Financial Services Unlisted Shares - Top NBFC and AMC Before IPO

The financial services unlisted shares investors are tracking in India include NBFC names such as Hero FinCorp, Hinduja Leyland Finance, InCred Holdings, Arohan Financial Services, and ICL Fincorp, along with AMC and wealth-management names such as PPFAS, SBI Funds Management, and ASK Investment Managers. These are research ideas, not buy recommendations. Each company needs a separate check on valuation, liquidity, disclosures, asset quality, and IPO visibility.

For investors, the attraction is clear: financial services unlisted shares can offer access before a public listing. The risk is also clear: these shares are harder to sell, harder to value, and often come with less public information than listed companies.

What Are Financial Services Unlisted Shares?

Financial services unlisted shares are shares of private financial companies that are not listed on stock exchanges such as NSE or BSE. These companies may operate in lending, mutual funds, wealth management, insurance distribution, stockbroking, fintech, or investment advisory services.

In simple terms, you are buying into a financial business before it becomes publicly traded. That can create early-access potential, but it also means lower liquidity, fewer public disclosures, and more dependence on private-market pricing.

Why Financial Services Unlisted Shares Are in Focus

Financial services unlisted shares are gaining attention because India's household financial behaviour is changing. More investors are using demat accounts, systematic investment plans, digital lending apps, wealth platforms, and alternative investment products.

That creates two broad investment themes.

First, credit demand remains large. Retail borrowers, small businesses, vehicle buyers, rural households, and self-employed customers all need financing. Non-banking financial companies, or NBFCs, often serve borrowers and use cases that banks may not prioritise.

Second, India's savings are becoming more financialised. Mutual funds, portfolio management services, and alternative investment funds are becoming more familiar to investors who previously relied mostly on fixed deposits, real estate, and gold.

The asset management theme is supported by industry data. AMFI data for April 2026 showed Indian mutual fund industry net AUM at around ₹81.92 lakh crore, with monthly SIP inflows of about ₹31,115 crore. You can review industry-level updates on the AMFI website.

However, sector growth does not automatically make every unlisted company attractive. Price, business quality, governance, and exit timing still matter.

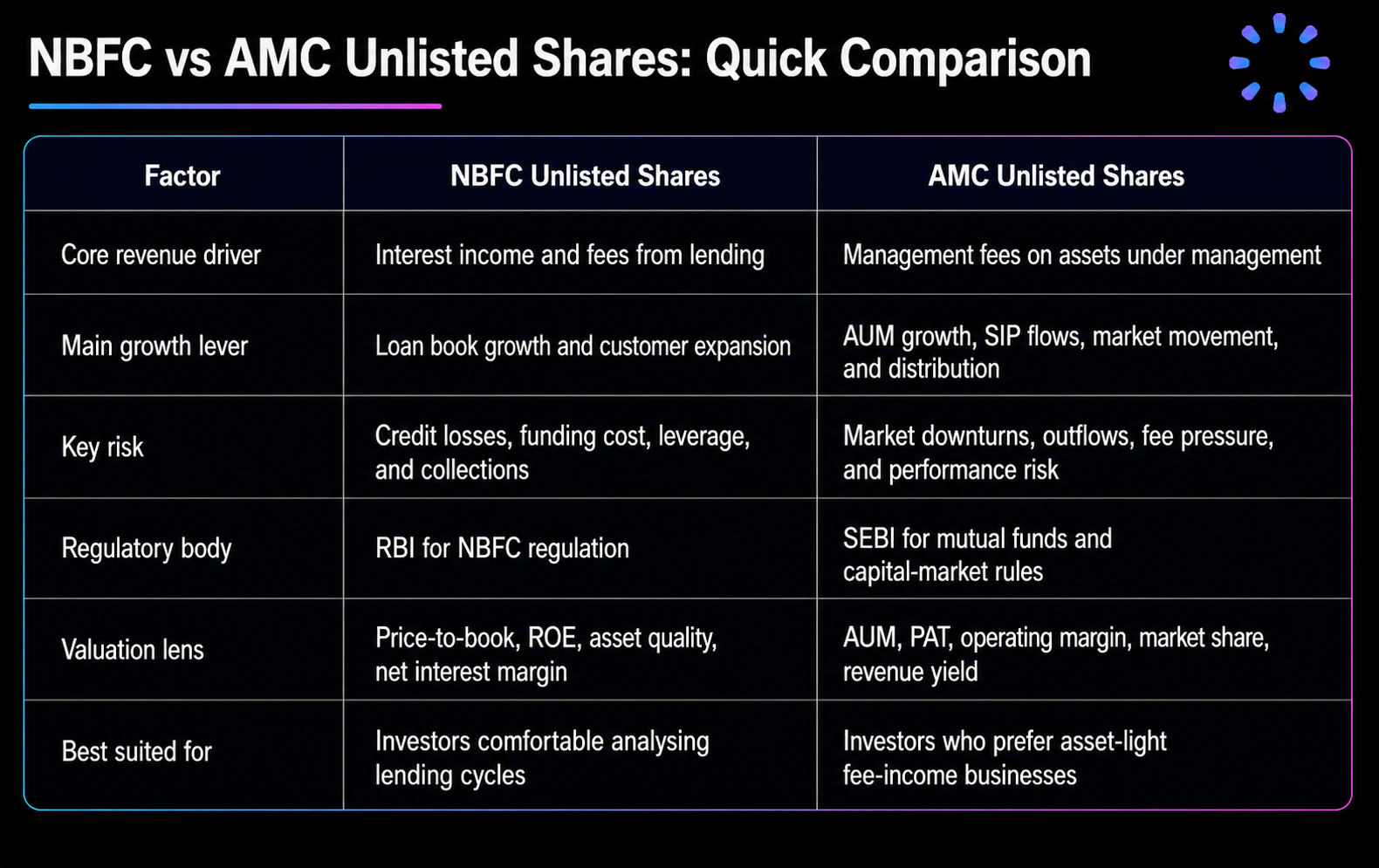

NBFC vs AMC Unlisted Shares: Quick Comparison

NBFCs and AMCs both sit inside financial services, but they are very different businesses. A lender takes credit risk. An asset manager earns fees for managing money.

For NBFC regulation, investors should track the Reserve Bank of India. For IPO filings and public issue documents, check SEBI public issue filings.

Top NBFC Unlisted Shares Before IPO

The NBFC names below are not ranked recommendations. They are widely discussed because they connect to large financial themes such as vehicle finance, consumer credit, MSME lending, microfinance, secured lending, and digital underwriting.

1. Hero FinCorp Unlisted Shares

Hero FinCorp is one of India's most tracked NBFC unlisted shares because of its Hero Group association, lending scale, and IPO pathway. The company operates across two-wheeler loans, personal loans, SME finance, loan against property, and other retail and commercial lending products.

Hero FinCorp has public IPO visibility. The company filed draft IPO documents in 2024, and public reports in 2025 said SEBI issued final observations for a proposed ₹3,668 crore IPO. The structure included a fresh issue and an offer for sale, though final pricing and listing dates depend on market conditions and updated offer documents.

For a deeper company-specific update, read Precize's note on Hero FinCorp IPO details.

Why investors track Hero FinCorp:

Strong brand association with the Hero ecosystem.

Diversified lending book across retail and MSME segments.

Potential capital raise through IPO, subject to final launch.

Exposure to vehicle finance, consumer lending, and small business credit.

Large addressable market in urban, semi-urban, and rural India.

Key risks to evaluate:

Asset quality and gross non-performing asset trends.

Profitability recovery if credit costs or funding costs rise.

High leverage, which is normal for lenders but still needs monitoring.

Valuation risk if private-market pricing assumes a smooth IPO.

NBFC regulatory changes and capital requirements.

Hero FinCorp is a good example of why investors should not look at IPO expectation alone. The better question is whether the lending book, capital position, and valuation support the investment case.

2. Hinduja Leyland Finance Unlisted Shares

Hinduja Leyland Finance is an NBFC focused on vehicle finance and allied lending products. Its association with the Ashok Leyland ecosystem gives it relevance in commercial vehicle financing, used vehicle loans, SME lending, and related retail finance segments.

Vehicle finance can benefit when logistics activity, infrastructure spending, and fleet replacement cycles improve. At the same time, it is cyclical. A slowdown in freight, higher fuel costs, weak borrower income, or lower used vehicle resale values can affect repayment behaviour.

Why investors track Hinduja Leyland Finance:

Strong positioning in vehicle and commercial transport finance.

Linkage to the broader Hinduja and Ashok Leyland ecosystem.

Opportunity from logistics, road transport, and used vehicle financing.

Reach across semi-urban and rural borrower segments.

Potential operating leverage if loan growth and collections remain healthy.

Key risks to evaluate:

Commercial vehicle cycles can be volatile.

Borrower stress can rise during economic slowdowns.

Used vehicle collateral values can fluctuate.

Funding cost changes can affect lending spreads.

IPO timing may remain uncertain until formal filings or announcements are available.

Investors comparing Hinduja Leyland Finance with other NBFC unlisted shares should pay close attention to collection efficiency and segment-level asset quality.

3. InCred Holdings Unlisted Shares

InCred Holdings has become one of the more visible financial services unlisted shares because it combines consumer lending, education loans, SME finance, wealth, and technology-led underwriting.

The InCred Holdings IPO context is stronger than many private names. Public reports in 2026 said InCred Holdings received SEBI approval and later filed updated draft IPO documents. The proposed IPO reportedly includes a fresh issue of up to ₹1,250 crore and an offer for sale by existing shareholders, with proceeds expected to support capital at InCred Financial Services.

For a fuller filing-led view, read Precize's guide to the Incred Holdings UDRHP.

Why investors track InCred Holdings:

Technology-led underwriting and digital loan origination.

Exposure to consumer, education, and SME credit.

Public IPO-related milestones and stronger market visibility.

Diversified financial services ecosystem beyond lending.

Institutional investor backing and experienced leadership.

Key risks to evaluate:

Digital lending rules and regulatory scrutiny.

Credit quality in unsecured and semi-secured lending segments.

Competition from banks, fintechs, and large NBFCs.

Valuation risk if growth expectations are too aggressive.

Final IPO timing, pricing, and dilution details.

InCred's investment case depends on whether it can scale lending without letting credit costs outrun revenue growth.

4. Arohan Financial Services Unlisted Shares

Arohan Financial Services is a microfinance-focused NBFC that serves underserved borrower segments, including rural households, women entrepreneurs, and small businesses.

Microfinance has a powerful inclusion story. It helps borrowers access small-ticket credit for working capital, household income generation, and local business needs. But it is also sensitive to rural cash flows, local disruptions, political pressure, and borrower over-indebtedness.

Why investors track Arohan Financial Services:

Clear financial inclusion theme.

Exposure to rural and semi-urban credit demand.

Focus on borrowers underserved by traditional banking.

Branch-led customer reach in underpenetrated regions.

Potential long-term demand for small-ticket credit.

Key risks to evaluate:

Collection volatility during regional stress.

Borrower concentration in specific geographies or income groups.

Regulatory caps, conduct rules, and pricing changes in microfinance.

Higher operating intensity than purely digital lending models.

Sensitivity to monsoon, inflation, and local employment cycles.

Microfinance can compound well when underwriting is disciplined. It can also deteriorate quickly when borrower stress spreads across a region.

5. ICL Fincorp Unlisted Shares

ICL Fincorp is a diversified financial services company known for secured lending products such as gold loans, along with other lending and investment-related services.

Gold loans are attractive because they are backed by collateral and can be disbursed quickly. They also serve customers who need short-term liquidity but may not qualify easily for unsecured credit. However, secured lending is not risk-free.

Why investors track ICL Fincorp:

Exposure to the secured lending and gold loan market.

Demand for small-ticket, short-tenure credit.

Regional customer base with scope for expansion.

Collateral-backed lending model.

Potential to deepen product offerings over time.

Key risks to evaluate:

Gold price volatility and loan-to-value discipline.

Regional concentration.

Competition from banks, large gold-loan NBFCs, and local financiers.

Operational controls around collateral storage and auctions.

Lower public disclosure compared with listed peers.

For investors, the key question is whether ICL Fincorp can grow outside its core regions while preserving credit controls and profitability.

Top AMC and Wealth Management Unlisted Shares Before IPO

AMC unlisted shares appeal to a different type of investor. Asset managers do not lend from their own balance sheet in the same way NBFCs do. Instead, they earn fees from managing investor money.

That can make the model asset-light and highly profitable at scale. But earnings still depend on markets, flows, scheme performance, distribution strength, and regulations around expense ratios.

1. PPFAS Unlisted Shares

Parag Parikh Financial Advisory Services, commonly associated with PPFAS Mutual Fund, is known for its value-investing philosophy and long-term investor communication. Its brand has earned strong recall among retail investors who prefer a disciplined and relatively transparent investment style.

PPFAS is not usually discussed as a scale story in the same way as the largest bank-backed AMCs. It is more often discussed as a trust, philosophy, and investor-loyalty story.

Why investors track PPFAS:

Strong investor trust and recognisable investment philosophy.

Loyal customer base built around long-term investing.

Potential to benefit from continued mutual fund participation.

Asset-light fee-income model.

Brand differentiation in a crowded AMC market.

Key risks to evaluate:

Revenue depends on AUM and market levels.

Scheme performance can influence inflows and redemptions.

Concentration around brand philosophy and key investment personnel.

Fee pressure across the mutual fund industry.

Limited private-market liquidity.

PPFAS may appeal to investors who value brand quality and process discipline, but valuation still matters.

2. SBI Funds Management Unlisted Shares

SBI Funds Management is one of India's most important asset management companies. It benefits from the SBI brand, a large distribution network, institutional trust, and participation across equity funds, debt funds, hybrid funds, exchange-traded funds, and passive products.

The SBI Funds Management IPO has strong public-market relevance. SEBI's public issue filing page showed the company's DRHP in March 2026. Public reports said the proposed IPO is an offer for sale by existing shareholders, with no fresh issue component.

Why investors track SBI Funds Management:

Market leadership in the Indian mutual fund industry.

Strong SBI distribution and brand trust.

Exposure to SIP growth and financialisation of household savings.

Scale benefits in asset management.

Clearer public IPO documentation than many unlisted names.

Key risks to evaluate:

Market correction can reduce AUM and fee income.

Passive products can pressure revenue yield.

High valuation expectations for a market-leading AMC.

IPO structure may be an offer for sale rather than fresh capital.

Competition from listed AMCs, fintech distributors, and passive managers.

SBI Funds Management is likely to remain a key AMC unlisted share to watch because it combines scale, brand, and public listing visibility.

3. ASK Investment Managers Unlisted Shares

ASK Investment Managers is known for portfolio management services, wealth management, and alternative investment solutions. Its customer base is more oriented toward high net worth individuals, family offices, and sophisticated investors than mass retail mutual fund investors.

ASK sits at the intersection of wealth management and private-market-style investing. That gives it exposure to the growth of affluent Indian households and professionally managed portfolios.

Why investors track ASK Investment Managers:

Strong brand in wealth and portfolio management.

Exposure to high net worth individual wealth creation.

Participation in PMS, alternative investments, and advisory-led solutions.

Asset-light revenue model when AUM scales.

Potential long-term growth from India's wealth management market.

Key risks to evaluate:

Market-linked revenue can fluctuate.

Performance track record affects investor flows.

Competition from banks, brokers, AMCs, and independent wealth platforms.

HNI behaviour can change quickly during weak markets.

Lower liquidity in unlisted shares.

ASK may suit investors who want exposure to India's wealth-management theme, but it should be compared with listed wealth and AMC peers before any decision.

How to Evaluate Financial Services Unlisted Shares

Before investing in financial services unlisted shares, use a structured checklist. A simple company story is not enough.

1. Check the Business Model

Start by asking how the company earns money. For NBFCs, study the loan segments, borrower profile, collateral, ticket size, pricing, and tenure. For AMCs and wealth firms, study AUM mix, fee yield, scheme performance, and client stickiness.

2. Review Asset Quality for NBFCs

For lenders, asset quality is central. Check gross NPA, net NPA, write-offs, collection efficiency, provision coverage, and credit-cost trends. If these numbers are not available, that itself is a risk.

3. Compare Valuation With Listed Peers

Private-market prices can move without the transparency of a stock exchange. Compare NBFCs with listed lenders on price-to-book and return on equity. Compare AMCs with listed asset managers on market capitalisation to AUM, price-to-earnings, margins, and growth.

4. Understand IPO Visibility

Not every unlisted company is close to IPO. Look for real milestones such as DRHP filing, SEBI observations, updated offer documents, board approvals, banker appointments, and official company statements.

5. Check Liquidity and Transfer Terms

Unlisted shares may not be easy to sell when you want liquidity. Confirm lot size, settlement process, demat transfer timelines, lock-in risks after IPO, taxes, and platform fees before investing.

If you are new to the process, review common investor questions on the Precize FAQs or contact Precize Care for platform-specific help.

Risks of Investing in Financial Services Unlisted Shares

Unlisted shares can be rewarding, but the risks are real. Financial services companies carry additional regulatory and market sensitivity because they deal directly with credit, money management, investor assets, and customer trust.

Key risks include:

Low liquidity: You may not find a buyer quickly or at your expected price.

Valuation uncertainty: Private-market pricing can differ from eventual IPO pricing.

Limited disclosures: Some companies provide less information than listed peers.

Regulatory risk: RBI and SEBI rules can affect NBFCs, AMCs, and wealth firms.

Credit risk: NBFCs can suffer when borrowers delay or default.

Market risk: AMCs and wealth firms can see revenue pressure during market declines.

IPO delay risk: A company may postpone or withdraw its IPO plan.

Concentration risk: Over-investing in one sector or one unlisted company can hurt portfolio balance.

A practical rule: if you cannot explain why the company should compound, what can go wrong, and how you might exit, you are not ready to invest.

Final Thoughts

Financial services unlisted shares sit in one of India's strongest long-term themes: the expansion of credit, investing, savings, and wealth management. NBFC unlisted shares offer exposure to lending growth, while AMC unlisted shares offer exposure to asset-light fee income and rising financial participation.

Hero FinCorp, InCred Holdings, Arohan Financial Services, PPFAS, SBI Funds Management, and ASK Investment Managers are all worth understanding if you track private financial companies before IPO. But none should be evaluated on name recognition alone.

Focus on fundamentals first: asset quality, profitability, capital strength, AUM growth, governance, valuation, and liquidity. IPO potential is useful, but it should be the final layer of analysis, not the starting point.

You can use the Precize Screener to compare available opportunities, research documents, pricing, and sector themes before taking the next step. Stay updated with unlisted companies through our Precize Community. If this article was useful, you can share it with other investors through the Precize Referral Program.

Frequently Asked Questions

1. Which Are the Top Financial Services Unlisted Shares in India?

Some of the most discussed financial services unlisted shares in India include Hero FinCorp, Hinduja Leyland Finance, InCred Holdings, Arohan Financial Services, ICL Fincorp, PPFAS, SBI Funds Management, and ASK Investment Managers. This is not a ranked buy list. Each company needs separate due diligence.

2. What Are NBFC Unlisted Shares?

NBFC unlisted shares are shares of non-banking financial companies that are not listed on stock exchanges. These companies may operate in areas such as vehicle finance, consumer loans, MSME lending, gold loans, education loans, or microfinance.

3. Which Is Riskier: NBFC Unlisted Shares or AMC Unlisted Shares?

NBFC unlisted shares usually carry more direct credit and leverage risk, while AMC unlisted shares carry more market and flow risk. The riskier option depends on the specific company, valuation, disclosure quality, and your ability to hold through illiquidity.

4. Can Financial Services Unlisted Companies Launch IPOs?

Yes, some financial services unlisted companies may launch IPOs if they meet regulatory, business, and market-readiness requirements. Investors should rely on official documents such as DRHP filings, SEBI observations, and final offer documents rather than informal market rumours.

Disclaimer: This content is for informational purposes only and does not constitute investment advice. Investing in unlisted shares involves risks including illiquidity and potential loss of capital. Consult a qualified financial advisor before making investment decisions. Precize is not a stock exchange and is not regulated by SEBI.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved