opportunities in India. It also provides detailed research reports, including balance sheets, cash flow statements, income statements, and peer comparisons, helping you make informed, data-driven investment decisions.

Reserve your access with Precize today and start building a diversified portfolio!

FAQs

1. How can seasonal businesses prepare for recurring working capital gaps?

A. They can plan cash reserves during low-demand periods, use short-term credit lines, and adjust inventory levels to match peak and off-peak cycles.

2. Can technology adoption reduce the working capital gap?

A. Yes, automation in invoicing, payments, and CRM tracking speeds up collections and reduces manual errors, improving cash flow predictability.

3. How do client contract structures impact working capital gaps?

A. Milestone-based or delayed payment contracts extend receivable cycles, requiring firms to fund operations internally until payments are received.

4. Are there industry-specific indicators for working capital stress in IT/SaaS firms?

A. Indicators include rising unpaid invoices, extended subscription collections, overstocked software licences, and increasing reliance on short-term financing.

5. Can a working capital gap affect a company’s credit rating?

A. Persistent gaps may increase dependence on credit, higher interest costs, and late payments, potentially impacting creditworthiness and financing terms.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved