Top 10 Methods for M&A Valuation for Unlisted Companies

Valuing unlisted companies in mergers and acquisitions (M&A) presents unique challenges, primarily due to the absence of publicly available market prices. In India, the space of private equity and venture capital has been increasingly active, with 1,839 deals announced in 2023, growing by 42% to 2,606 deals in 2024

This increase in private deals highlights how critical it is to use reliable valuation methods when assessing unlisted companies. Investors and acquirers need accurate valuations to determine fair pricing, evaluate strategic opportunities, and reduce investment risk.

In this blog, we explore the top 10 methods used to value unlisted companies, explaining practical approaches and considerations for M&A and private equity transactions.

Key Takeaways:

Unlisted company valuation requires multiple methods—market comparables, precedent transactions, DCF, and asset-based approaches—to ensure a robust and defendable value.

Adjustments for illiquidity, private ownership, industry, and geographic factors are essential to reflect realistic exit potential and market conditions.

Terminal value estimation captures long-term value beyond projection periods, using either perpetuity growth or exit multiples.

Blending methods and applying weighted averages reduces reliance on any single assumption and provides a well-rounded valuation.

Practical application of these methods supports M&A, private equity, and strategic investment decisions, with structured processes improving transparency and defensibility.

List of Top 10 Methods for M&A Valuation for Unlisted Companies

Valuing unlisted companies for mergers and acquisitions (M&A) requires a structured approach to capture their true worth, despite the absence of public market pricing.

Investors and acquirers must combine market benchmarks, historical transaction data, projected cash flows, and adjustments for private ownership, illiquidity, and sector-specific risks.

The following ten methods provide a comprehensive toolkit to assess value, compare alternatives, and ensure informed investment or negotiation decisions

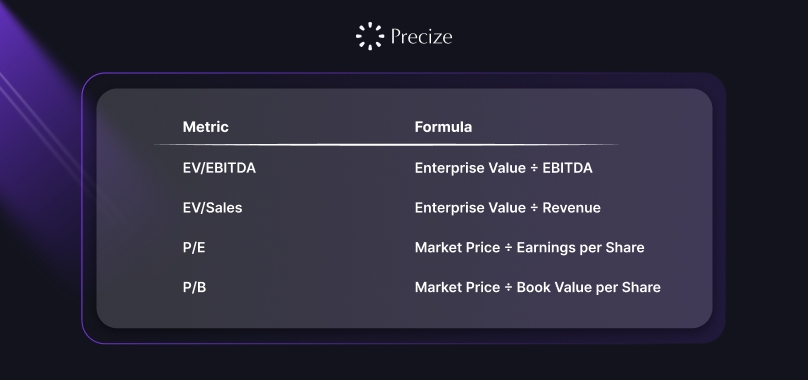

1. Comparable Company Analysis (CCA)

CCA benchmarks an unlisted company against publicly traded peers in the same sector to provide a market-based valuation reference. It is used when investors need to gauge what similar companies are trading at and when sufficient public data exists to reflect sector trends.

This approach is particularly useful in M&A negotiations or private equity deals where market multiples help validate internal forecasts and pricing assumptions.

Application & Considerations

Identify 3–5 listed peers with similar business models, size, and geography.

Adjust multiples for growth, profitability, leverage, and operational differences.

Apply illiquidity discounts and account for minority stakes.

Use as a sanity check alongside DCF or precedent transaction valuations.

Key Metrics & Formula

Also Read: Internal Rate of Return (IRR): Types, Formula, Calculation, Example

2. Precedent Transaction Analysis

Examines historical M&A deals of similar companies to derive valuation multiples and acquisition premiums. Applied when reliable past transactions exist in the same sector, it reflects actual premiums paid and strategic considerations in comparable deals.

Useful for structuring offers and benchmarking unlisted targets.

Application & Considerations

Select comparable transactions within the last 3–5 years for sector relevance.

Adjust for market conditions, deal structure, and time-related changes.

Reflect any control premiums or minority discounts applicable to the target.

Combine with other methods for triangulated valuation.

Key Metrics & Formula

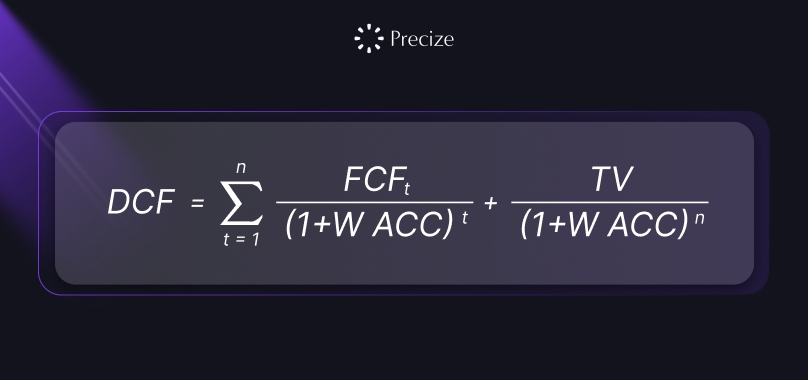

3. Discounted Cash Flow (DCF) Analysis

DCF estimates the present value of projected free cash flows, capturing intrinsic value based on company-specific growth, margins, and capital requirements.

It is applied when detailed projections are available and investors want to model risk-adjusted scenarios. Commonly used in strategic acquisitions, PE investments, and long-term planning.

Application & Considerations

Forecast cash flows for 5–10 years, incorporating realistic growth and expense assumptions.

Calculate WACC including equity and debt components.

Test sensitivity to discount rates and terminal growth assumptions.

Combine with market-based approaches for robustness.

Key Formula

Looking Beyond the Public Markets? At Precize, we know privacy and trust are non-negotiable. Your data stays with you; we never sell, share, or monetize it. With one click, your investment specialist is online to guide you through private equity and private credit opportunities that match your goals.

4. Asset-Based Valuation

Values a company based on net assets minus liabilities. Primarily used for asset-heavy or distressed firms. Investors apply this when assets constitute the bulk of value and for risk-averse floor valuations.

Application & Considerations

Include tangible and intangible assets, adjusting for fair market value.

Factor in off-balance sheet liabilities or contingencies.

Use liquidation value when evaluating distressed scenarios.

Less useful for high-growth or intangible-heavy businesses.

Key Formula

Adjusted Net Asset Value = Total Assets (fair value) – Total Liabilities

Liquidation Value = Expected asset proceeds – transaction costs

5. Earnings Capitalisation

Capitalises normalised earnings using industry-specific capitalisation rates. Best applied for mature companies with stable, predictable earnings. It helps investors convert recurring profits into enterprise value.

Application & Considerations

Normalise earnings for seasonality, one-offs, or extraordinary items.

Select capitalisation rates reflecting risk, sector, and marketability.

Apply discounts for minority ownership or illiquidity.

Useful for mature companies with stable cash flows rather than high-growth startups.

Formula

Company Value = Normalised Earnings ÷ Capitalisation Rate

Also Read: Cash Application Process in Accounting: Impact, Challenges, & Best Practices

6. Sum-of-the-Parts (SOTP) Analysis

Values each business segment separately and aggregates them for total enterprise value. Applied to diversified companies or conglomerates, it helps uncover hidden or segment-specific value.

Application & Considerations

Segment revenue, EBITDA, and assets for each business line.

Apply appropriate multiples or DCF per segment.

Allocate shared costs and synergies carefully.

Summarize segment valuations to determine total company value.

Formula

Total Company Value = Σ (Value of each segment)

Also Read: Methods of Debt Redemption in Finance and Business

7. Guideline Public Company Analysis

Uses listed companies as benchmarks to validate CCA multiples. Applied when investors want a market check on unlisted valuations, particularly for private equity or M&A purposes.

Application & Considerations

Adjust for size, margins, growth, and liquidity differences.

Apply illiquidity discounts and minority shareholding considerations.

Cross-check assumptions against DCF and precedent transactions.

Provides additional validation for investor negotiations.

8. Adjustments for Illiquidity and Private Status

Private companies are less liquid, increasing risk and exit constraints. These adjustments are applied across all valuation methods for private equity, M&A, or pre-IPO investments to reflect marketability, minority stakes, and exit horizons.

Application & Considerations

Apply marketability discounts of 15–30% depending on liquidity constraints.

Adjust multiples, cash flows, and terminal values for private ownership risk.

Include minority or control premiums appropriately.

Maintain consistency across all methods.

9. Industry and Geographic Factors

Sector dynamics, economic conditions, and regional regulations influence cash flows, multiples, and risk profiles. Applied to adjust growth forecasts, discount rates, and terminal values, reflecting market and regulatory realities.

Application & Considerations

Incorporate industry growth rates, regulatory constraints, and competitive landscape.

Adjust discount rates for currency, political, and macroeconomic risks.

Apply sector-specific risk premiums in DCF or capitalisation approaches.

Benchmark assumptions against comparable markets and regions.

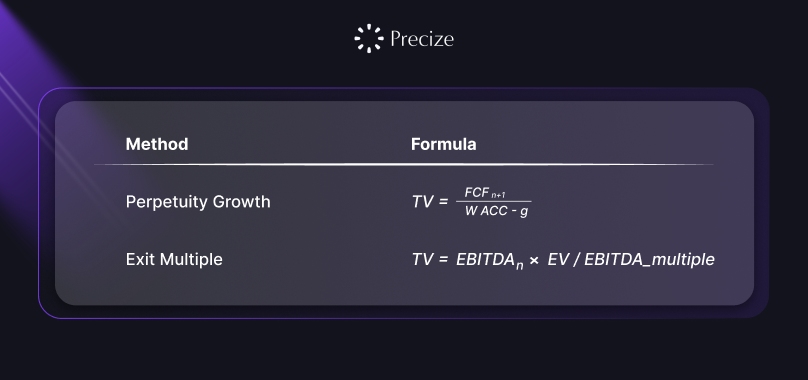

10. Terminal Value Estimation

Terminal value captures the value beyond the projection horizon in a DCF and is essential for long-term valuation. Applied when cash flows are projected for a finite period, it estimates ongoing enterprise value using perpetuity growth or exit multiples.

Application & Considerations

Choose perpetuity growth rates reflecting realistic long-term growth or exit multiples from comparable transactions.

Adjust terminal value for illiquidity and private ownership discounts.

Include in DCF to complete enterprise value calculation and ensure consistency with all other valuation assumptions.

With each method explored individually, let’s see how blending them can provide a more accurate and defendable overall valuation.

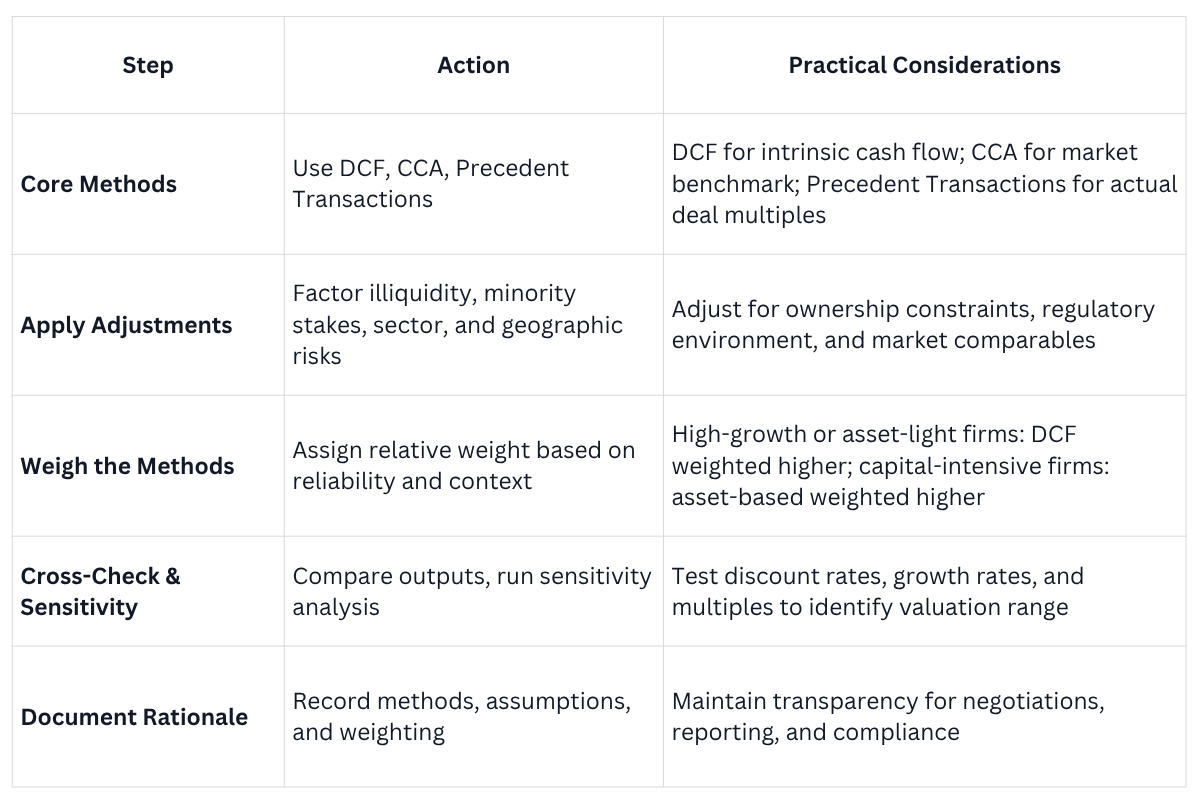

How to Combine Valuation Approaches for a More Accurate Assessment?

Relying on just one method to value unlisted companies can give a partial or misleading picture because of limited market data, low liquidity, and company-specific factors.

Using a combination of approaches, market comparables, precedent transactions, DCF, and asset-based methods gives a fuller, more reliable view of a company’s worth.

This blended approach combines projected cash flows, real market behaviour, and tangible assets to create a well-rounded and defendable valuation that investors and acquirers can use with confidence for M&A, private equity, or strategic decisions.

Note:

Blending multiple valuation methods reduces reliance on any single assumption and captures multiple dimensions of value such as cash flows, market sentiment, and asset backing, resulting in a defendable and actionable valuation for unlisted companies

Conclusion

Valuing unlisted companies requires careful analysis and multiple perspectives. No single method captures every dimension of value, which is why combining approaches offers a more complete and defendable picture.

Adjusting for illiquidity, private ownership, and industry-specific factors ensures that the valuation is realistic and aligned with market and strategic realities.

For investors looking to put these valuation principles into practice, platforms like Precize offer curated access to private equity and pre-IPO shares.

With structured research, KYC-compliant processes, and portfolio tracking from ₹10,000, Precize makes participating in unlisted opportunities transparent, secure, and actionable.

Reserve access today and apply informed valuation insights to your investment decisions.

FAQs

Q1: How do minority stakes affect valuation in unlisted companies?

A: Minority stakes reduce liquidity and control rights, often leading to discounts applied to valuation multiples. Investors should consider the lack of decision-making influence and potential exit challenges when adjusting value. This adjustment ensures fair pricing for both acquirers and existing shareholders.

Q2: How can industry cyclicality impact unlisted company valuations?

A: Sector-specific cycles—like commodity price swings, technology adoption, or regulatory changes—affect growth projections and risk premiums. Valuers should adjust cash flow forecasts, discount rates, and terminal growth assumptions to reflect the cyclical environment accurately.

Q3: When is an asset-based valuation preferable to a DCF?

A: Asset-based valuation is preferred for capital-intensive, distressed, or asset-heavy firms where cash flows are uncertain or negative. It provides a floor value based on tangible assets, ensuring risk-averse investors do not overpay despite volatile projections.

Q4: How do geographic risks influence valuation?

A: Exposure to multiple countries or regions introduces currency risk, political uncertainty, and varying regulatory environments. Adjust discount rates and growth assumptions for these factors to ensure valuations reflect the true risk-adjusted potential.

Q5: Can ESG factors be incorporated into unlisted company valuation?

A: Yes, environmental, social, and governance considerations can affect future cash flows, brand value, and regulatory compliance costs. Integrating ESG risks into projections and discount rates ensures valuations align with sustainable performance and long-term investor expectations.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved