TL;DR

Capital gains are profits from selling assets like property, shares, mutual funds, or gold and are taxable under Indian law.

They are classified as short-term or long-term based on how long you hold the asset before selling.

The tax rate depends on the type of gain and asset, with recent updates including a 12.5% flat LTCG rate (without indexation) for most cases.

You can calculate capital gains using a simple formula: Sale Price – Purchase Cost – Transfer + Improvement Expenses.

Smart tax planning strategies, like claiming exemptions, setting off losses, and timing your sale, can help reduce your tax burden.

If you’ve ever sold a piece of land, a flat, or even made a profit from shares or mutual funds, you’ve probably wondered how much tax you need to pay on that amount. That profit is called a capital gain, and it’s something you can’t ignore while filing your income tax.

In this blog, you’ll understand what capital gains really mean for you, the difference between short-term and long-term capital gains, and the current tax rates. You’ll also learn how to calculate capital gains tax correctly and explore some smart tax planning strategies to manage your gains better and avoid last-minute confusion.

Let’s get started!

What Are Capital Gains?

Capital gains are the profits you earn when you sell a capital asset like property, shares, mutual funds, or gold at a higher price than what you paid for it. The difference between the selling price and the purchase price is treated as your capital gain and is taxable under the Income Tax Act in India.

The amount of tax you pay depends on how long you hold the asset before selling it. Based on the holding period, capital gains are classified as either short-term or long-term, with different tax rates and rules for each.

Knowing what capital gains are sets the foundation. Now, let’s explore the different types.

Types of Capital Gains

In India, capital gains are divided into two main types, short-term and long-term, based on how long you hold the asset before selling it. Each type has different tax rules and holding periods depending on the kind of asset.

Short-Term Capital Gains (STCG)

You make a short-term capital gain when you sell an asset within a short period after buying it.

Holding period:

For listed equity shares and equity mutual funds: Less than 12 months.

For real estate, unlisted shares, bonds, and other assets: Less than 24 months.

Tax rate (FY 2025):

For listed equity shares and equity mutual funds (where STT is paid): 20% (earlier, it was 15%).

For other assets: Taxed as per your income tax slab.

Long-Term Capital Gains (LTCG)

A long-term capital gain is when you sell an asset after holding it for a longer period.

Holding period:

For listed equity shares and equity mutual funds: More than 12 months.

For real estate, unlisted shares, bonds, and other assets: More than 24 months.

Tax rate (FY 2025):

For listed equity shares, equity mutual funds, and business trust units: 12.5% on gains above ₹1.25 lakh per year (no indexation benefit).

For real estate, unlisted shares, bonds, and other non-financial assets: 12.5% without indexation.

If you bought the property before July 23, 2024, you have the option to choose between 12.5% (without indexation) or 20% (with indexation benefit).

Key Takeaways

Classification matters: The tax you pay depends on how long you held the asset before selling.

Equity vs. Other Assets: Listed equities have shorter holding periods compared to real estate and unlisted assets.

Updated Rates (FY 2025):

STCG on listed equity increased to 20%.

LTCG on listed equity is taxed at 12.5% for gains over ₹1.25 lakh, with no indexation.

Choice for older properties: Properties bought before July 23, 2024, allow you to choose the more tax-beneficial route (with or without indexation).

Tax slab impact: For short-term gains on non-equity assets, your personal income tax slab still applies.

Once you're clear about the types of capital gains, it's important to see how the actual gain is calculated to know what part is taxable.

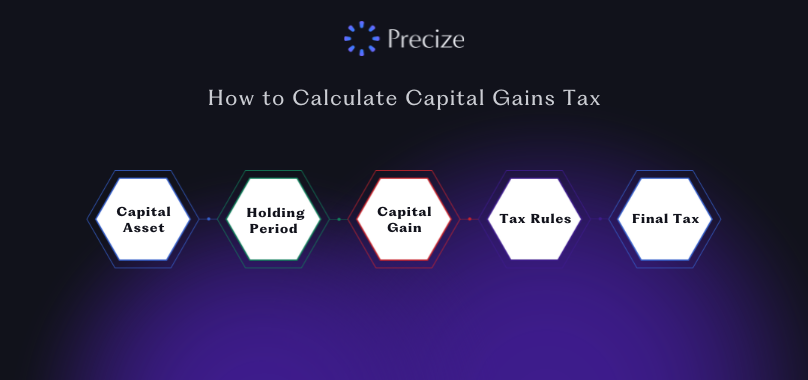

How to Calculate Capital Gains Tax

To figure out your capital gains for the financial year 2024–25 (assessment year 2025–26), you can follow the pointers below. Here is how you can do it:

1. Identify the Capital Asset

Start by checking if the asset you sold is considered a capital asset under Indian tax laws. Common capital assets include real estate, shares, mutual funds, gold, jewellery, and even virtual digital assets like cryptocurrency. Personal-use items like clothes, furniture, or business stock are not counted as capital assets.

2. Check the Holding Period

Based on how long you hold the asset, your gain will either be short-term or long-term.

3. Calculate the Capital Gain

Use this formula:

Capital Gain = Sale Price – Purchase Cost – Transfer Expenses – Improvement Cost

Sale Price: The amount you received from selling the asset.

Purchase Cost: The original price paid for the asset.

Transfer Expenses: Any costs related to the sale (brokerage, legal fees, etc.).

Improvement Cost: Expenses for improving the asset before sale (if any).

Note: As per the 2025 rules, indexation (adjusting cost for inflation) is not available for most assets. If you sold a property bought before July 23, 2024, you may still compare with the older method using indexation, but it's optional.

4. Apply the Tax Rules

Once you know the type of gain, apply the relevant tax rules to calculate the taxable amount.

5. Calculate Final Tax

Subtract any exemption (₹1.25 lakh in case of LTCG) from your total gain.

Multiply the remaining amount by the applicable tax rate.

Add surcharge and cess, if applicable.

Example (LTCG on Shares):

Sale Price: ₹5,00,000

Purchase Cost: ₹2,00,000

Transfer Expenses: ₹5,000

Capital Gain: ₹5,00,000 – ₹2,00,000 – ₹5,000 = ₹2,95,000

Exemption: ₹1,25,000

Taxable Gain: ₹1,70,000

Tax Payable: 12.5% of ₹1,70,000 = ₹21,250 (plus surcharge and cess).

Once you know how to calculate your capital gains tax, the next step is finding simple ways to manage and reduce that tax legally.

Smart Tax Planning Strategies for Capital Gains

Planning ahead can help you reduce the tax you may need to pay on your capital gains. While you can’t avoid tax completely, there are a few legal ways to manage and lower your tax burden. Here are some practical strategies you can consider:

1. Use Exemptions Available Under the Income Tax Act

If you have long-term capital gains from selling property, you may be eligible for exemptions under sections 54, 54EC, and 54F.

These sections allow you to claim tax relief if the sale proceeds are used in specific ways, such as purchasing another residential property or investing in notified bonds.

2. Set Off Capital Losses

You can adjust your capital gains with capital losses from other investments.

Short-term capital losses can be set off against both short-term and long-term gains.

Long-term capital losses can only be adjusted against long-term gains.

Unused losses can also be carried forward for up to eight years.

3. Plan the Sale Timing

If you’re close to the holding period needed for long-term gains, it might help to wait and qualify for the lower tax rate.

Holding the asset a little longer could shift your gain from short-term to long-term, which is usually taxed at a lower rate.

4. Split Gains Across Financial Years

If your total gain is expected to be high, selling assets in different financial years may help. This way, you can make use of the basic exemption limit (like ₹1.25 lakh for LTCG) more effectively and reduce overall tax in one year.

5. Keep Proper Records

Make sure you have clear documentation of your purchase cost, sale price, improvement expenses, and any transaction-related costs. These records are important not just for accurate calculation but also in case of a tax audit.

Conclusion

Now that you’ve understood what capital gains are, the different types, how they’re taxed, and how to calculate them, it becomes easier to manage your tax responsibilities. You’ve also seen how smart planning, like using exemptions, adjusting losses, or simply timing your sale, can help reduce your tax burden. With recent changes in tax rules, staying informed and organized is key to handling capital gains the right way.

If you're looking to explore alternative investment opportunities beyond the usual options, Precize gives you access to pre-IPO shares and global trade finance opportunities. These options can help add variety to your portfolio and offer exposure to private market investments.

Reserve your access with Precize and take a step towards building a more diversified and future-ready portfolio.

Frequently Asked Questions (FAQs)

1. What is indexation, and is it still allowed?

Indexation is the process of adjusting the purchase cost of an asset based on inflation, which helps reduce the taxable capital gain. However, under the latest rules, this benefit has been removed for most assets sold after July 23, 2024. In some cases, especially for property purchased before this date, the old indexation rules may still apply in a limited way.

2. Can you use the basic exemption limit on capital gains?

No, capital gains do not benefit from the basic income tax exemption or rebate under the new tax regime. They are taxed separately under specific rules.

3. Is capital gains tax applicable to inherited or gifted assets?

You don’t have to pay tax when you receive an asset through inheritance or as a gift. But if you sell that asset later, you’ll need to pay capital gains tax. The original purchase price and holding period of the previous owner will be considered while calculating your gain.

4. Which assets are excluded from capital gains tax?

Items for personal use, like clothes, furniture, or household goods, as well as stock-in-trade and raw materials used in business, are not treated as capital assets. So, they aren’t subject to capital gains tax.

Disclaimer

The information provided in this blog is for general understanding only and should not be considered as tax, legal, or financial advice. Tax laws are subject to change, and the actual tax treatment may vary based on individual circumstances. Please consult a qualified tax advisor or financial expert for guidance specific to your situation.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved