Capital Gains Tax on Shares in India: LTCG & STCG Rates, Holding Periods, and Budget 2026

Union Budget 2026 did not increase or decrease these headline equity rates for FY 2026-27 (Assessment Year 2027-28): listed equity LTCG stays at 12.5% (with the same ₹1.25 lakh carve-out where eligible), and STCG on listed equity remains at 20% where Securities Transaction Tax (STT) conditions are met. Treat this article as a structured overview, not tax advice. For your own filing, confirm details with a chartered accountant and the latest Income Tax Department circulars.

What "capital gains" means

A capital gain is simply the profit when you sell a capital asset for more than its cost of acquisition (subject to adjustments the law allows). The Income-tax Act, 1961 splits gains into:

Short-Term Capital Gains (STCG) when you sell before completing the required holding period.

Long-Term Capital Gains (LTCG) when you hold long enough for the asset class.

What you pay depends on what you sold (listed equity, unlisted shares, debt, etc.), how long you held it, whether STT was paid on a recognized exchange trade, and which sections of the Act apply (for example, Section 112A is central for many listed equity gains).

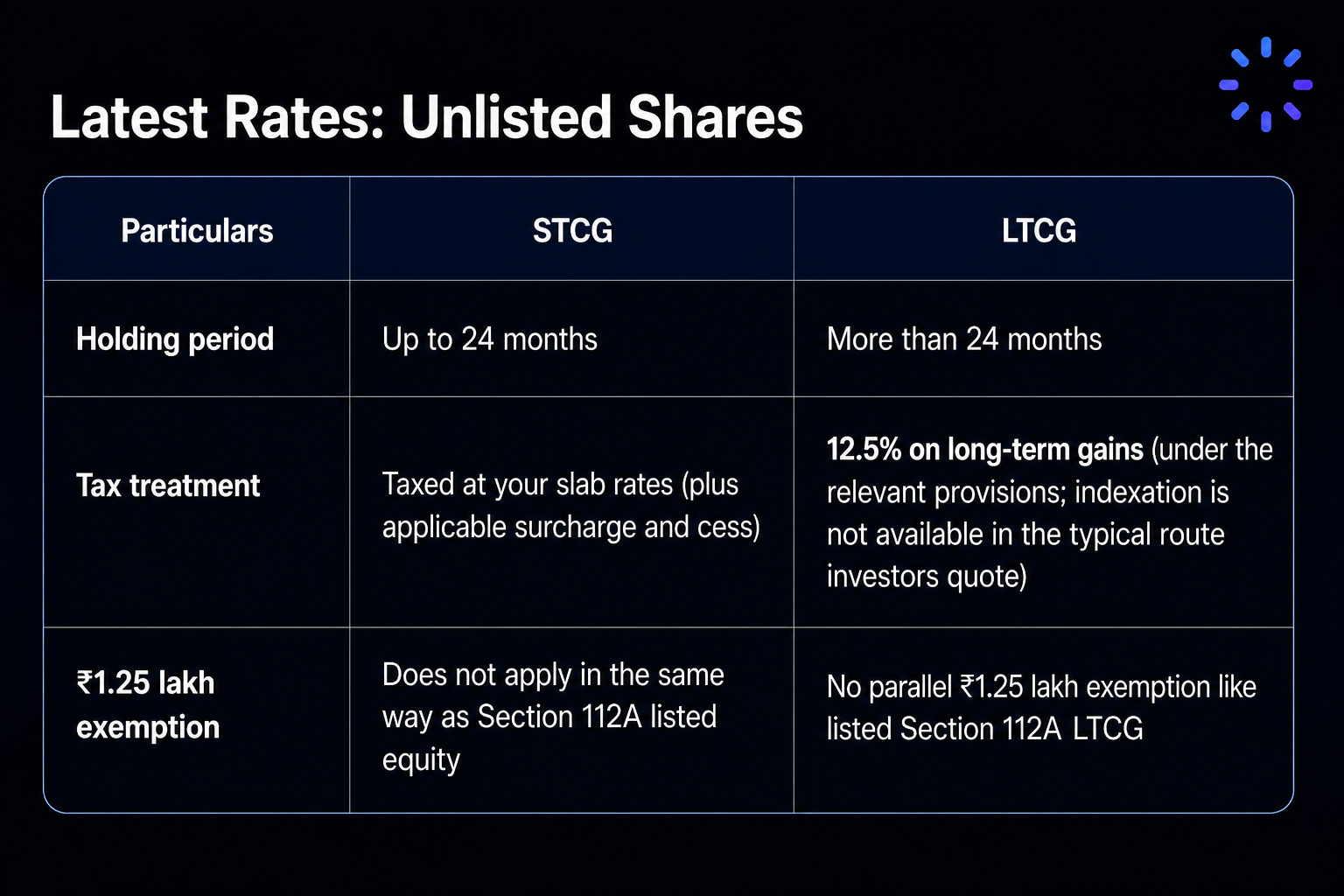

Latest Rates: Unlisted Shares (Including Pre-IPO)

Unlisted shares cover pre-IPO equity, startup stakes, private limited shares, and many ESOPs in unlisted companies. The holding-period bar for long-term treatment is different from listed stocks:

Because short-term unlisted gains follow slab rates, a taxpayer in the higher brackets can face a large tax bite on exits before 24 months. That is why exit timing matters so much for pre-IPO and private market holdings.

If you are evaluating unlisted opportunities and want to compare businesses systematically, the Precize screener helps you narrow the universe before you dig into filings and notes.

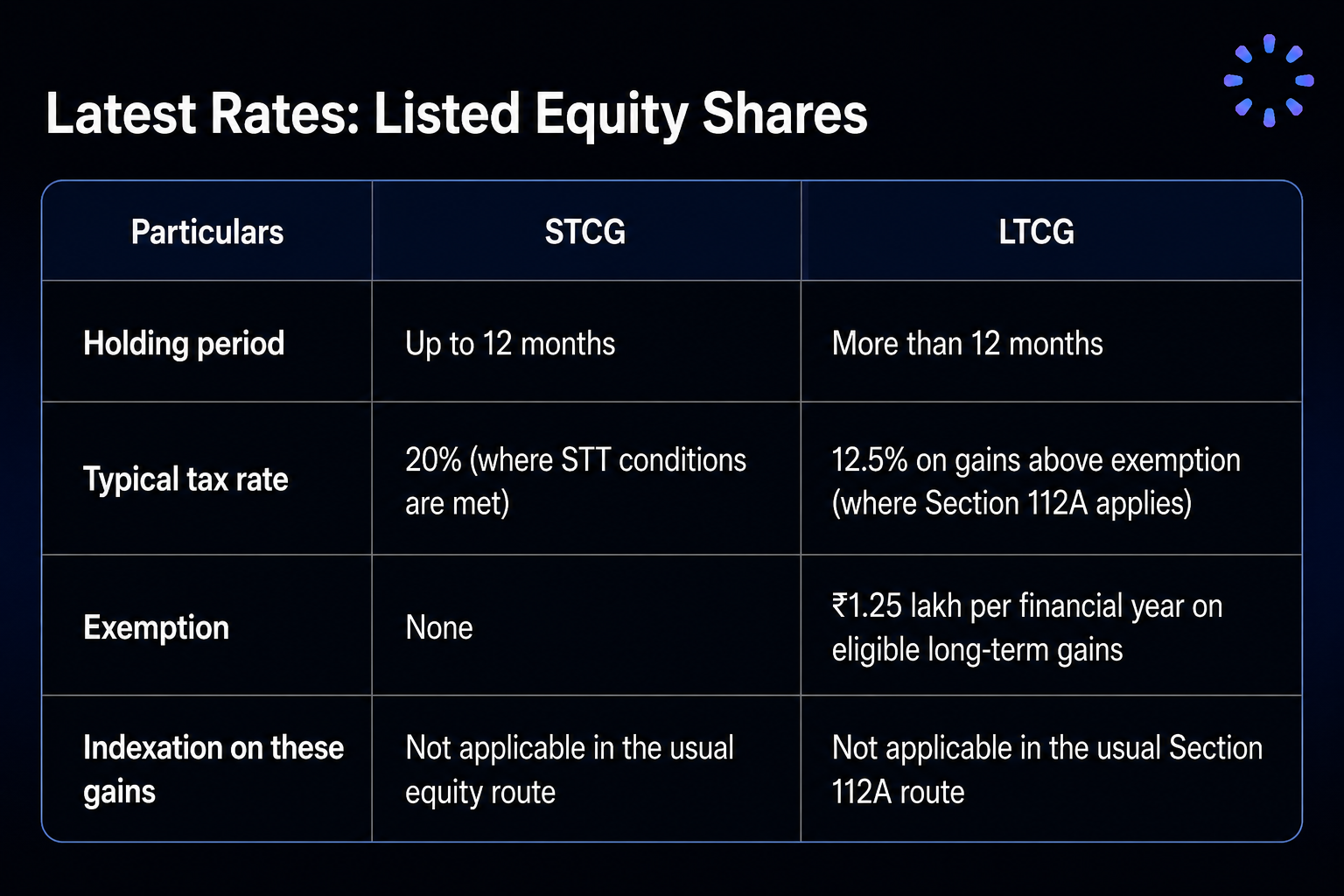

Latest Rates: Listed Equity Shares (FY 2026-27 context)

Listed shares are traded on recognized stock exchanges (for example, NSE and BSE). For investors, the usual labels look like this:

What changed in recent budgets (before Budget 2026): the Government had raised STCG on many listed equity trades from 15% to 20% and LTCG from 10% to 12.5%, while widening the annual LTCG exemption from ₹1 lakh to ₹1.25 lakh for qualifying listed equity. Budget 2026 largely left these equity rates as they were for FY 2026-27, so your planning focus stays on holding period, STT, and whether the gain sits in listed or unlisted books.

Authoritative numbers and fine print evolve with notifications. For statutory text and updates, use the Income Tax Department portal and Budget documents from the Ministry of Finance.

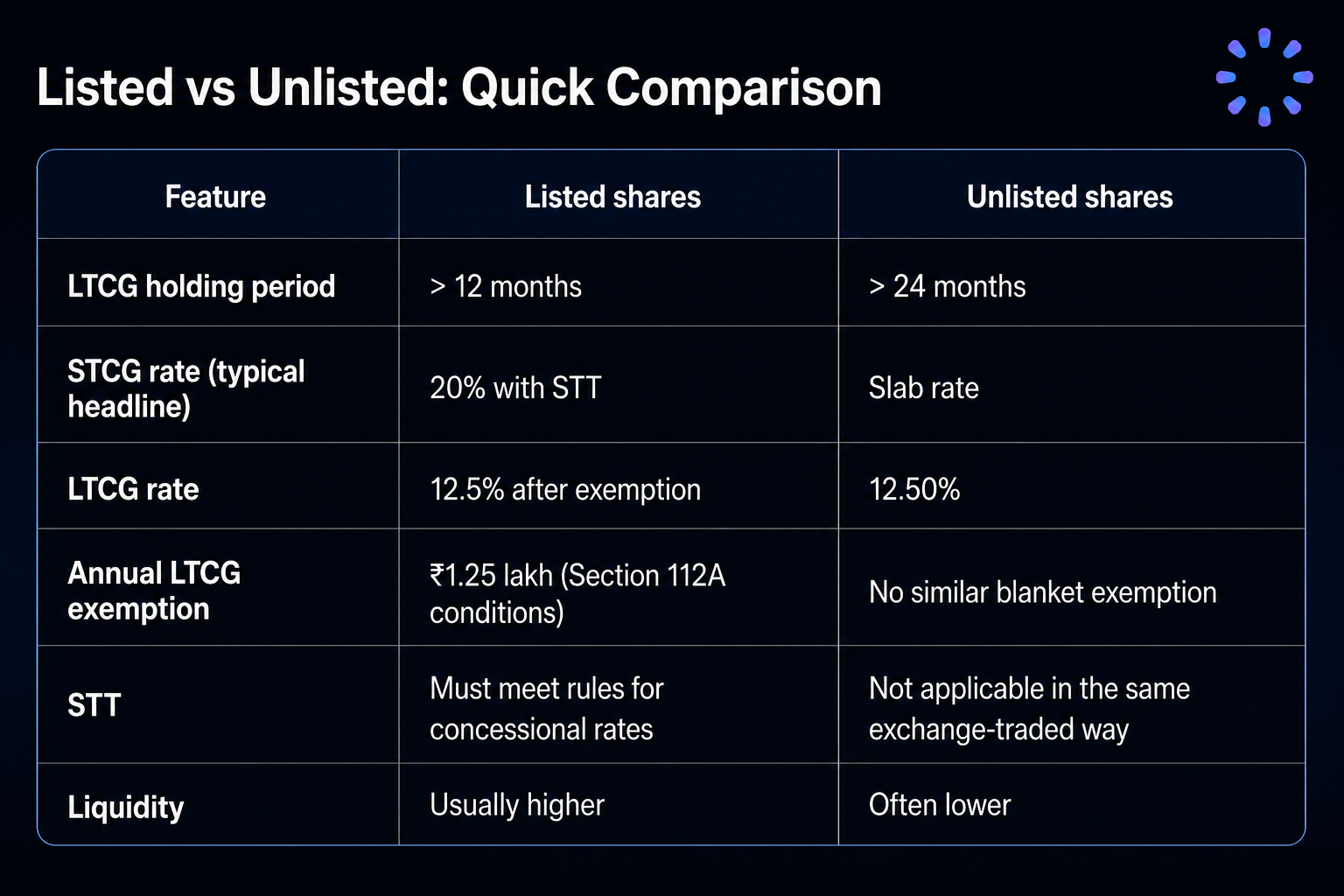

Holding periods

Listed shares

Sell at 12 months or less → generally STCG at 20% where STT rules are satisfied.

Sell after 12 months → generally LTCG at 12.5%, with the first ₹1.25 lakh of such gains in a year often exempt only when the listed-equity conditions (including STT) are met.

Example: You buy a listed stock in January 2026 and sell in September 2026. Holding is eight months, so the gain is usually STCG at 20% (subject to STT conditions). If you sell after February 2027, you cross 12 months, so the gain is typically tested as LTCG at 12.5% after the exempt threshold.

Unlisted shares

Sell within 24 months → STCG taxed at slab rates.

Sell after 24 months → LTCG taxed at 12.5% (subject to the applicable charging section and conditions).

Example: You buy pre-IPO shares in 2023 and sell in 2026 after holding more than 24 months. The profit is generally LTCG at 12.5%. If you exit at 18 months, the entire gain is typically STCG at your marginal slab.

Listed vs Unlisted: Quick Comparison

For more educational posts on private markets, see the Precize blog.

Why STT matters for listed equity

Concessional STCG and LTCG rates on listed equity generally require that Securities Transaction Tax (STT) has been paid as prescribed (buy/sell legs and transaction type matter). If you are looking at off-market transfers, physical, or other non-standard routes, do not assume the same rates apply. This is a common planning mistake.

Equity Mutual Funds

Equity-oriented mutual funds often follow similar holding-period ideas as listed equities (for example, STCG if held up to 12 months and LTCG if more than 12 months for many equity funds), but fund type (equity vs debt vs hybrid), stamp duty, and grandfathering can matter. Use this article only for the direct shares angle unless your adviser confirms parity for your scheme.

What Budget 2026 signals for investors

For FY 2026-27, media and industry summaries indicate no hike to the headline 12.5% / 20% listed-equity LTCG/STCG structure described above; the ₹1.25 lakh LTCG exemption on qualifying listed gains remains. Separately, Budget headlines sometimes cover buybacks, STT tweaks on certain segments, or reporting changes. Those items can affect specific transactions (for example, buybacks) even when headline equity rates are unchanged.

Because secondary summaries can miss nuances, pair this blog with primary sources: Income Tax Department, Ministry of Finance, and your tax adviser.

Who feels the impact most

Active traders: Higher STCG on short holding hurts net returns unless gross alpha is strong.

Long-term listed investors: Still benefit from LTCG rates and the ₹1.25 lakh exemption window where eligible.

Pre-IPO and startup investors: 24-month discipline is often the difference between 12.5% and slab taxation.

ESOP holders in unlisted firms: Vesting and liquidity events need a timeline, not just a valuation story.

Practical planning ideas (general education only)

Listed equity: If your strategy allows, crossing 12 months moves you from 20% STCG (when rules apply) toward 12.5% LTCG with a possible ₹1.25 lakh annual exemption on eligible gains.

Unlisted equity: Map exits against the 24-month marker when feasible; slab taxation below that mark can dominate the outcome.

Household-level exemption: The ₹1.25 lakh exemption is per taxpayer. Families sometimes allocate holdings across individuals for investment merit first, not tax alone; never let tax tail wag the risk wag.

Documentation: Keep contract notes, demat statements, cost adjustments, and corporate action notes. Private transactions need especially clean evidence of cost and dates.

If platform mechanics are unclear, start with Precize FAQs or reach Precize Care for product questions (not personal tax filing advice).

Worked examples (illustrative)

Example 1: Listed share

Purchase: ₹5 lakh

Sale after 14 months: ₹8 lakh

Gain: ₹3 lakh

Assume Section 112A applies and exemption is available:

Exempt: ₹1.25 lakh

Taxable LTCG: ₹1.75 lakh

Tax @ 12.5%: ₹21,875

Example 2: Unlisted share

Purchase: ₹10 lakh

Sale after 18 months: ₹15 lakh

Gain: ₹5 lakh

Holding is below 24 months, so the gain is typically STCG at slab rates. A taxpayer in the 30% slab might pay roughly ₹1.5 lakh plus cess before surcharge effects, versus 12.5% on long-term gains had they waited beyond 24 months (other risks permitting).

Important caveats investors overlook

STT and eligibility: Wrong assumptions here can change the entire rate card.

Surcharge and cess: Slab tables are not the full story for high incomes.

Loss set-off and carry-forward: Strategic use of capital losses has rules and deadlines.

International holdings and reporting: Not covered here; scope changes quickly.

Closing Takeaway

Capital gains tax in India now pairs higher STCG on short listed trades with 12.5% LTCG and a ₹1.25 lakh annual exemption on qualifying listed long-term gains. Unlisted paths demand 24 months for long-term 12.5% treatment; otherwise slab rates can apply to short-term gains.

Whether you trade listed stocks or build pre-IPO exposure, holding period and transaction mechanics are as important as picking the right company. Stay close to official guidance, and use professionals for filing.

Disclaimer: This article is for education and general information only. It is not tax, legal, or investment advice. Tax law depends on facts, residential status, regime choices, and notifications. Always consult a qualified chartered accountant or tax adviser before acting.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved