Hero FinCorp FY26 Results: Loss, ROCE and IPO Readiness - What Investors Should Know

Hero FinCorp's FY26 numbers are best read as a transition-year report card. The company still has scale, capital efficiency, a recognised brand ecosystem, and a SEBI-approved public issue plan. At the same time, the swing from profit to loss has made profitability recovery the central question for investors.

For investors tracking Hero FinCorp unlisted shares, the IPO story cannot be separated from the FY26 financials. A public listing may improve capital access and price discovery, but valuation will depend on whether the company can convert its revenue base and ROCE strength back into sustainable profit.

If you are comparing Hero FinCorp with other pre-IPO opportunities, you can screen unlisted companies on Precize and then verify each company's financials through official documents.

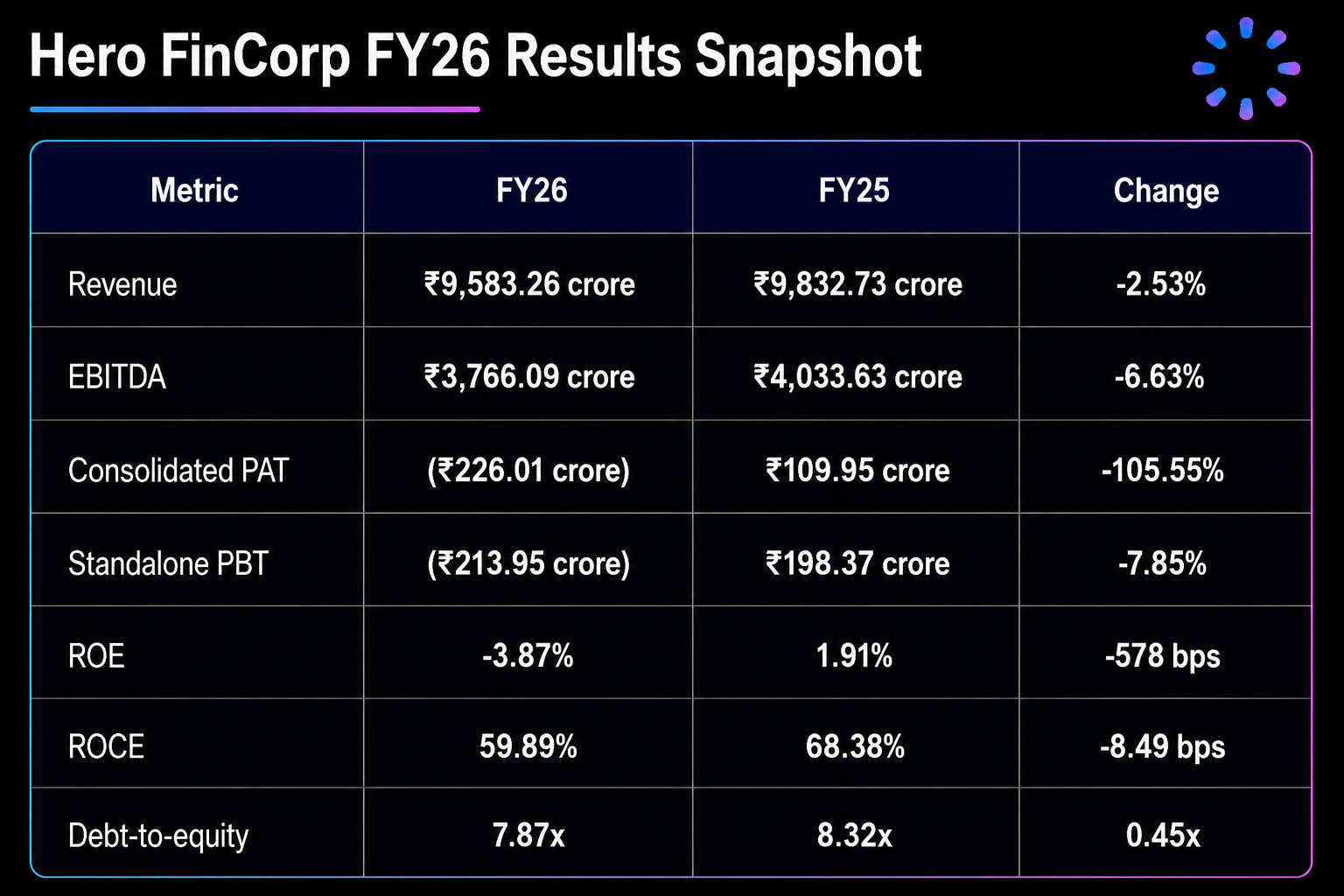

Hero FinCorp FY26 Results Snapshot

The headline from the Hero FinCorp FY26 results is not weak revenue. It is the gap between a still-large revenue base and a sharply weaker bottom line.

Revenue fell modestly to ₹9,583.26 crore from ₹9,832.73 crore in FY25. That is a 2.53% year-on-year decline, which suggests the business continued to operate at scale even in a tighter market.

EBITDA also remained substantial at ₹3,766.09 crore, although it declined 6.63% from ₹4,033.63 crore in FY25. The larger concern appears after EBITDA, where profitability moved into negative territory.

For this NBFC financial analysis, EBITDA means earnings before interest, tax, depreciation, and amortisation. PAT means profit after tax, PBT means profit before tax, ROE means return on equity, and ROCE means return on capital employed.

The table shows why the market reaction may be nuanced. Revenue and EBITDA are not pointing to a broken franchise. However, the loss at both consolidated and standalone levels shows that costs, credit charges, margins, tax effects, or other below-EBITDA factors materially affected earnings.

What Changed in Profitability?

The most important change in the FY26 results is the move from profit to loss. On a consolidated basis, Hero FinCorp reported a net loss of ₹226.01 crore, compared with a ₹109.95 crore profit in FY25.

The Hero FinCorp consolidated net loss is therefore the main headline investors will want management to explain before the IPO.

At the standalone level, the shift was also sharp. Profit before tax moved from ₹198.37 crore in FY25 to a ₹213.95 crore loss in FY26.

The Standalone PBT FY26 swing matters because it shows pressure at the individual entity level, not only at the consolidated group level.

For a lending business, this kind of reversal can come from several areas:

Credit costs: Higher provisioning or write-offs can reduce profit even if loan income remains steady.

Funding pressure: If borrowing costs rise faster than lending yields, net interest margins can compress.

Operating expense growth: Collections, technology, compliance, branch operations, and people costs can weigh on earnings.

Portfolio mix changes: Growth in certain borrower segments may carry different risk, margin, and provisioning profiles.

IPO-readiness costs: Governance upgrades, advisory costs, controls, and capital-market preparation can add transitional expense.

The supplied figures do not provide a full profit bridge, so the safer conclusion is this: Hero FinCorp's revenue base remained resilient, but FY26 exposed a profitability gap that investors will want management to explain clearly before the IPO.

Hero FinCorp ROCE: Why It Still Matters

The standout metric in the source brief is ROCE of 59.89%. Return on capital employed measures how efficiently a company uses capital to generate operating returns.

For investors, a high ROCE can indicate that the operating engine still has strength. It suggests the company is not simply consuming capital without productive output. In Hero FinCorp's case, that matters because the profit loss headline could otherwise dominate the entire story.

However, ROCE should not be read in isolation. A lender can show strong operating efficiency and still report weak shareholder returns if credit costs, leverage, funding costs, or provisions absorb the benefit. That is why the negative ROE of 3.87% matters. It shows that FY26 did not translate into positive returns for equity holders.

The practical read-through is balanced:

Positive signal: The franchise appears capable of generating operating returns from capital.

Negative signal: Those operating returns did not flow through to profit in FY26.

Investor question: Can management reduce the leakage between operating strength and net profitability?

This is the difference between a temporary earnings reset and a structural margin issue.

Hero FinCorp IPO: What SEBI Approval Means

The Hero FinCorp IPO remains the main valuation event for existing shareholders and unlisted-market investors. According to the supplied brief, SEBI approved the proposed ₹3,668 crore IPO in May 2025. This makes the SEBI approved IPO pathway a key part of the investment case, though final timing and pricing still need official confirmation.

The IPO structure includes:

Fresh issue: ₹2,100 crore.

Offer for sale: ₹1,568 crore.

Total issue size: ₹3,668 crore.

The fresh issue is important because the proceeds go to the company. For an NBFC, additional capital can support loan book growth, improve the capital buffer, and potentially strengthen lender confidence.

The offer for sale is different. It allows existing shareholders to sell part of their holdings, and those proceeds do not come into the company. Investors should review the final red herring prospectus to see the exact use of proceeds, selling shareholders, capital adequacy details, and risk factors.

For official IPO documentation, investors should track SEBI's public issue filings and company-specific updates before relying on informal market timelines. Broader regulatory context for NBFCs is available from the Reserve Bank of India.

Leadership Changes and Governance Signals

Hero FinCorp announced a leadership overhaul on 28 April 2026, including two roles that matter directly in a transition year.

Anand Kumar Saluja was appointed as Chief Financial Officer. The CFO role is central to capital planning, funding strategy, cost control, IPO readiness, and investor communication.

Amit Jain stepped in as Chief Risk Officer. For an NBFC, the CRO role is critical because underwriting quality, credit monitoring, provisioning discipline, and collections directly affect profitability.

Leadership changes do not automatically solve a profit issue. They do, however, tell investors where the company is focusing attention. In Hero FinCorp's case, new finance and risk leadership should be assessed through future results rather than announcements alone.

The key tests will be:

Whether margins stabilise.

Whether credit costs become more predictable.

Whether leverage and liquidity stay under control.

Whether IPO disclosures clearly explain the FY26 loss.

Whether management provides a credible path back to profit.

Funding Flexibility: CPs and NCDs

The board also approved the issuance of commercial papers (CPs) and non-convertible debentures (NCDs) to maintain liquidity and funding flexibility.

This is normal for a lending business, but it matters in the current context. NBFCs depend on access to debt markets. If a lender can raise money at competitive rates, it can protect spreads and support disbursement growth. If funding costs rise, profitability recovery can take longer.

Investors should watch future debt issuances for:

Coupon or yield.

Tenor.

Credit rating commentary.

Investor demand.

Security structure.

Use of proceeds.

The debt-to-equity ratio improved to 7.87x from 8.32x in FY25, which is a positive direction. Still, NBFC leverage needs continuous monitoring because small changes in asset quality or funding cost can have a large effect on equity returns.

What This Means for Unlisted Investors

For investors evaluating Hero FinCorp in the unlisted market, FY26 creates a more careful setup than a simple IPO momentum story.

The bull case is that Hero FinCorp has scale, a strong brand ecosystem, high reported ROCE, improving debt-to-equity, and a SEBI-approved IPO plan. A successful fresh issue could strengthen the capital base and support the next phase of lending growth.

The bear case is that FY26 delivered a consolidated loss of ₹226.01 crore and a standalone PBT loss of ₹213.95 crore. Investors will want evidence that the company can restore profitability before assigning a premium valuation.

If you are comparing Hero FinCorp with other private-market opportunities, use a consistent checklist across lenders and verify each company's financials through primary documents. For broader market explainers, you can also follow IPO and unlisted share updates on the Precize blog.

Investor Checklist Before the IPO

Before taking a view on Hero FinCorp, investors should track:

Profitability recovery: Does the company return to profit in the next reporting period?

Credit cost trend: Are provisions and write-offs stabilising?

Funding cost: Can CPs, NCDs, and IPO capital reduce pressure on margins?

ROE improvement: Does shareholder return move back into positive territory?

IPO valuation: Does the final price band reflect FY26 risks as well as long-term opportunity?

Capital adequacy: Does the fresh issue materially improve the lending runway?

Management commentary: Does the new CFO and CRO team provide a credible recovery plan?

Investors new to unlisted shares should also review common investor questions on Precize before comparing specific companies.

Bull Case and Bear Case

Bull Case

The positive investment case is supported by the company’s large revenue base, strong return on capital employed (ROCE), and relatively lower debt-to-equity ratio. In addition, the receipt of SEBI approval for its IPO and the expected infusion of fresh capital from the proposed issue could strengthen the balance sheet, support future growth initiatives, and improve overall financial flexibility.

However, investors should watch whether the company can successfully convert its operating strength into sustainable net profitability. While operational metrics remain encouraging, consistent earnings growth and improved bottom-line performance will be key factors in validating the long-term investment thesis.

Bear Case

On the other hand, the cautious view stems from the company’s consolidated loss position, standalone profit-before-tax (PBT) loss, negative return on equity (ROE), and uncertainty regarding the sustainability of margins. These factors raise concerns about the company's ability to generate consistent shareholder returns and maintain profitability in a competitive environment.

That said, the outlook could improve if the company successfully completes its capital raise, benefits from lower borrowing costs, and demonstrates stronger execution on strategic and operational initiatives. Clear progress on profitability and margin expansion would help address many of the concerns currently weighing on investor sentiment.

The balanced view is that Hero FinCorp remains an important NBFC IPO candidate, but FY26 has increased the importance of valuation discipline. Investors should avoid judging the company only by IPO status or only by one loss year.

Closing View

Hero FinCorp's FY26 results show a company moving toward the public markets while working through profitability pressure. The revenue base remains large, ROCE is strong, and the IPO can improve the capital base. But the swing into loss cannot be ignored.

For investors, the key question is now simple: can Hero FinCorp restore profit before the IPO valuation is finalised? If the company can stabilise margins, control credit costs, and communicate a credible recovery plan, FY26 may be remembered as a reset year. If losses continue, IPO pricing may need to reflect that risk.

FAQs on Hero FinCorp FY26 Results

1. Did Hero FinCorp report a profit or loss in FY26?

Hero FinCorp reported a loss in FY26. Based on the supplied figures, the company posted a consolidated net loss of ₹226.01 crore and a standalone PBT loss of ₹213.95 crore.

2. What was Hero FinCorp's FY26 revenue?

Hero FinCorp reported FY26 revenue of ₹9,583.26 crore, down 2.53% from ₹9,832.73 crore in FY25. The decline was modest, but profitability weakened sharply.

3. What was Hero FinCorp's ROCE in FY26?

Hero FinCorp's reported ROCE was 59.89% in FY26. This indicates strong capital efficiency, but investors should also consider the negative ROE and net loss.

4. What is the latest Hero FinCorp IPO update?

According to the supplied brief, SEBI approved Hero FinCorp's proposed ₹3,668 crore IPO in May 2025. The issue includes a ₹2,100 crore fresh issue and a ₹1,568 crore offer for sale.

Use the IPO as a catalyst, not as the entire investment thesis. Start with official filings, compare peer NBFCs, and size any unlisted exposure carefully. For platform-related help, you can reach Precize Care. Stay updated with NCDEX and other unlisted companies through our Precize Community. If this article was useful, you can share it with other investors through the Precize Referral Program.

Disclaimer: This article is for informational purposes only and should not be considered investment advice. Investing in unlisted shares carries risks including illiquidity and potential loss of capital. Please consult with a qualified financial advisor before making investment decisions. Precize is not a stock exchange and is not authorized by any capital markets regulator. This is not a recommendation to buy or sell shares of Hero FinCorp.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved