Types of Alternative Investments: Benefits and Risks

When you think of investing, stocks and bonds probably feel like the default choices. But if you are like many modern investors, you might be asking: is there something beyond the usual stock market rollercoaster? That curiosity has fueled a growing interest in alternative investments.

Investors look to these assets because they promise diversification when public markets are shaky, some strategies can provide income when rates rise, and certain real assets even act as a natural hedge against inflation. Alternatives are no longer just a playground for big institutions. More retail and high-net-worth investors are exploring them through private funds, semi-liquid products, and even tokenised assets.

The numbers highlight their rise. By mid-2023, alternative assets under management were valued at 13.4 trillion US dollars, with North America holding nearly 57 percent of this share. Yet fundraising slowed from 2024 onwards, showing how liquidity and exit challenges can make alternatives less predictable than they first appear.

This blog will help you understand the different types of alternative investments, how they generate returns, and most importantly, the benefits and risks you should know before adding them to your portfolio.

Key Takeaways

Alternative investments are assets outside traditional stocks and bonds, including private equity, venture capital, hedge funds, real estate, infrastructure, commodities, collectibles, digital assets, and structured products.

They appeal to investors seeking diversification, higher potential returns, income generation, and inflation protection.

Popular strategies include long-term plays like private equity, growth-focused venture capital, income-oriented private credit, flexible hedge funds, and tangible assets such as real estate and infrastructure.

Key benefits are diversification, return premium, inflation hedging, and steady cash flows, but these advantages come with trade-offs.

Risks include illiquidity, valuation opacity, high fees, leverage, regulatory uncertainty, and wide performance differences between managers.

What Are Alternative Investments?

Before diving into the details, it is worth defining what alternatives really are.

Alternative investments include any assets that are not traditional stocks, bonds, or cash. According to the CFA Institute, they are commonly grouped into private capital, hedge funds, and real assets.

You might be drawn to alternatives for three main reasons:

To diversify your portfolio away from traditional markets.

To seek potentially higher absolute or uncorrelated returns.

To protect against inflation or generate income.

Typically, alternatives are added as a satellite allocation in a portfolio, complementing the core holdings of equities and bonds.

Alternatives are broad and diverse, ranging from real estate to private equity.

Let’s break down the main types of alternative investments so you can see how each works in practice.

The Core Types of Alternative Investments

1. Private Equity (Buyouts and Growth)

Private equity firms acquire businesses with the goal of improving operations, increasing profitability, and selling them later at a higher valuation. Value is typically created through operational changes, cost efficiencies, and sometimes financial leverage.

According to McKinsey & Company, private equity remains one of the largest segments of alternatives, but fundraising slowed significantly in 2024 and 2025, highlighting its cyclical nature. Financial Times also reports investors have faced slower exits, making cash returns less predictable.

The private equity investment option is best for long-term investors who can handle illiquidity for 7 to 10 years.

While private equity focuses on mature businesses, venture capital is all about backing new ideas.

If you're looking to diversify your portfolio and are ready to explore the potential of private equity, Precize can help you start your journey today. Let us guide you through investing in high-growth private companies that can offer exciting returns.

2. Venture Capital

Venture capital is investing in early-stage companies. The reward is potentially massive returns if a startup succeeds, but the risk is equally high since many companies fail. Returns often follow a “power law,” where only a few investments drive most of the gains.

One challenge for early investors is the reduction in ownership stake when new funding rounds bring in additional investors. Liquidity is also limited, with exits such as IPOs or acquisitions typically taking 7 to 12 years.

Venture capital represents the risk-taking edge of alternatives. But if you prefer income-oriented strategies, private credit might be more appealing.

3. Private Credit

Private credit, also known as private debt, involves lending directly to companies outside of traditional banking systems. Strategies include direct lending, mezzanine financing, and special situations.

This market has grown rapidly. According to PwC, by September 2024 private debt unrealised value and dry powder reached 1.05 trillion US dollars, nearly doubling since 2019. The appeal lies in steady income, often from floating-rate loans, but liquidity is limited and downturns in the credit cycle can create losses.

Private credit is often seen as the income-generating heart of alternatives. For investors who want flexible strategies, hedge funds offer a very different approach.

Tap into stable, income-focused investments with Precize private credit.

4. Hedge Funds

Hedge funds use diverse strategies such as long/short equity, global macro, and event-driven investing. They aim to deliver returns that are not tightly correlated to the stock market.

By Q3 2024, hedge fund assets under management reached 4.9 trillion US dollars, with average returns around 10 percent that year. However, the SEC has cautioned that hedge funds with illiquid holdings can sometimes report artificially smooth returns. Fees are also high, often “two and twenty,” though investor.gov notes that mutual fund variants may provide lower-cost access.

Hedge funds bring flexibility but also complexity. Real estate, on the other hand, is more familiar to most investors.

5. Real Estate (Private & Listed)

Real estate can provide rental income and potential appreciation. Strategies include direct property ownership, private funds, or listed REITs. Risks include vacancies, refinancing pressures, and sensitivity to interest rates.

During market stress, some open-ended property funds have restricted redemptions, a reminder that real estate is not always as liquid as investors expect.

Real estate anchors portfolios with tangible assets. Infrastructure, another real asset, offers even more predictable cash flows.

6. Infrastructure and Renewable Energy

Infrastructure assets such as toll roads, airports, and renewable energy projects generate regulated or contracted cash flows. Many are linked to inflation, which makes them attractive during rising price environments.

The key risk is policy or regulatory change, especially for renewable energy projects.

Infrastructure provides stability, while commodities bring exposure to global supply and demand cycles.

7. Commodities and Natural Resources

Commodities such as oil, gold, and agricultural products can act as inflation hedges. Investors often use futures contracts, but these come with roll yield risks and volatility. Geopolitical events also play a major role in commodity price swings.

Commodities can hedge inflation but are volatile. If you want something more personal, collectibles may appeal.

8. Collectibles (Art, Wine, Cars)

Collectibles are passion-driven investments. Some rare items appreciate dramatically, but they are illiquid, costly to insure, and subjective in valuation.

Collectibles highlight the emotional side of investing. Digital assets, in contrast, are driven by technology and regulation.

9. Digital Assets and Tokenised Real-World Assets

Digital assets include cryptocurrencies and tokenised versions of traditional assets. Tokenisation aims to make investing more efficient by allowing fractional ownership and faster settlement.

However, regulation is tightening. The FCA classifies crypto promotions in the UK as “Restricted Mass Market Investments,” requiring risk warnings, appropriateness tests, and cooling-off periods. Reports from the Bank for International Settlements and Financial Stability Board warn that tokenisation creates both opportunities and new risks.

Digital assets are innovative but uncertain. For investors wanting structured exposure, semi-liquid funds are another option.

10. Structured Products and Semi-Liquid Funds

Structured products combine derivatives with traditional securities to offer tailored payoffs. Semi-liquid funds like interval or tender-offer funds allow periodic liquidity but come with layered fees. They are often designed for mass-affluent investors who want access to alternatives without full lock-ups.

Now that we have seen the wide landscape of alternatives, let us look at why investors actually consider them and what risks they need to prepare for.

Also Read: Understanding Basics Of Financial Business: Types And Importance

Benefits: Why Consider the Types of Alternative Investments?

Alternative investments offer several compelling benefits:

Diversification: Alternatives can reduce dependence on traditional equity and bond returns. For example, infrastructure and commodities may behave differently during inflationary periods, offering a cushion against downturns.

Potential return premium: You may earn higher returns for taking on illiquidity, complexity, or sourcing advantages. Private equity historically has delivered higher average returns than public equities, though results vary by manager.

Inflation protection: Real assets like real estate, commodities, and infrastructure often provide natural inflation hedges. Contracts linked to consumer price indices or commodity prices adjust with inflation, preserving value.

Income generation: Private credit, real estate debt, and infrastructure projects generate steady cash flows, making them attractive for income-focused investors.

These benefits are attractive, but they are never free. Each advantage comes with risks, which are equally important to understand before committing capital.

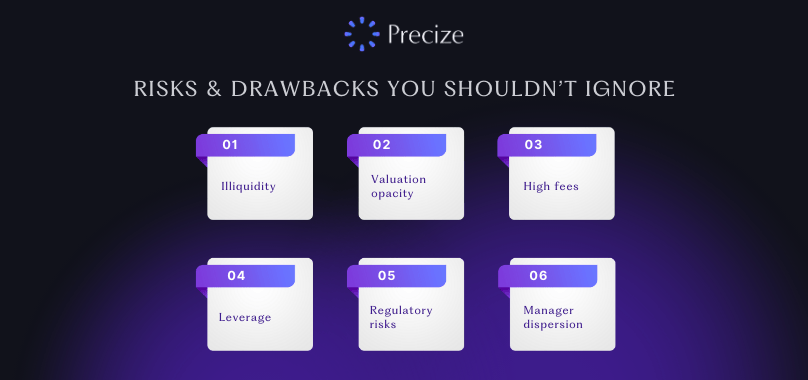

Risks & Drawbacks You Shouldn’t Ignore

While alternatives offer opportunities, they carry significant challenges:

Illiquidity: Most private funds require investors to lock money for years. Redemption gates and side pockets may restrict access during stress.

Valuation opacity: Illiquid assets are often valued infrequently. This can smooth out reported returns, masking the true volatility of the portfolio.

High fees: Many hedge funds charge management and performance fees. According to Investor.gov, “two and twenty” remains common, making costs a serious drag on net returns.

Leverage: Some strategies rely heavily on debt or derivatives. While this can amplify returns, it also magnifies losses, especially during market shocks.

Regulatory risks: Alternatives like crypto are subject to rapidly changing rules. The FCA’s restrictions on crypto marketing in the UK are an example of how fast compliance burdens can shift.

Manager dispersion: Unlike public equity indices, performance in alternatives can vary widely between managers. Choosing the wrong manager can mean underperformance even when the asset class performs well.

With benefits and risks laid out, the final step is deciding whether alternatives belong in your portfolio and how much weight they should carry.

Final Thoughts

Alternative investments can diversify your portfolio, provide income, and offer protection against inflation. At the same time, they require patience, careful due diligence, and an understanding of risks like liquidity limits, valuation opacity, and high fees. By exploring the different types of alternative investments, you can decide which strategies fit your goals and risk tolerance.

At Precize, we make alternative investments accessible, from unlisted pre-IPO shares to private credit opportunities. Our platform is built to help you diversify, generate income, and invest with confidence.

Ready to explore unlisted shares or private credit deals? Start investing with Precize today.

Frequently Asked Questions (FAQs)

What percentage of a portfolio should be in the types of alternative investments?

Advisers usually suggest 10 to 25 percent of a portfolio. The exact amount depends on how much risk you are comfortable with and how easily you may need access to your money.

Are semi-liquid funds safer than traditional hedge funds?

Semi-liquid funds let you take out money more often than hedge funds, but they still carry risks like market swings, valuation issues, and limits on withdrawals.

How do gates and lock-ups actually work?

A lock-up means you cannot take out your money for a set time. A gate means only part of your money can be withdrawn during certain periods. These rules protect the fund but can limit your flexibility.

What is tokenisation and does it reduce risk?

Tokenisation breaks assets, like real estate, into digital tokens so they can be traded more easily. It can improve access and efficiency, but the risks of the asset remain, and new technology and regulatory risks are added.

Can I access alternatives without being accredited?

Yes, through products like interval funds, ETFs, or UCITS funds. These allow regular investors to get exposure, though usually with lower return potential and different fees compared to private funds.

Disclaimer

The content in this blog is for informational purposes only and does not constitute financial advice. Alternative investments come with inherent risks, and investors are advised to consult a financial expert before making any decisions.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved