MSEI FY26 Results Show ₹1,434 Cr Assets but a ₹25.84 Cr Loss - What Investors Should Know

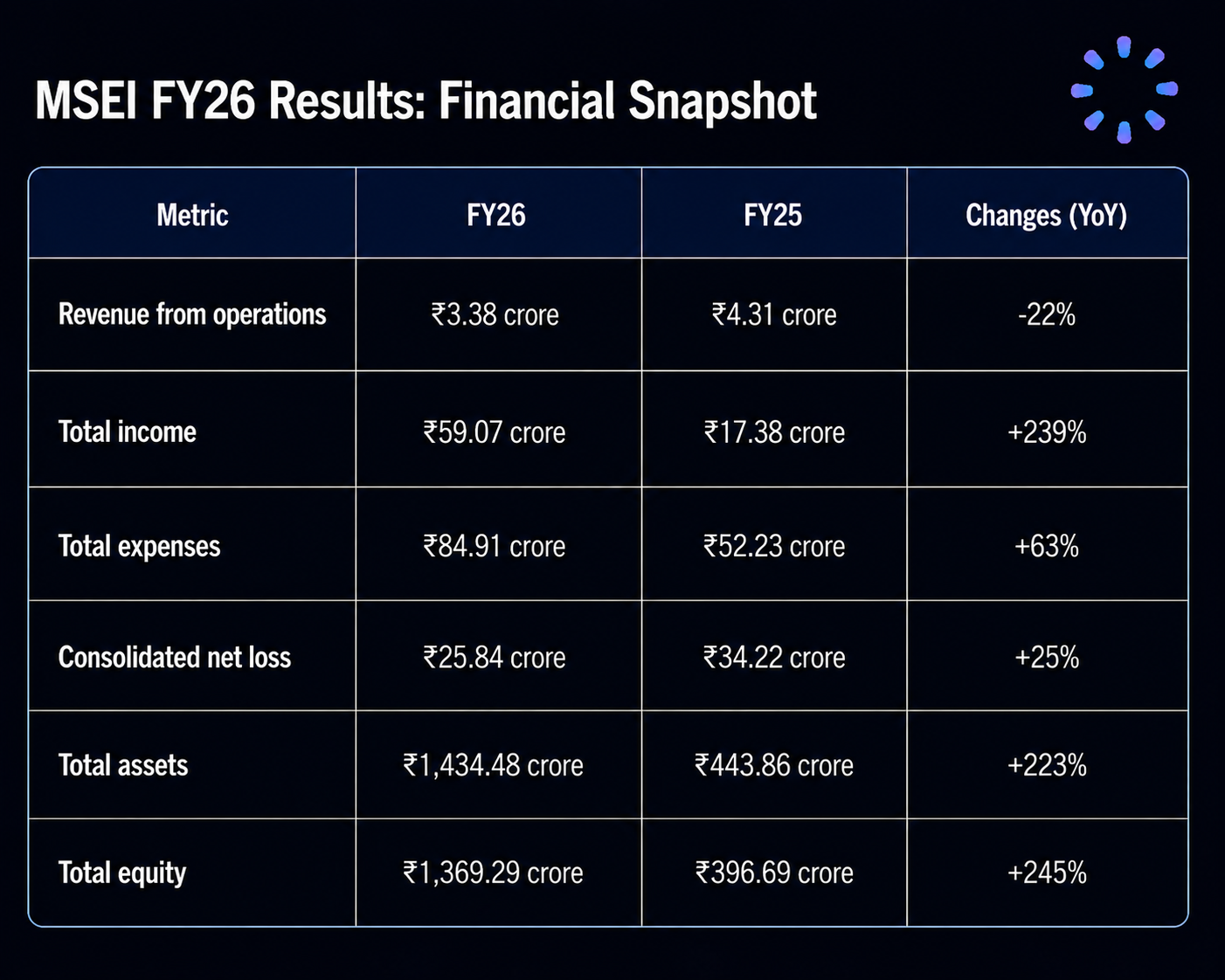

MSEI FY26 results show a business with much more capital than last year, a narrower net loss, and a core operating engine that still needs to prove itself. The Metropolitan Stock Exchange of India (MSEI) reported a consolidated net loss of ₹25.84 crore for FY26, better than the ₹34.22 crore loss in FY25, but revenue from operations fell from ₹4.31 crore to ₹3.38 crore.

That combination matters. MSEI did not narrow losses because its core exchange revenue surged. It narrowed losses mainly because other income rose sharply, supported by interest income and gains from financial assets after a large capital raise.

MSEI FY26 Results: Headline Financial Snapshot

Here is the simplest way to read MSEI FY26 results against FY25:

MSEI is financially stronger on the balance sheet, but the profit and loss statement still depends heavily on non-operating income.

That distinction is important for unlisted investors. A large asset base can provide runway, credibility, and optionality. However, exchange businesses ultimately need liquidity, trading activity, and recurring operating revenue to justify long-term confidence.

Why MSEI's Loss Narrowed in FY26

MSEI's FY26 net loss of ₹25.84 crore marks an improvement from the ₹34.22 crore loss reported in FY25. On the surface, that looks positive, and it is. A smaller loss gives the company more breathing room.

But the quality of the improvement deserves a closer look.

Core Revenue Fell

Revenue from operations declined to ₹3.38 crore in FY26 from ₹4.31 crore in FY25. For an exchange, this is the line investors should watch most closely because it reflects the strength of the operating franchise.

Operating revenue can include fees and income tied to exchange activity, depending on segment mix and accounting presentation. When this line falls, it tells investors that the business has not yet translated its strategic efforts into clear recurring revenue growth.

Other Income Did the Heavy Lifting

The major swing factor was other income, which rose to ₹55.69 crore from ₹13.07 crore in FY25. The disclosures indicate that this was largely supported by:

Interest income from financial assets, totaling ₹40.14 crore.

Net fair value gains on financial assets.

Income linked to the larger investment base after capital raising.

This is not automatically negative. Interest income can be real and useful, especially when a company has raised capital and invested it conservatively. But it is different from core exchange revenue.

For investors, the practical question is simple: Can MSEI use the capital base to build a stronger operating business, or will reported performance remain dependent on treasury income?

That makes MSEI loss narrowing a quality-of-earnings question, not just a headline improvement.

The Capital War Chest: What Changed on the Balance Sheet

Within the broader MSEI FY26 results, the most striking change is the balance sheet expansion. Total assets increased to ₹1,434.48 crore from ₹443.86 crore in FY25.

That is a massive change for a business that still reports a relatively small operating revenue base.

Private Placement Drove the Jump

In August 2025, MSEI allotted 500 crore equity shares with a face value of ₹1 each at a premium of ₹1 per share through private placement.

This MSEI capital raising changed the company's financial profile. Total equity increased to ₹1,369.29 crore, compared with ₹396.69 crore at the end of FY25.

MSEI now has a much larger cushion. That cushion can support technology upgrades, product development, regulatory capital needs, market development, and a longer path toward business revival.

Investment Portfolio Expanded

With the capital raise completed, MSEI's non-current investments rose to ₹400.01 crore. That helps explain the surge in other income and interest income during the year.

This also creates a clearer investor lens: MSEI is no longer just a loss-making exchange trying to survive. It is a capital-rich exchange trying to turn financial runway into market relevance.

That is a better position than having losses and limited capital. Still, capital alone does not create liquidity. The next phase depends on execution.

Expense Growth Shows the Cost of Rebuilding

MSEI's total expenses increased to ₹84.91 crore in FY26 from ₹52.23 crore in FY25. That is a sharp rise, and it matters because operating revenue remains low.

The increase was led by people costs, technology costs, and depreciation.

Employee Benefit Expenses

Employee benefit expenses rose to ₹25.32 crore. A portion of the increase was linked to the implementation impact of the New Labour Codes, which added about ₹0.13 crore in the final quarter because of the revised definition of wages.

For a financial market infrastructure company, people costs are not unusual. Exchanges need regulatory, technology, risk, compliance, product, and business development teams. But investors should watch whether these costs start producing higher revenue over time.

Technology and Depreciation

Technology expenses increased to ₹17.86 crore, while depreciation and amortisation more than doubled to ₹12.56 crore.

That suggests continued investment in digital infrastructure and operating capability. For an exchange, technology is not optional. Reliability, speed, market surveillance, cyber resilience, and member connectivity are core to trust.

The question is whether this investment leads to higher participation. If trading volumes and segment activity rise, these fixed costs can become easier to absorb. If volumes remain low, the expense base will continue to weigh on profitability.

Strategic Updates: Leadership Stability and Merger Consolidation

Beyond the numbers, two strategic updates stand out from the FY26 report.

Leadership Continuity

Shareholders approved the reappointment of Ms. Latika S Kundu as MD and CEO for a three-year term effective February 2025.

Leadership continuity matters because MSEI's turnaround is not a one-quarter story. Building exchange liquidity requires member confidence, regulatory alignment, technology investment, product focus, and time.

Merger of MSE Enterprises Limited

The FY26 results also reflect the integration of MSE Enterprises Limited (MEL) after the National Company Law Tribunal approved the merger, which became effective in June 2024.

This kind of consolidation can simplify group structure and reporting. For investors, the cleaner question is what the merged structure enables: lower duplication, better capital use, and clearer strategic focus.

What MSEI FY26 Results Mean for Unlisted Investors

If you track MSEI unlisted shares, the FY26 report gives both comfort and caution.

The comfort is clear: the company has a much stronger balance sheet. A ₹1,434.48 crore asset base and ₹1,369.29 crore equity base give MSEI more room to invest, compete, and wait for market initiatives to mature.

The caution is just as clear: core revenue is still small and declined year on year. The company remains loss-making, and the improvement in the bottom line came largely from other income.

For investors evaluating unlisted opportunities, the right approach is to separate three things:

Balance sheet strength: Does the company have enough capital to keep investing?

Operating traction: Are trading volumes, members, and revenue improving?

Entry valuation: Does the unlisted share price already assume a successful turnaround?

You can use the Precize screener to explore unlisted companies and compare opportunities with a research-led lens. For related operating context, read our MSEI trading volume April 2026 analysis. If you are new to unlisted shares, the Precize FAQs can help with process and eligibility questions.

Analyst View: MSEI Is Asset-Rich, but the Operating Test Remains

The analyst verdict on MSEI FY26 results is balanced.

MSEI has bought itself a runway. The capital raise materially improved the balance sheet, boosted financial assets, and helped generate other income. That matters because exchange turnarounds need patience and funding.

But the core exchange engine is not yet firing strongly. Revenue from operations of ₹3.38 crore remains small relative to the expense base and total assets. EPS remained negative at ₹(0.02), showing that shareholders are still waiting for operating leverage to turn.

The next stage is not about whether MSEI has cash. It is about whether it can use that cash to create a durable role in India's market infrastructure stack.

For MSEI, the long-term value drivers are likely to be:

Sustained trading volume growth across relevant segments.

Broader broker and member participation.

Technology reliability and product depth.

Tighter spreads and better liquidity, if market development initiatives work.

A shift from other income-led support to operating revenue-led growth.

Until that shift becomes visible, MSEI remains a capital-rich turnaround story rather than a proven operating turnaround.

What to Watch After MSEI FY26 Results

Investors should track the next few quarters with a specific checklist:

Revenue from operations: Does it recover from the FY26 decline?

Other income mix: How much of reported income still comes from treasury and fair value gains?

Expense discipline: Do people and technology costs keep rising faster than revenue?

Trading activity: Are volume improvements sustained, or do they appear in short bursts?

Capital use: Is the new equity being deployed toward measurable operating outcomes?

Regulatory and governance updates: Are leadership, compliance, and structure moving in the same direction?

FAQ for Investors Tracking MSEI

What were MSEI FY26 results in one sentence?

MSEI FY26 results showed that the Metropolitan Stock Exchange of India had a narrower consolidated net loss, a much stronger balance sheet after capital raising, lower operating revenue, and a major increase in other income.

Did MSEI become profitable in FY26?

No. MSEI still reported a consolidated net loss of ₹25.84 crore in FY26, although the loss narrowed from ₹34.22 crore in FY25.

Why did MSEI's loss narrow if operating revenue declined?

The loss narrowed mainly because other income rose sharply to ₹55.69 crore, helped by interest income from financial assets and fair value gains. Operating revenue declined to ₹3.38 crore.

How large was MSEI's FY26 capital raise?

MSEI allotted 500 crore equity shares at a face value of ₹1 each and a premium of ₹1 per share through private placement in August 2025.

Conclusion: A Stronger Runway, Not Yet a Finished Turnaround

MSEI FY26 results tell a clearer story than the headline loss number alone. The company is financially stronger, with a much larger asset base and equity cushion. It also narrowed its net loss, which is a positive sign.

However, the operating business still has work to do. Core revenue fell, expenses rose, and other income carried much of the improvement. That makes FY27 important: investors need to see whether MSEI can convert its capital war chest into higher volumes, stronger participation, and recurring operating revenue.

For now, MSEI is an asset-rich exchange with time to execute. The next proof point will be whether that time turns into traction.

Stay updated with MSEI and other unlisted companies through our Precize Community.

Disclaimer: This article is for informational purposes only and should not be considered investment advice. Investing in unlisted shares carries risks, including illiquidity, limited disclosures, valuation uncertainty, and potential loss of capital. This is not a recommendation to buy, sell, or hold shares of MSEI or any other security. Please consult a qualified financial advisor before making investment decisions. Precize is not a stock exchange and is not authorized by any capital markets regulator as a stock exchange.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved