InCred Holdings UDRHP With SEBI: What Investors Should Read Before the IPO

InCred Holdings UDRHP filing: Timeline and why it matters

On May 6, 2026, InCred Holdings parent of non-banking finance company (NBFC) InCred Financial Services filed an Updated Draft Red Herring Prospectus (UDRHP) with India’s markets regulator SEBI. Official offer documents and updates typically appear on the regulator’s site bookmark SEBI and cross-check the final red herring prospectus when it lands.

This is not the first filing. The company had filed an initial DRHP confidentially in November 2025 and already received in-principle approval from SEBI. The UDRHP updates the picture with nine-month financials through December 31, 2025.

For anyone following NBFC listings, InCred is worth a careful read: The growth story is strong, but the filing also raises questions any serious investor should weigh.

InCred IPO Structure: Fresh Issue vs Offer For Sale

The IPO has two parts:

Fresh issue: Equity shares worth up to ₹1,250 crore.

Offer for sale (OFS): Up to 9.90 crore equity shares sold by existing shareholders.

Media estimates put the total issue size around ₹3,000–4,000 crore, with a valuation talked about near ₹15,000 crore (always confirm against the final prospectus and price band).

Who sells in the OFS

KKR India Financial Investments leads with 4 crore shares. Others include MNI Ventures (1.98 crore shares), MEMG Family Office LLP, V'Ocean Investments, Moore Strategic Ventures, and more.

Important: The company does not receive OFS proceeds. That money goes to selling shareholders only.

How to read KKR’s sale

A large exit by a marquee private-equity investor can mean confidence in timing and valuation and it can also mean partial monetisation. After the issue, how much KKR still holds is one lens on continued alignment.

Pre-IPO placement

The company may place up to 20% of the fresh issue before the IPO. If it does, the fresh issue size shrinks accordingly. For retail participants, a bigger placement can mean less stock left for the public offer and can affect listing-day price discovery.

Use of fresh issue money

Net proceeds from the ₹1,250 crore fresh issue are intended to flow to InCred Finance (the wholly owned NBFC) to add Tier-I capital, support lending, and support capital adequacy a standard pattern for a growing lender and no diversion to promoters from this bucket.

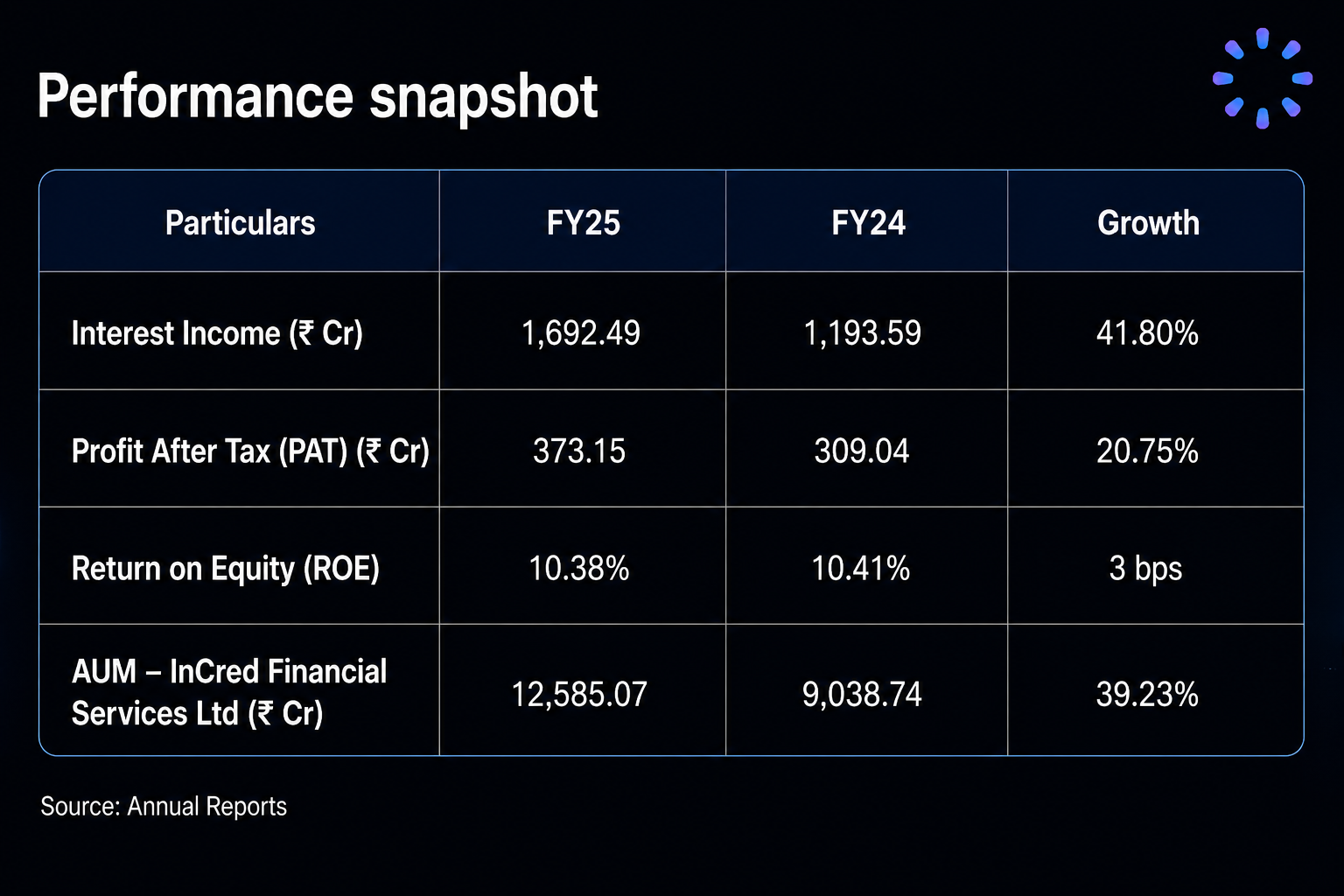

Performance snapshot

44% AUM CAGR and 85% PAT CAGR (FY23–FY25) stand out. Yield minus funding cost is roughly 8.3% points (18.39% − 10.05%) — a healthy spread for the model described. AA-/Stable from CRISIL and ICRA supports confidence on the funding and liability side.

The watch item is asset quality: Gross NPA moves from 2.05% to 2.28% year on year. With personal loans a large share of the book and yields high, small shifts in stress can hit profitability. 98.3% collection efficiency and a 327-person collections footprint are offsets — but post-listing, NPA and roll rates deserve tracking.

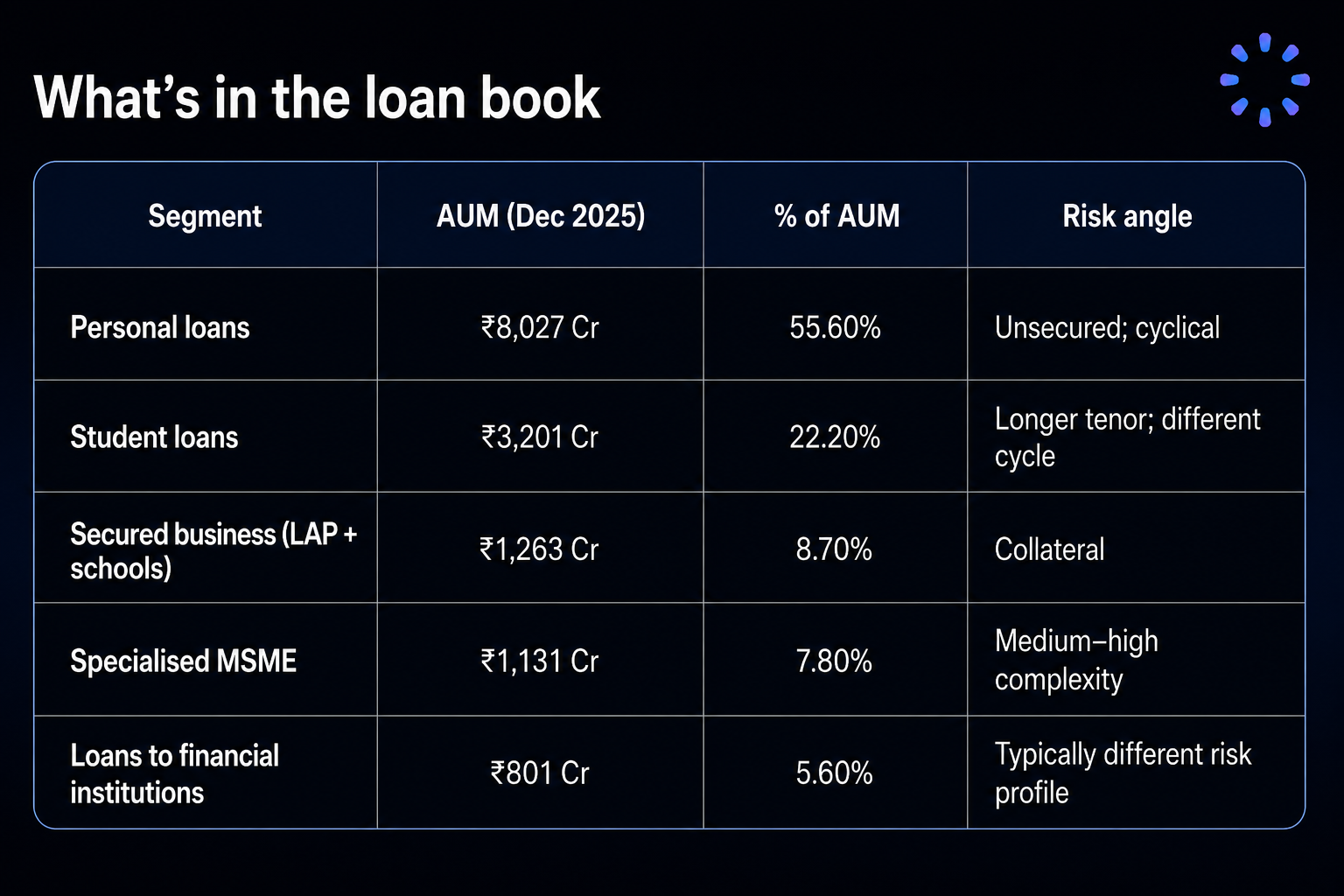

What’s in the loan book

The strategy targets underserved middle-market borrowers, salaried professionals, students, smaller businesses where large banks are often lighter.

Personal loans above half of AUM is a known sensitivity when rates are elevated and consumption stress appears in parts of the income pyramid.

Student loans (~22%) are a differentiator: Education credit can be stickier and longer tenor, which can help asset–liability thinking but segment-specific risks still apply.

Secured and MSME sleeves are still small but point to mix diversification over time.

Tech: Outcome vs. Slogan

InCred describes lending as risk-first, backed by an in-house tech stack and AI-enabled processes. The app is cited at 4.5 lakh+ users (Dec 2025); tech headcount rose from 114 to 152 (Mar 2023 → Dec 2025).

From outside the company, technology claims in a prospectus are hard to verify independently. One hard checkpoint in the document set is credit cost: 1.74% for FY25, second lowest among diversified NBFC peers in the comparison cited — that suggests underwriting is delivering measurable results, at least through that window.

Distribution: 158 branches, 152 cities, 19 states/UTs, 17,000+ PIN codes, 51 lender relationships — meaningful scale for a firm founded in 2017 by Bhupinder Singh.

One structural point many miss

The UDRHP states that InCred Capital and InCred Money are not subsidiaries of InCred Holdings. They sit in the wider group but outside this listed perimeter.

So this IPO is not a bet on wealth management or capital-markets subsidiaries bundled in; valuation and proceeds anchor on InCred Financial Services as the lending NBFC. Price the stock as that entity, not as “all of InCred Group.”

Bull vs. Bear

Reasons bulls cite

Very strong PAT growth vs peers in the CRISIL framing (FY23–25).

Healthy spread; AA-/Stable ratings.

CRAR ~25% vs 15% regulatory floor.

KKR association as institutional validation (with OFS nuance).

Collections and credit cost metrics that look disciplined on paper.

Fresh issue strengthens the operating lender.

Student finance as a structural theme in India.

Reasons to stay cautious

Personal loans ~56% of AUM — macro and collection sensitivity.

Gross NPA inching up in a tighter credit backdrop.

OFS, especially KKR’s block — partial exit, not necessarily “wrong,” but material.

Narrow IPO perimeter — no automatic exposure to Capital/Money.

Pre-IPO placement could shrink public float.

44% AUM CAGR may normalize as the base grows.

~₹15,000 crore implied valuation (~40× FY25 PAT) leaves little room if growth or asset quality disappoints.

Valuation sanity check

If ₹15,000 crore enterprise value is in the ballpark and FY25 PAT is ₹373 crore, that is roughly 40× trailing earnings. Annualising 9M FY26 PAT (₹290 crore × 4/3 ≈ ₹387 crore) lands near 38–39× on that run-rate — before final price band and share count adjustments.

Listed high-growth NBFCs in India often trade wide ranges (commonly cited 25–45× depending on growth and book quality). InCred’s growth supports a premium; unsecured concentration and NPA drift can cap how far that premium goes.

Once the issue price and book value per share are fixed, P/B will matter as much as P/E. Peer screens often include names such as Five Star Business Finance, SBFC Finance, and Arohan Financial Services — always compare mix, funding, and asset quality, not headline multiples alone.

When you study pre-IPO or unlisted opportunities in parallel, filter names by sector and growth profile with the Precize screener so comparisons stay like-for-like.

Verdict

InCred is a credible fast-growth NBFC story: scale, ratings, and profitability progression show up in the filing. The capital raise structure (fresh issue → subsidiary capital) is clean for a lender.

The stress tests are unsecured share, NPA trend, and valuation at the upper end of expectations. The OFS, particularly KKR, is a liquidity event for sellers — factor it into post-offer ownership, not just headlines.

Watch-list framing: High interest, valuation-sensitive. Subscription and holding decisions should lean on final price vs book, peer multiples, and updated asset-quality through FY26. Long-term holders comfortable with NBFC cycles may still find it interesting if the listing level leaves margin of safety.

Next step: When the price band and anchor book details land, compare them with peer NBFCs you track — and use Precize to stay across private-market opportunities if pre-IPO names matter to your portfolio.

Closing

The UDRHP is a milestone for a lender that in under a decade has built ~₹14,448 crore AUM, posted strong PAT growth, and carried investment-grade ratings rare air for a young NBFC.

As the process moves toward roadshows and listing, three practical monitors are: (1) issue price vs book and peers, (2) NPA and stress through FY26, (3) who owns how much after OFS and fresh issue.

For more market and unlisted education, see the Precize blog. If this article was useful, you can share it with other investors through the Precize referral program. To stay updated on unlisted companies, join our community.

Disclaimer: This piece is for information and education only. It is not investment advice and not a recommendation to buy, sell, or hold any security. Speak to a SEBI-registered adviser before acting. The author is not a registered investment adviser. Figures and quotes are from public UDRHP materials and press coverage as of May 8, 2026, unless noted; verify against the final prospectus and official regulatory disclosures.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved