How Credit Ratings Shape Smarter Financial Decisions in 2025

Raising money is easy to discuss but difficult to execute well. The real challenge is earning the confidence of lenders and investors who need assurance that their capital will be repaid. That’s where credit ratings come in. They provide an independent view of reliability for individuals, companies, and governments.

In India, more than 80% of issuances are concentrated among AAA- and AA+-rated entities, and regulators have mandated minimum rating criteria for investments, particularly for retirement funds and insurance companies.

This highlights the significant role credit ratings play in determining access to capital and shaping investor behaviour.

This blog covers what a credit rating is, how it is built, how rating moves affect pricing and access to capital, common reading mistakes, and how to use ratings to make stronger decisions.

Key Takeaways

Credit ratings provide an independent view of a borrower’s reliability and are used by lenders, investors, and regulators to assess risk.

In India, over 80% of issuances are concentrated among AAA- and AA+-rated entities, with minimum rating criteria set by regulators for investments.

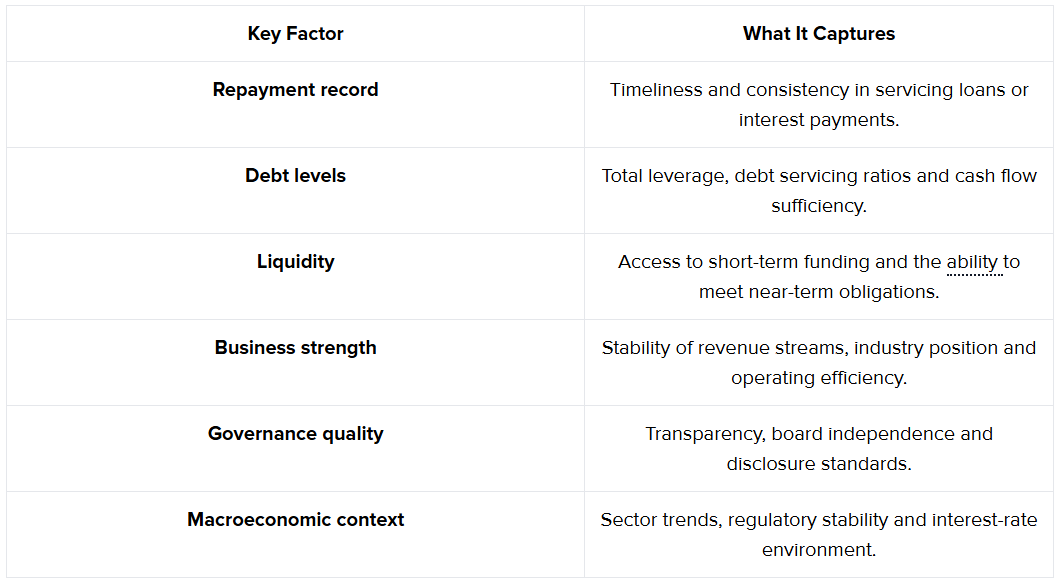

Credit ratings are based on factors such as repayment history, debt levels, liquidity, business strength, and governance.

Rating changes can directly impact the cost of capital, investor behaviour, and borrowing rates.

Credit ratings should be used alongside other data, and investors should track rating changes, diversify investments, and combine ratings with independent research for stronger decisions.

What Exactly Is a Credit Rating and How Is It Calculated?

A credit rating measures a borrower's likelihood of meeting repayment commitments. It serves as a shorthand for financial credibility among lenders, investors, and regulators.

In India, rating agencies such as CRISIL, ICRA, CARE Ratings, and India Ratings & Research assess both companies and debt instruments, while international agencies like Moody’s and S&P rate global issuers.

Credit ratings are expressed as grades ranging from AAA (highest safety) to D (default). Each grade reflects an independent view of creditworthiness, based on detailed financial analysis and judgment by analysts and committees.

To understand how ratings are determined, it helps to see what factors agencies examine most closely.

Rating agencies combine quantitative models with qualitative assessment. Algorithms estimate default probabilities, while analysts review management quality and sector resilience to arrive at a final grade.

Example:

Two Indian mid-sized companies may both report annual revenue of ₹500 crore. The first holds ₹150 crore in cash, keeps debt low, and discloses clear governance policies. The second carries ₹400 crore of debt, relies on seasonal income and has inconsistent disclosures.

Despite similar revenue, the first company might earn an A+ rating, while the second drops to BBB. The difference reflects discipline, not size, and directly affects their borrowing cost and investor interest.

Also Read: Key Ratios, Non-Financial Factors, Tools & How to Measure

Once you understand the basics of credit ratings, it’s important to explore how they actually influence the financial decisions of lenders, investors, and institutions.

How Credit Ratings Influence Investment, Lending, and Risk Decisions

Credit ratings sit at the center of financial decision-making. They act as a quick measure of reliability for lenders, investors, and regulators.

Banks use them to set credit limits, investors use them to measure risk, and companies depend on them to access affordable capital. A single downgrade can alter market confidence within hours.

A study by India Ratings & Research found that the annual default rate in India stood at 2.4% in FY 25, underscoring the continued reliability of ratings as a measure of repayment strength.

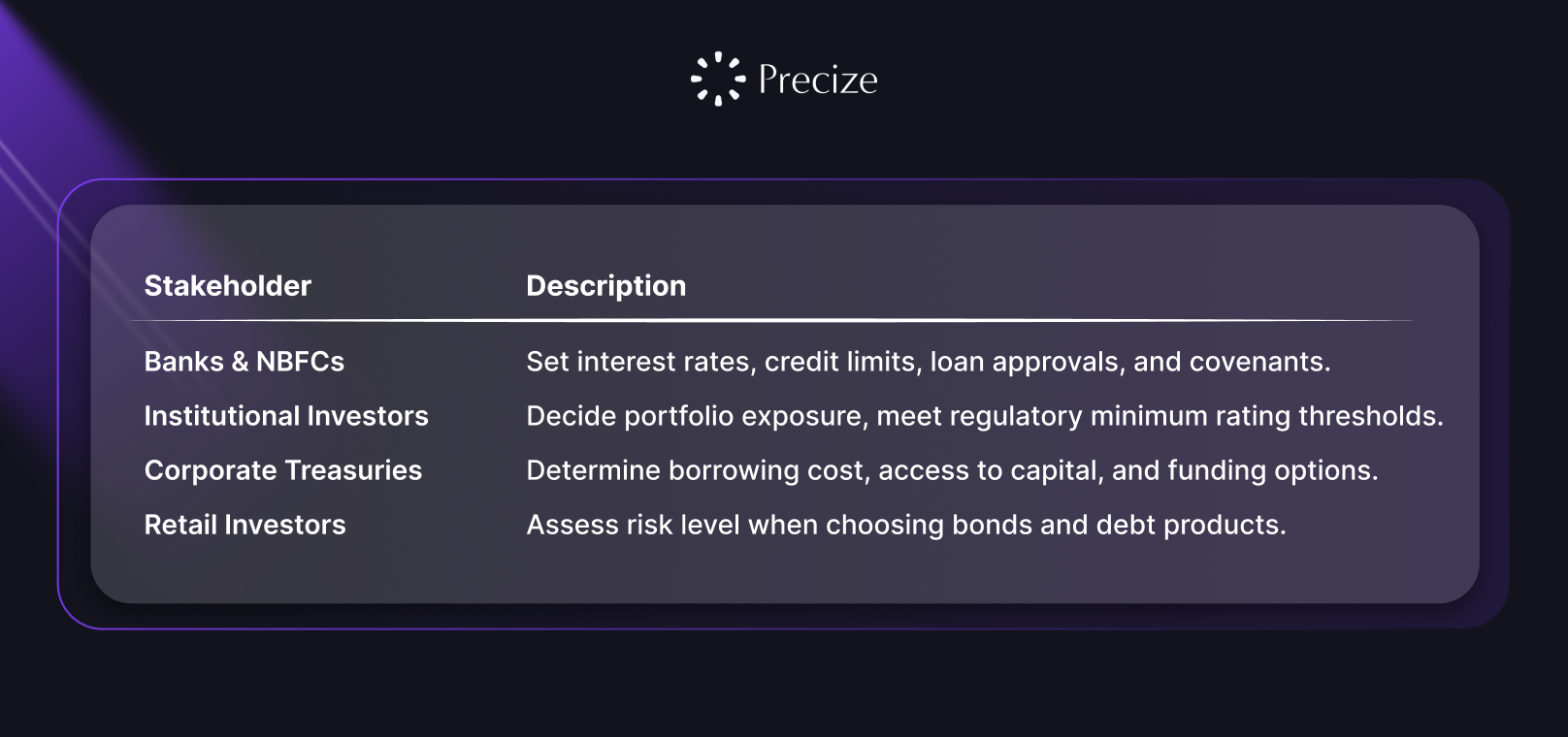

Below are the main ways ratings shape financial decisions and behaviour across the ecosystem.

1. Banks and NBFCs

Banks review borrower ratings before every major lending decision. A downgrade means higher interest rates, tighter covenants and sometimes reduced exposure. For new borrowers, the rating often determines whether credit is approved at all.

2. Institutional Investors

Pension funds, insurance firms and mutual funds use minimum rating thresholds in their mandates. A downgrade can trigger partial or complete exits, forcing portfolio rebalancing.

3. Corporate Treasuries

For companies, a higher rating means cheaper access to capital. A fall in rating pushes borrowing costs up and limits funding options. A one-notch drop can cost several percentage points in interest, cutting directly into profit margins.

4. Retail Investors

Credit ratings help individual investors judge safety. Before buying a bond or debt product, Indian investors often check whether the issue carries an AAA, AA or BBB rating. An AAA-rated bond may offer lower returns but greater stability, while a BBB-rated one carries a higher yield and higher risk.

Are your investment decisions grounded in reliable credit insights?

Precize provides verified research on private equity and private credit, including pre-IPO shares and trade finance opportunities. Explore Precize today and reserve access to upcoming private market opportunities.

Also Read: Credit Rating Meaning: Key Factors, Agencies, Types, and Credit Scores Difference

While credit ratings are crucial, there are common misconceptions that can lead to poor decision-making if not understood properly. Let’s look at some of the most frequent pitfalls.

Common Misconceptions and Pitfalls in Reading Credit Ratings

Credit ratings are not guarantees; they are opinions. They represent the probability of a borrower meeting their obligations, based on current and historical data. However, many investors treat these ratings as absolutes, which can lead to poor risk assessments.

1. Overreliance on Ratings

Relying only on a credit rating without understanding the underlying data is risky. Ratings are one signal of a company’s financial health, but do not capture everything.

Focusing solely on the rating without considering the company's financials, market conditions, or management can expose investors to hidden risks.

2. Recency Bias

Investors tend to put too much faith in recent rating upgrades. A company’s upgrade might seem like a green light to invest, but it could overlook long-term risks like high debt levels or weak cash flow. Don’t let short-term changes cloud your long-term judgment.

3. Herd Behaviour

Following the crowd can lead to poor decisions. If everyone rushes to buy bonds after an upgrade, it may be due to herd mentality rather than solid reasoning.

A stampede to invest based solely on a rating can push prices too high and increase risk.

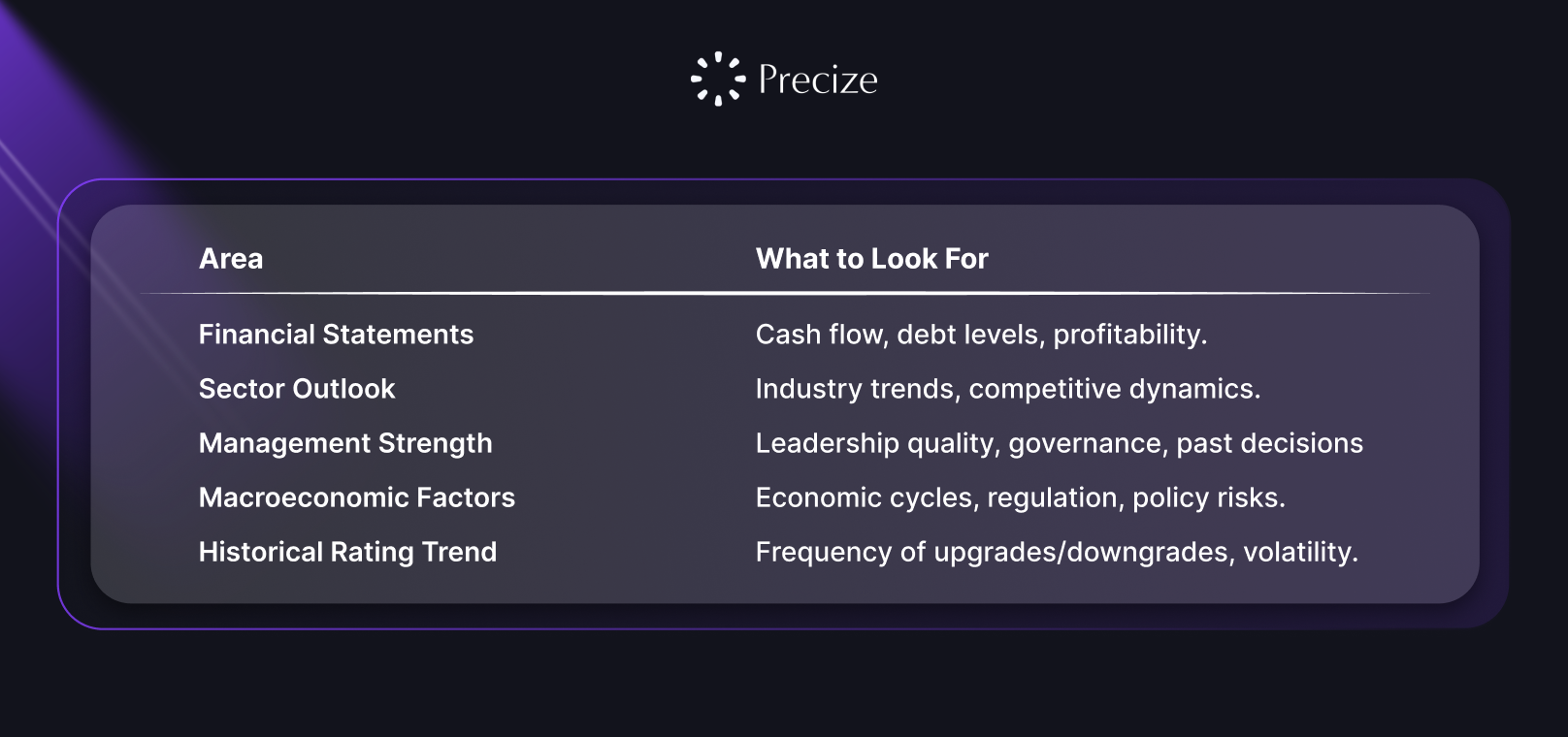

What to Review Beyond the Credit Rating

Financial Statements: Look at cash flow, debt levels, and profitability. A strong rating doesn’t always mean good liquidity or steady profits.

Sector Outlook: Ratings reflect current market conditions, but do not predict future changes in the industry. Understanding the sector’s trends is essential.

Management Strength: A high rating won’t protect you from poor leadership. Evaluate the company’s governance, leadership, and decision-making history.

Macroeconomic Factors: Consider external risks like economic downturns, regulatory changes, or political instability.

Historical Rating Trends: Look at how the rating has changed over time. Frequent upgrades or downgrades may indicate volatility.

Also Read: Road to $5 Trillion Economy: India's Growth & Strategy

Knowing how to interpret credit ratings is just the beginning. To make smarter financial decisions, it’s important to integrate ratings with a comprehensive investment strategy.

How to Use Credit Ratings to Strengthen Your Financial Decisions

Credit ratings are vital tools for assessing risk, but they should never be the only consideration in your investment decisions. To maximise the value of these ratings, it's essential to combine them with other data, understanding, and strategy.

Below are practical steps to ensure you use credit ratings effectively and make smarter, more informed decisions.

1. Combine Credit Ratings with Independent Research

Credit ratings are valuable, but they don't provide the full picture. Agencies like CRISIL and India Ratings & Research offer forward-looking opinions, not guarantees. Pair ratings with financial data, such as cash flow, profitability, and market trends, to get a clearer picture.

A BBB-rated company may still face liquidity issues despite its solid repayment history, and its reputation can impact borrowing costs significantly

2. Track Rating Changes Quarterly

Credit ratings are dynamic and can change frequently based on a company's financial performance or shifts in broader market conditions. Tracking these rating changes quarterly helps you stay ahead of potential risks and adjust your portfolio accordingly.

A downgrade can signal increasing risk, while an upgrade might indicate a more stable investment opportunity.

3. Diversify Across Rating Bands to Balance Risk and Return

High-rated bonds (such as AAA or AA) offer lower risk but also tend to yield lower returns. On the other hand, lower-rated bonds (BBB, BB) can offer higher returns but carry greater risk. To optimise your portfolio, balance investments across various rating bands.

Holding a mix of AA and BB bonds could provide stability while still capturing high-yield opportunities. This strategy helps mitigate the risk of concentrated losses if any one investment suffers a downgrade.

Conclusion

As we move further into 2025, credit ratings remain a critical input for evaluating financial risk, but they are most effective when used as part of a broader analytical framework. Ratings help establish baseline creditworthiness, yet smarter decisions come from combining them with deeper financial analysis, market context, and risk assessment.

Precize supports this approach by helping investors view credit ratings alongside structured risk insights and company fundamentals, allowing for more informed judgment rather than blind reliance on a single score.

In an environment defined by volatility and complexity, disciplined interpretation, not just access to ratings, is what ultimately drives better financial decisions.

Start making informed, strategic decisions today with Precize.

FAQs

Q: How often should I review credit ratings for the companies I invest in?

A: It's advisable to track credit ratings quarterly, especially for companies with variable performance or those in industries prone to market shifts. Rating changes can signal both risks and opportunities, so staying updated ensures timely adjustments to your portfolio.

Q: Can credit ratings change even if a company is financially stable?

A: Yes, ratings can change due to macroeconomic factors, market sentiment, or regulatory shifts. A company with solid financials may still face a downgrade if broader market conditions worsen or if there are changes in industry outlooks that affect risk perception.

Q: How do credit ratings impact individual investors in India?

A: For individual investors, credit ratings help assess the safety of bond investments. Bonds rated AAA or AA are considered low-risk, while those rated BBB or lower offer higher yields but come with increased risk, which is crucial when managing a personal portfolio.

Q: Are credit ratings influenced by a company’s management or governance?

A: Yes, credit rating agencies consider the strength of a company’s management and governance in their assessments. Poor governance or a history of inconsistent management decisions can lead to a lower rating, even if the company’s financials are solid.

Q: How do rating agencies determine whether a company’s rating should be upgraded or downgraded?

A: Rating agencies assess several factors, including debt levels, repayment history, market position, and external economic conditions. A company’s rating may be upgraded if it improves its financial stability, increases profitability, or lowers its debt-to-equity ratio, while downgrades typically follow financial distress or negative market developments

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved