Mohan Meakin: Old Monk Maker's Legacy, FY25 Financials, and 70% Shareholder Return

The company has drawn fresh investor attention after reported shareholder returns of nearly 70% during the recent rally phase, supported by stronger FY25 numbers, cash generation, and renewed interest in heritage consumer brands.

That return figure should be read carefully. Mohan Meakin is an unlisted company, so prices can vary across private-market deals, liquidity is limited, and past performance does not guarantee future results. Still, the company is worth studying because it combines three rare traits: a 170-year operating history, a cult consumer brand, and improving financial performance.

What Is Mohan Meakin?

Mohan Meakin is an Indian alcoholic beverage and consumer products company best known for Old Monk Rum. Its roots go back to the colonial-era brewing business started in Kasauli in 1855, and its modern identity was shaped after Indian businessman Narendra Nath Mohan acquired control from British shareholders after independence.

Today, the company remains a well-known name in India's liquor industry because of its heritage brands, especially Old Monk. For investors, Mohan Meakin is also interesting because it is not listed on the National Stock Exchange (NSE) or Bombay Stock Exchange (BSE). Its shares are generally discussed in the unlisted shares market.

If you are researching similar private-market opportunities, you can use the Precize Screener to compare available unlisted companies, financials, and sector exposure.

The Origins of Mohan Meakin

Mohan Meakin's history begins in 1855, when Edward Dyer established a brewery in Kasauli during British rule. The business initially operated under names such as E. Dyer & Co. and later became part of the Dyer brewing group.

In the late 19th century, H.G. Meakin, who came from a brewing background in Burton-on-Trent, acquired and expanded brewery assets in India. During the First World War period, the Dyer and Meakin businesses were merged to form Dyer Meakin & Co. Ltd.

The company's official history describes this period as the foundation of a large India-linked brewing enterprise, with facilities across locations such as Kasauli, Solan, Simla, Lucknow, and other centres. This long operating record is one reason Mohan Meakin continues to stand apart from newer alcohol brands.

Source note: The 1855 founding, Dyer-Meakin merger, and later name changes are described on Mohan Meakin's official history page.

Was Mohan Meakin Listed on the London Stock Exchange?

One of the most interesting parts of Mohan Meakin's story is its overseas capital-market connection. The company was historically linked to British ownership and was associated with London-based shareholders under the Dyer Meakin Breweries name.

This matters because it shows the company's role in the colonial-era business ecosystem. Mohan Meakin was not just a local brewery. It was part of a larger British-controlled commercial network that supplied beer and spirits across several regions.

For modern investors, the London connection is more historical than financial. The company is no longer a London-listed business. Its present-day relevance comes from its unlisted share status in India, its brand portfolio, and its financial performance.

How Narendra Nath Mohan Acquired the Company

After independence, control of the company shifted from British ownership to Indian entrepreneurship. In 1949, businessman Narendra Nath Mohan travelled to London and acquired a controlling stake in Dyer Meakin Breweries from British shareholders.

That transaction changed the company's direction. Under Mohan family leadership, the business expanded across India and built facilities in places such as:

Ghaziabad

Lucknow

Khopoli

Solan

The acquisition also symbolised a larger post-independence shift. Several colonial-era businesses moved into Indian ownership during this period, and Mohan Meakin became one of the better-known examples in the consumer beverages space.

From Dyer Meakin to Mohan Meakin

As the Mohan family strengthened control, the company's name also changed.

In 1966, the company became Mohan Meakin Breweries Ltd.

In 1980, the word "Breweries" was removed as the business diversified.

The company is now known as Mohan Meakin.

This change reflected a broader product mix. While liquor remains central to the business, Mohan Meakin has also operated across categories such as:

Rum

Whisky

Beer

Brandy

Juices

Cornflakes and cereals

Other FMCG products

The business is still closely associated with the historic Solan Brewery in Himachal Pradesh, which adds to its heritage appeal.

The Old Monk Legacy

For many Indian consumers, Mohan Meakin means Old Monk Rum.

Old Monk has built a rare kind of consumer loyalty. It has survived changing drinking habits, premiumisation, imported spirits, and aggressive marketing by larger players. Its strength comes less from glossy advertising and more from memory, affordability, availability, and word-of-mouth.

The brand's appeal rests on four factors:

Nostalgia: Old Monk has been part of Indian drinking culture for decades.

Affordability: It has remained accessible compared with many premium spirits.

Recognition: The bottle, name, and brand identity are instantly familiar.

Distribution: The brand has long-standing reach across many Indian markets.

Mohan Meakin's flagship portfolio is commonly associated with:

Old Monk Rum

Golden Eagle Beer

Solan No.1 Whisky

This heritage positioning gives Mohan Meakin a different identity from newer premium alcohol brands. It also explains why investors often view the company as a consumer brand story, not only a liquor manufacturing business.

Why Mohan Meakin Was Delisted

Mohan Meakin was later listed on Indian regional stock exchanges, including the Delhi Stock Exchange and Calcutta Stock Exchange. However, it eventually moved toward delisting as trading activity on regional exchanges declined.

The broader reason was simple: Indian capital-market liquidity shifted toward larger national exchanges such as NSE and BSE. Regional exchanges gradually lost relevance, and many listed companies saw little real trading in their shares.

According to a 2003 report in The Times of India, Mohan Meakin shareholders approved delisting from the Delhi and Calcutta stock exchanges because the shares were not actively traded and the company had no immediate plan to raise public funds.

For investors, this history explains why Mohan Meakin now appears in the unlisted shares conversation. It is not a newly founded private company. It is an older company whose listed-market presence faded as India's exchange structure changed.

If you are new to this category, the Precize FAQs explain common questions around unlisted shares, liquidity, transaction process, and risks.

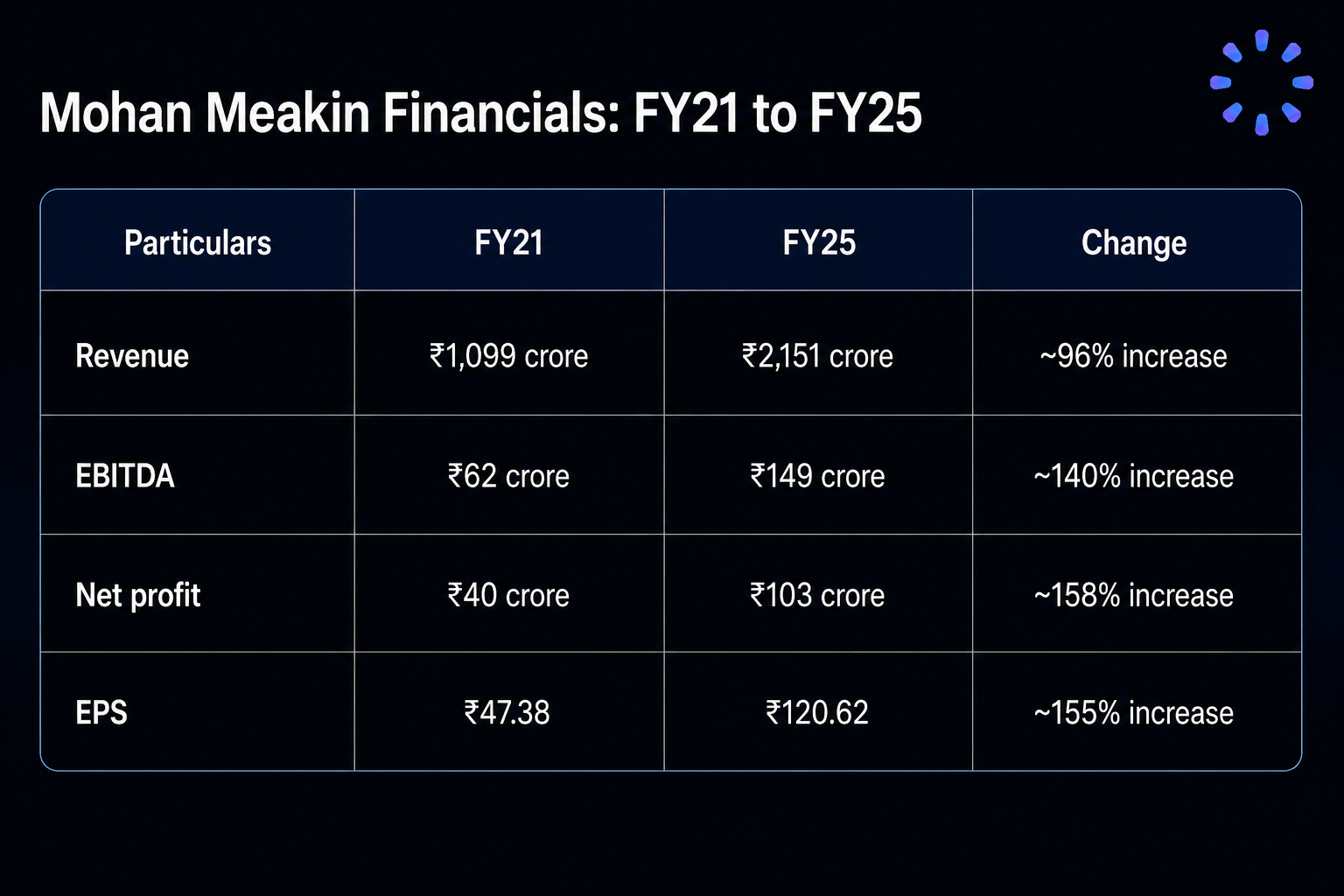

Mohan Meakin Financials: FY21 to FY25

Mohan Meakin financials are one reason investors have started paying closer attention. Based on company financial data referenced in unlisted-market research, revenue, EBITDA, net profit, and earnings per share improved meaningfully between FY21 and FY25.

Revenue Nearly Doubled

Revenue rose from about ₹1,099 crore in FY21 to about ₹2,151 crore in FY25. This points to steady demand across the company's beverage portfolio and improved scale in its core business.

Profitability Improved

EBITDA increased from about ₹62 crore to about ₹149 crore over the same period. Net profit rose from about ₹40 crore to about ₹103 crore.

Margins also improved:

EBITDA margin: around 5.67% in FY21 to 6.92% in FY25.

PAT margin: around 3.67% in FY21 to 4.77% in FY25.

These are not high margins compared with some premium consumer companies, but the direction is positive.

Balance Sheet Looks Conservative

The company has been described as having very low debt, with a reported debt-to-equity ratio of about 0.01x in the data shared with the original article. Some third-party unlisted share platforms show different debt ratios, so investors should cross-check the latest annual report rather than rely on a single source.

The key point is that Mohan Meakin does not appear to be a heavily leveraged business. That matters in a regulated industry where working capital, raw material prices, and excise duties can affect cash flow.

Operating Cash Flow Strengthened

Operating cash flow reportedly increased from about ₹29.7 crore in FY21 to ₹96.5 crore in FY25. Stronger cash generation gives the company more room to fund operations without taking on excessive debt.

Capital Efficiency Remained Strong

Mohan Meakin reportedly maintained ROCE above 28% in recent years. Return on capital employed (ROCE) measures how efficiently a company uses capital to generate operating profit. For an old manufacturing and consumer brand business, a high ROCE suggests disciplined capital use.

From Near Decline to Revival

What makes Mohan Meakin’s journey even more interesting is how the company quietly recovered from a difficult phase.

Back in 2015, the company reportedly generated only around ₹3 crore in annual profit. Sales volumes had also declined sharply, with bottle sales falling from nearly 80 lakh bottles to nearly 30 lakh bottles.

By 2017, many industry observers believed the Old Monk brand had lost relevance as consumer preferences shifted toward premium whisky and modern alcohol brands.

However, the company slowly rebuilt itself without aggressive marketing or external funding.

Today, the story looks very different.

FY24 revenue crossed nearly ₹1,930 crore

The company exports to 21 countries

Sales volumes reportedly crossed more than 12 crore bottles annually (around 1 crore cases)

Mohan Meakin is also setting up a new distillery project worth nearly ₹100 crore

What stands out is that the company continues to expand largely through internal accruals rather than heavy borrowing.

No major debt burden

No dependence on external investors

Conservative capital allocation

In many ways, Mohan Meakin still operates the same way it always has — quietly, steadily, and without excessive market noise.

Mohan Meakin Share Price and the Reported 70% Return

Mohan Meakin has reportedly delivered nearly 70% returns to shareholders during the recent rally phase. The move appears to be driven by a combination of better financial performance and renewed demand for heritage consumer brands in the private market.

Because Mohan Meakin is unlisted, there is no single live Mohan Meakin share price on NSE or BSE. Investors usually see deal-level quotes, platform quotes, or negotiated prices. That makes verification important before using any return number for valuation.

Several factors may have supported the re-rating:

Consistent earnings growth: Revenue and net profit both improved between FY21 and FY25.

Better margins: EBITDA and PAT margins expanded from a low base.

Strong brand recall: Old Monk remains one of India's best-known alcohol brands.

Low debt: A conservative balance sheet can make investors more comfortable.

Cash generation: Higher operating cash flow adds credibility to reported profit growth.

Consumer-sector interest: Investors often assign higher value to businesses with durable brands and repeat demand.

However, unlisted share returns are not the same as exchange-traded stock returns. There may be wider bid-ask spreads, fewer buyers, and less frequent price discovery. A quoted return can look attractive on paper, but the actual exit price depends on demand at the time of sale.

For ongoing IPO-related updates, you can read more on our blog.

Industry Outlook for Indian Liquor Stocks

India's alcoholic beverage industry continues to benefit from long-term consumption changes. Urbanisation, rising disposable incomes, and premiumisation have helped organised liquor stocks in India build stronger brands across spirits and beer.

Recent industry commentary points to a mixed but broadly constructive outlook:

Premiumisation continues to support value growth.

Beer volumes may grow faster than some spirits categories.

State-level price approvals can support revenue growth.

Input costs and excise changes can still affect margins.

For Mohan Meakin, this creates both opportunity and pressure. The company has a powerful heritage brand in Old Monk, but larger listed competitors have deeper marketing budgets, wider premium portfolios, and stronger visibility with institutional investors.

The next stage of value creation may depend on whether Mohan Meakin can use its legacy to strengthen premium products without weakening the affordability and nostalgia that made Old Monk successful.

Mohan Meakin vs Listed Liquor Stocks

Mohan Meakin is often compared with listed liquor companies, but the comparison needs care.

This does not make one category automatically better. It means the risk-return profile is different. Listed liquor stocks offer better liquidity and public disclosures. Mohan Meakin offers exposure to a heritage brand through the unlisted market, but with lower liquidity and less frequent information flow.

Should Investors Track Mohan Meakin Unlisted Shares?

Mohan Meakin may be worth tracking for investors who understand unlisted share risks and want exposure to established private consumer businesses. The company's appeal comes from Old Monk's brand equity, improving FY25 financials, strong cash generation, and a long operating history.

At the same time, investors should avoid buying only because of the reported 70% return. That return reflects the past. Future value will depend on earnings growth, portfolio strategy, liquor regulation, transaction pricing, and whether buyers remain interested in the unlisted market.

A disciplined investor should ask:

Are the latest financials independently verified?

What price and valuation multiple am I paying?

How easy will it be to sell if I need liquidity?

Is the company growing beyond Old Monk?

How does the valuation compare with listed liquor peers?

These questions matter more than the headline return number.

Final Thoughts

Mohan Meakin represents a rare combination of history, consumer recall, and improving financial performance. From its roots in the 1855 Kasauli brewery to its transformation under Narendra Nath Mohan, the company mirrors part of India's shift from colonial enterprise to Indian-owned consumer brand.

The recent investor interest is understandable. Revenue has nearly doubled between FY21 and FY25, net profit has improved, cash generation has strengthened, and Old Monk remains a powerful brand.

But the right lens is balance. Mohan Meakin is a heritage business with real strengths, not a guaranteed wealth-creation story. Investors should study the financials, compare valuation with listed liquor peers, and understand unlisted share liquidity before making any decision.

If you are evaluating private-market opportunities, use the Precize screener or reach Precize Care for platform support. Stay updated on unlisted companies with our Precize Community.

This is not a recommendation to buy or sell Mohan Meakin shares. Do your own research before investing.

Disclaimer: This content is for informational purposes only and does not constitute investment advice. Investing in unlisted shares involves risks including illiquidity and potential loss of capital. Past performance does not guarantee future results. Returns on unlisted shares are not guaranteed. Consult a qualified financial advisor before making investment decisions. Precize is not a stock exchange and is not regulated by SEBI.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved