Parag Parikh FY26 Results - Why Strong FY26 Performance Could Matter for Investors

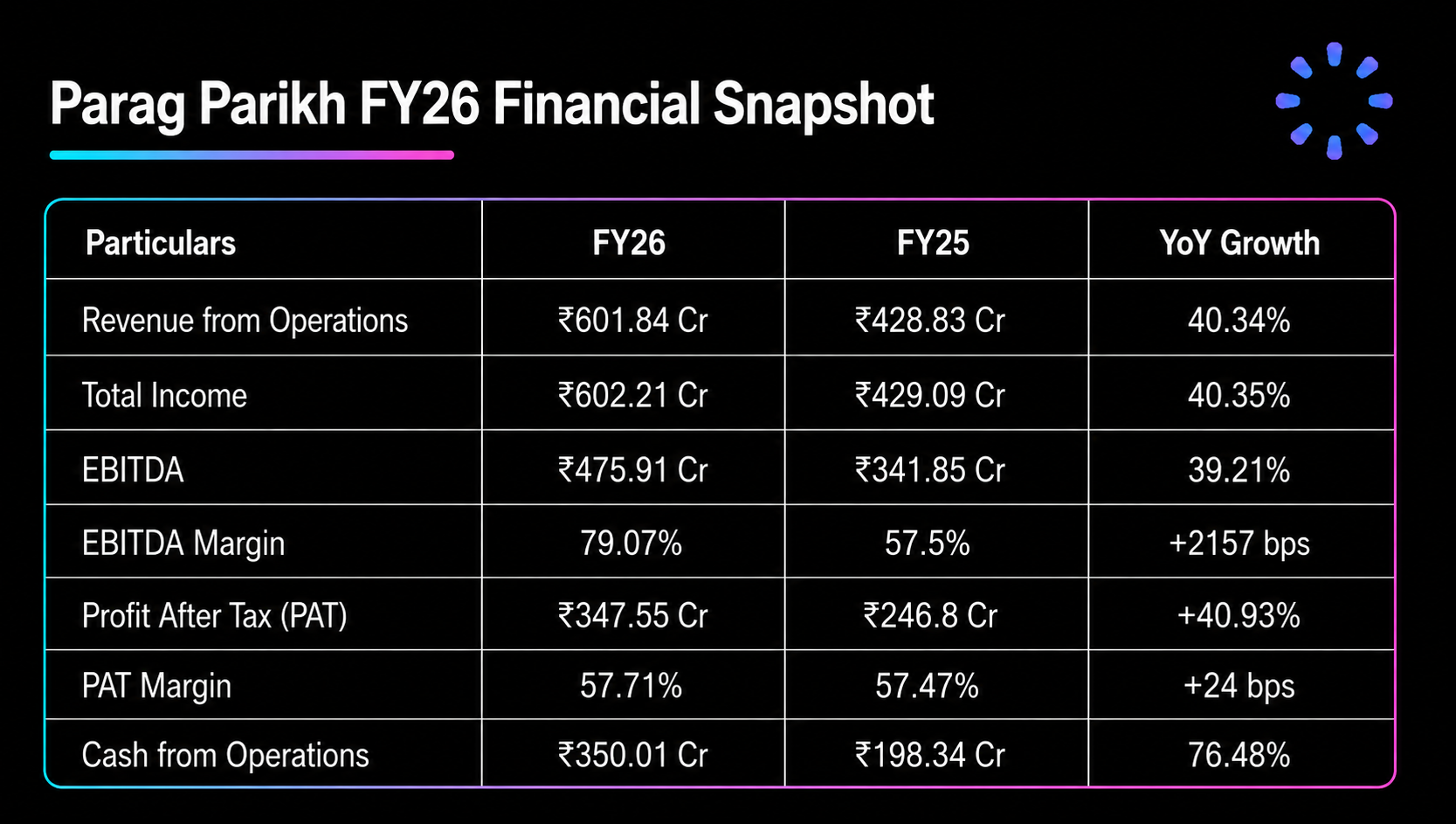

PPFAS reported revenue from operations of ₹601.84 crore, up 40.34% year-on-year, while profit after tax (PAT) increased 40.94% to ₹347.55 crore. Despite rapid growth, PPFAS continued to maintain industry-leading profitability, generated healthy operating cash flows, and strengthened its balance sheet, reinforcing the scalability of its asset management business.

If you hold or are tracking Parag Parikh unlisted shares, these results provide valuable insights into the company's earnings quality, operating efficiency, and long-term growth potential. Below is a detailed analysis of the FY26 performance and what it could mean for investors.

More company breakdowns like this live on the Precize blog. If you evaluate pre-IPO and unlisted names systematically, start with the Precize screener.

Parag Parikh FY26 Financial Highlights at a Glance

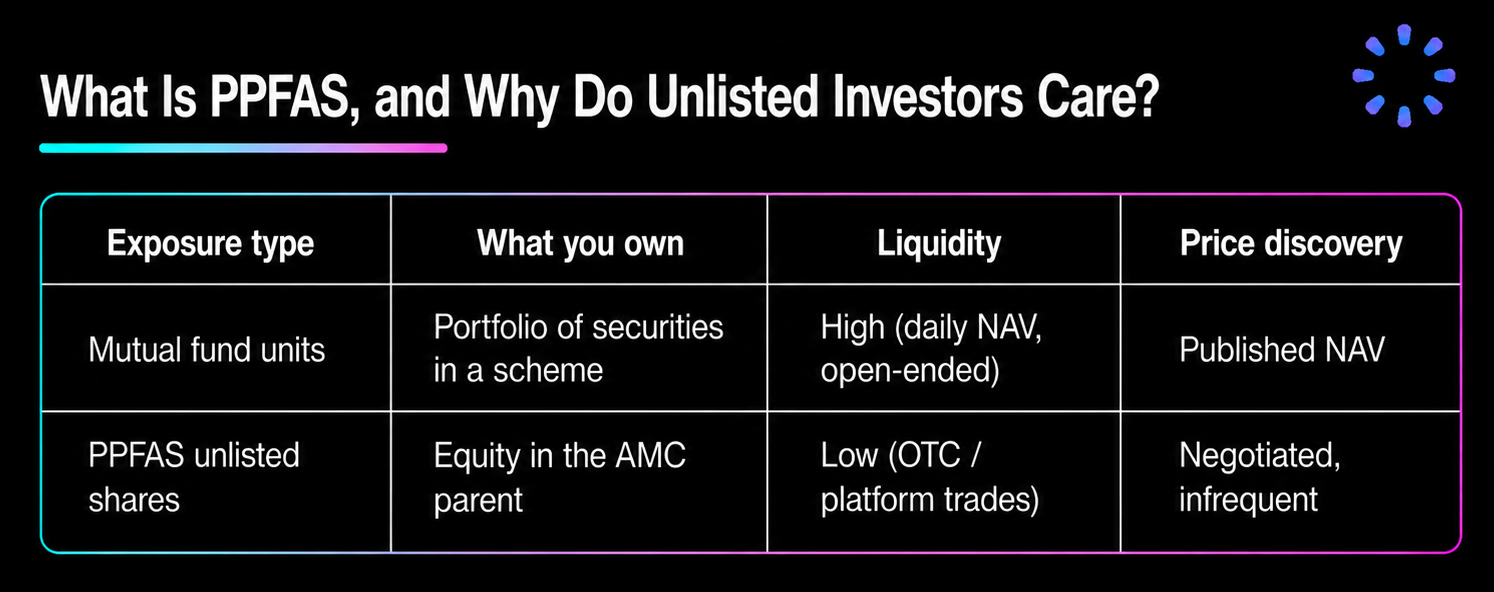

PPFAS is the unlisted parent company of Parag Parikh Mutual Fund. While investors participate in its mutual fund schemes through regular investment platforms, ownership in the company itself is available only through the unlisted market.

Two aspects stand out immediately. First, both revenue and profit grew by over 40%, highlighting the continued expansion of the company's core asset management business. Second, despite rapid growth, EBITDA margins remained close to 80%, reflecting the highly scalable nature of the AMC business model.

Revenue Crosses ₹600 Crore: What's Driving Growth?

Parag Parikh reported ₹601.84 crore in revenue from operations during FY26, compared with ₹428.83 crore in FY25.

For an asset management company, revenue primarily depends on average assets under management (AUM) and management fee income. During FY26, several favourable factors supported revenue growth:

Rising assets under management across equity-oriented mutual fund schemes.

Continued growth in SIP inflows as retail participation increased.

Higher management fee income resulting from expanding investor assets.

Strong brand recognition supported by the company's disciplined long-term investment philosophy.

India's mutual fund industry continues to benefit from increasing financial awareness, digital onboarding, and the shift of household savings towards financial assets. As one of the country's well-recognized active fund managers, PPFAS continues to benefit from these long-term structural trends.

Profit After Tax Grows Over 40%

PPFAS reported ₹347.55 crore in profit after tax, representing a 40.94% year-on-year increase over FY25.

The company's profitability remained strong as higher revenue translated into earnings without a proportionate increase in operating costs. This operating leverage is one of the biggest strengths of the asset management business model.

Unlike capital-intensive industries, asset management companies require relatively low capital expenditure. As assets under management increase, incremental revenue contributes significantly to profitability, allowing margins to remain consistently high.

Use the Precize screener to compare financial profiles across unlisted companies in adjacent sectors, from fintech to consumer brands, using the same margin-and-cash-flow lens.

Operating Margins Continue to Lead the Industry

PPFAS reported an EBITDA margin of 79.07% during FY26, compared with 79.67% in FY25.

Although margins moderated marginally, they remain among the highest in India's financial services industry. The company's ability to consistently generate EBITDA margins near 80% reflects disciplined cost management, efficient operations, and the scalability of its business model.

Its PAT margin also improved slightly to 57.71%, demonstrating that strong profitability continues even as the business expands.

Cash Flow, Balance Sheet, and the ₹25 Dividend

Healthy Operating Cash Flow

The company generated ₹350.01 crore in cash from operating activities during FY26, compared with ₹198.34 crore in FY25.

Strong operating cash flow indicates that reported earnings are backed by healthy cash generation rather than accounting adjustments. This provides financial flexibility to invest in technology, expand operations, and continue rewarding shareholders.

Balance Sheet Snapshot (March 31, 2026)

PPFAS continues to maintain a financially strong and low-leverage balance sheet.

Total Assets: ₹1,072.12 crore

Total Equity: ₹1,009.68 crore

Total Liabilities: ₹62.43 crore

Current Assets: ₹1,002.63 crore

A strong equity base and limited liabilities provide resilience during periods of market volatility while supporting future business expansion.

Dividend Announcement

The Board of Directors has recommended a final dividend of ₹25 per equity share (face value ₹10) for FY26, subject to shareholder approval.

The proposed dividend reflects management's confidence in the company's cash generation capabilities and its continued focus on creating long-term shareholder value.

Dividend yield on unlisted shares depends on your entry price, which is negotiated in the pre-IPO / unlisted market rather than displayed on an exchange ticker. That makes entry valuation as important as FY26 growth rates. Read our FAQs on unlisted shares for how pricing, settlement, and demat transfer typically work.

What Is PPFAS, and Why Do Unlisted Investors Care?

Parag Parikh Financial Advisory Services (PPFAS) is the holding company behind Parag Parikh Mutual Fund. Most retail investors interact with the fund house through schemes such as Parag Parikh Flexi Cap Fund. A smaller set of investors seek exposure to the company itself through unlisted equity.

That distinction matters:

Unlisted PPFAS shares appeal to investors who want direct ownership in the AMC business model rather than fund-level returns alone. The trade-off is familiar in private markets: potentially attractive long-term economics, but illiquidity, limited public disclosure cadence, and price opacity relative to listed peers.

FY26 results give unlisted investors fresh fundamentals to underwrite: Margins, Cash, and Capital return policy.

Industry Context: Why AMCs Are Winning the SIP Era

PPFAS did not grow in isolation. India's asset management industry has been supported by structural trends that extend beyond any single fund house:

Rising retail participation through systematic investment plans (SIPs).

Financial awareness spreading via digital onboarding and direct plans.

Shift from physical savings (real estate, gold) toward financial assets.

Long equity bull phases that expand AUM bases (with cyclical risk attached).

SEBI's mutual fund regulations govern expense ratios, disclosures, and distributor commissions. Regulatory stability has helped the industry scale, though rule changes can alter economics overnight. Active managers like PPFAS compete not only with other active houses but also with passive index funds pushing fee rates lower across the market.

How to Read Parag Parikh FY26 Results as an Unlisted Investor

Before you react to headline growth rates, run FY26 numbers through a simple four-point checklist:

Revenue vs AUM growth: Fee income should broadly track average AUM. If revenue outpaces industry AUM trends, the fund house may be gaining share or benefiting from mix shift toward higher-fee equity schemes.

Margin trajectory: Expanding EBITDA and net margins suggest operating leverage is intact. Flat or falling margins despite AUM growth can signal rising compliance, technology, or distribution costs.

Cash conversion: Compare PAT to operating cash flow. Large gaps can flag working-capital swings or one-off items worth investigating in full statements.

Capital return policy: Dividend size relative to earnings and cash reserves tells you how management balances shareholder payouts with reinvestment.

FY26 scores well on all four points: Revenue and PAT growth, Margin expansion, ₹350 crore operating cash flow, and a ₹25/share dividend recommendation. That does not eliminate market or regulatory risk, but it confirms the underlying AMC economics remain healthy.

Risks Unlisted Investors Should Weigh

Strong FY26 numbers do not eliminate structural risks. If you are evaluating Parag Parikh unlisted shares, balance the growth story against these headwinds:

Market dependency: AMC revenue ties to AUM, and equity-heavy AUM falls when markets correct. A prolonged bear phase can slow both inflows and fee income.

Competition: Passive funds, direct plans, and digital-first AMCs compete on cost and convenience. Market share is never guaranteed, even for respected brands.

Regulatory change: SEBI periodically revisits expense ratios, commission structures, and disclosure norms. A rule change that compresses fees would flow straight to margins.

Liquidity and valuation: Unlisted shares can be hard to exit quickly. Without daily market pricing, you need a clear view of fair value before you buy; FY26 profits are one input, not the whole model.

Concentration: Fund-house fortunes often rest on a handful of flagship schemes. Performance slippage in key strategies can affect flows disproportionately.

Precize publishes research to help investors weigh opportunities and risks together, not hype alone. If you want help evaluating a specific unlisted name, Precize Care can walk through process and documentation questions.

FY26 Parag Parikh Results: Outlook for Investors

India's AMC sector still sits in a long runway story: under-penetrated relative to developed markets, rising SIP books, and growing financial literacy. PPFAS enters that backdrop with strong brand equity, a disciplined investment identity, and FY26 financials that demonstrate scale.

Near-term earnings will still move with market cycles. Longer term, the Parag Parikh FY26 results show 35%+ revenue growth, expanding margins, ₹350 crore operating cash flow, and a ₹25 dividend recommendation, painting a company executing well within a favourable industry structure.

For investors already in mutual funds, FY26 results are a reminder that the fund house itself can be a separate investment thesis from the funds it manages. For those exploring that path, start with verified financials, understand illiquidity, and compare entry price against normalized earnings power.

Explore unlisted opportunities on Precize and use our research tools before you commit capital. Stay updated with unlisted companies through our Precize Community. If this article was useful, you can share it with other investors through the Precize Referral Program.

Frequently Asked Questions

1. What were Parag Parikh's FY26 revenue and profit?

Parag Parikh Financial Advisory Services reported ₹601.84 crore in revenue from operations and ₹347.55 crore in profit after tax for FY26. Revenue grew 40.34% and PAT grew 40.35% compared with FY25.

2. How much dividend did Parag Parikh announce for FY26?

The board recommended a final dividend of ₹25 per equity share (face value ₹10) for FY26. The payout is subject to approval at the annual general meeting.

3. Is Parag Parikh Financial Advisory Services a listed company?

No. PPFAS is unlisted. It is the parent company of Parag Parikh Mutual Fund. Investors can buy mutual fund schemes through standard channels; ownership in the company itself is available only through unlisted / pre-IPO equity markets.

4. What drove Parag Parikh's strong FY26 performance?

Higher assets under management, sustained mutual fund inflows (including SIPs), operating leverage in a low-capex AMC model, and disciplined cost management were the primary drivers. Industry-wide retail participation in mutual funds also provided a tailwind.

Disclaimer: This article is for informational purposes only and should not be considered investment advice. Investing in unlisted shares carries risks including illiquidity, limited disclosures, and potential loss of capital. Please consult a qualified financial advisor before making investment decisions. Precize is not a stock exchange and is not authorized by any capital markets regulator.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved