OYO IPO 2026 - Can India's Hospitality Unicorn Make a Successful Comeback?

For years, OYO was one of India's most talked-about startups. It transformed the fragmented hotel industry by bringing thousands of independent hotels under one technology-driven brand. At its peak, the company expanded rapidly across multiple countries and became one of India's most valuable startups.

However, the COVID-19 pandemic severely impacted the travel industry. OYO faced declining occupancy, significant losses, multiple rounds of restructuring, and postponed its IPO plans several times. Many investors questioned whether the company would ever return to profitability.

Fast forward to 2026, and the story looks very different.

OYO's parent company, Oravel Stays, has filed its Draft Red Herring Prospectus (DRHP) for a ₹6,650 crore fresh issue IPO. Unlike its earlier attempt, the company is now presenting itself as a more disciplined, profitable, and globally diversified hospitality platform rather than a high-growth startup burning cash.

But is this truly a turnaround story? Or is there still significant risk for investors?

OYO IPO Overview

OYO's parent company, Oravel Stays Limited, has filed a Draft Red Herring Prospectus (DRHP) for an Initial Public Offering (IPO) comprising a fresh issue of equity shares worth ₹6,650 crore.

Unlike many technology startups that use IPO proceeds primarily for aggressive expansion, OYO plans to strengthen its balance sheet by using a significant portion of the proceeds to repay or prepay existing borrowings. The remaining funds will be used for general corporate purposes and future business initiatives.

The proposed IPO marks the company's second major attempt to list on the Indian stock exchanges after postponing its earlier plans due to changing market conditions and operational restructuring.

About OYO

Founded in 2013, OYO started with a simple idea—standardize affordable hotels using technology.

Instead of owning hotels, the company partnered with independent hotel owners by providing branding, pricing technology, booking platforms, customer support, and marketing services. In return, hotel partners shared a portion of their revenue or paid franchise fees.

Over the years, OYO expanded beyond India into Europe, Southeast Asia, the Middle East, and North America.

Today, the company operates across 35+ countries with a diversified hospitality portfolio comprising:

More than 24,300 hotels

Around 124,600 vacation homes

Approximately 144,500 online accommodation listings

Over 119 million customers served since inception

Rather than positioning itself only as a budget hotel company, OYO has evolved into a global hospitality technology platform serving multiple accommodation categories.

How OYO's Business Model Works

One of the biggest misconceptions about OYO is that it owns thousands of hotels.

In reality, OYO follows an asset-light business model, which means it generally does not own the properties listed on its platform.

Instead, hotel owners partner with OYO to improve occupancy, pricing efficiency, and customer reach.

The process is straightforward:

Hotel owners join the OYO network.

OYO provides branding, technology, pricing tools, marketing support, and reservation systems.

Customers book rooms through OYO's platform.

Guests stay at partner hotels.

OYO earns revenue through revenue sharing, franchise fees, management fees, and other hospitality services.

Since the company doesn't need to purchase hotel properties, it can expand into new markets with significantly lower capital investment compared to traditional hotel chains.

This asset-light strategy allows OYO to focus on technology, operations, and customer acquisition while hotel owners manage the physical infrastructure.

How OYO Makes Money

OYO's revenue model has evolved significantly over the last few years.

Earlier, the business relied heavily on revenue-sharing agreements with partner hotels. Today, the company has diversified its income sources across multiple hospitality businesses, reducing dependence on any single revenue stream.

Revenue Sharing

Revenue sharing continues to be one of OYO's primary income sources.

Whenever a guest books a room at a partner hotel through OYO's platform, the company earns a percentage of the booking revenue. This model aligns OYO's earnings with hotel occupancy and booking performance.

Franchise Fees

Many hotel owners choose to operate under the OYO brand while continuing to manage their own properties.

In such cases, OYO earns franchise fees by allowing hotel owners to use its brand name, technology platform, reservation systems, pricing tools, and operational standards.

This model is attractive because it generates recurring income with relatively lower operating costs.

Hotel Management Fees

Some hotel owners prefer OYO to manage day-to-day hotel operations.

For these properties, OYO oversees operational activities such as pricing, guest experience, housekeeping standards, and overall hotel management while charging management fees for these services.

Vacation Homes

OYO has expanded beyond hotels into the vacation rental segment through brands such as Belvilla and DanCenter.

These businesses generate revenue from holiday home bookings across several European markets, giving OYO exposure to leisure travel and seasonal tourism.

Motel 6 and Studio 6 Royalties

Following the acquisition of Motel 6 and Studio 6, OYO has added an entirely new revenue stream.

Unlike traditional revenue-sharing agreements, these brands generate franchise royalty income from franchise operators across North America.

Royalty income is generally more stable and predictable because earnings are based on franchise agreements rather than direct hotel operations.

Subscription and Listing Services

Property owners can also subscribe to OYO's digital platforms and listing services.

These subscriptions provide an additional recurring revenue stream while helping property owners improve their online visibility and bookings.

Value-Added Services

Beyond accommodation, OYO earns income from several hospitality-related services including food and beverages, housekeeping support, workspaces, payment solutions, insurance offerings, and other value-added services.

These additional services increase customer engagement while improving revenue diversification.

Global Presence and Brand Portfolio

Although OYO remains widely recognized for affordable hotels in India, the company today operates a far more diversified global portfolio.

Its brands include:

OYO

Hotel O

Townhouse

Sunday

Belvilla

DanCenter

Motel 6

Studio 6

This broader portfolio allows the company to cater to different customer segments, including budget travelers, premium hospitality customers, vacation home users, and long-stay guests.

The company now derives revenue from multiple international markets, reducing its dependence on India alone. Following the Motel 6 acquisition, North America has become one of OYO's most important growth markets, strengthening its global presence and expanding its recurring franchise income.

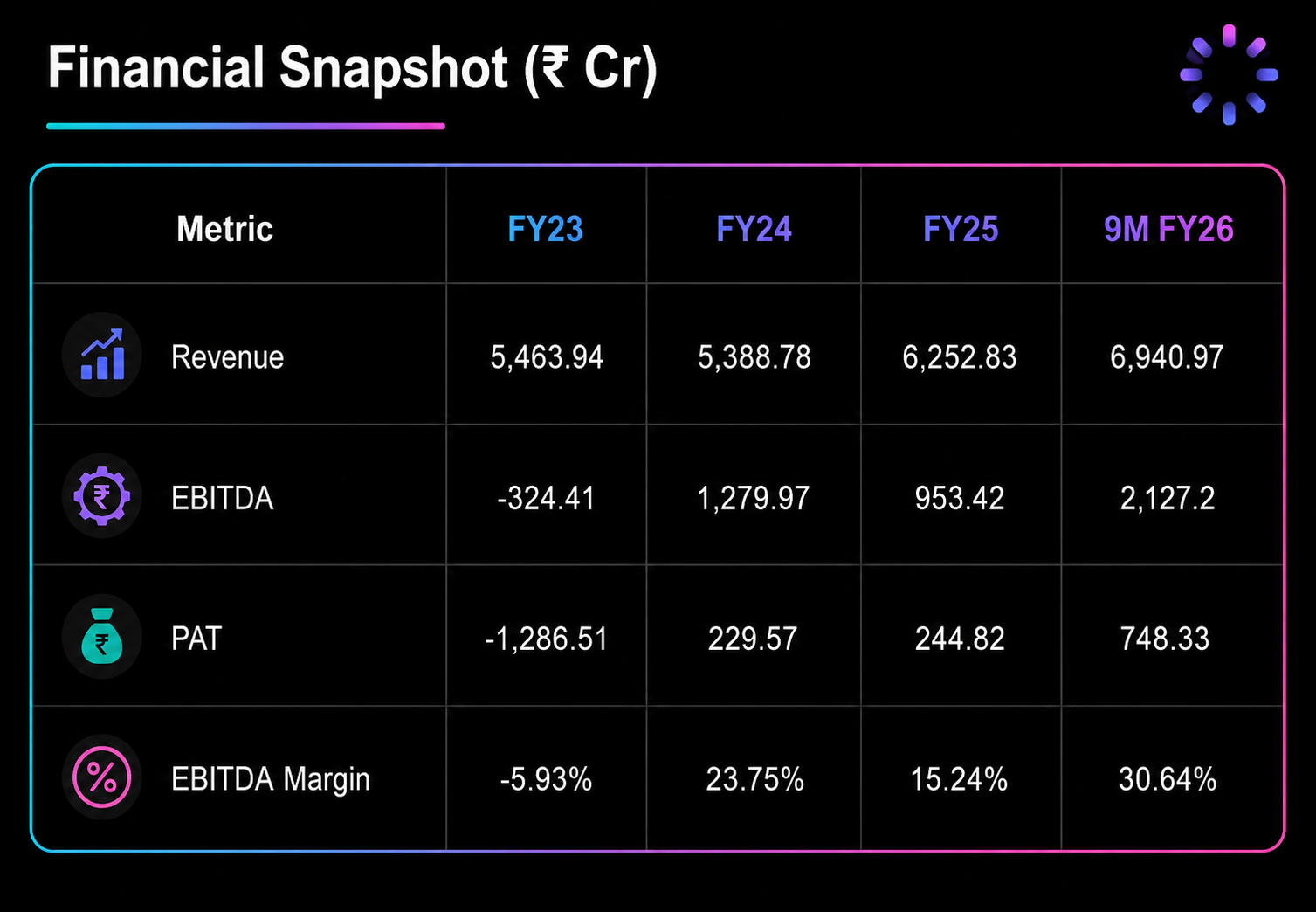

Understanding OYO's Financial Performance

One of the biggest reasons OYO's latest IPO filing has attracted attention is its financial turnaround. The company, which once faced criticism for prioritizing rapid expansion over profitability, has shown significant improvement in its operating performance over the last few years.

Instead of focusing solely on adding more hotels, OYO has shifted towards improving margins, expanding franchise-led operations, increasing royalty income, and maintaining tighter cost control.

Revenue Growth

OYO's revenue remained relatively stable during FY23 and FY24 before witnessing strong growth in FY25 and the first nine months of FY26.

The improvement reflects higher occupancy across key markets, better monetization of partner properties, expansion of international operations, and contributions from newly acquired businesses such as Motel 6.

The company is no longer relying on one geography or one business segment, making its revenue base more diversified than before.

EBITDA Performance

Perhaps the biggest change has been at the operating profit level.

After reporting negative EBITDA in FY23, OYO turned EBITDA positive in FY24 and has continued to generate healthy operating profits. The improvement indicates that the company is earning more from each additional booking while keeping operating expenses under better control.

Higher-margin businesses such as franchise operations and royalty income have also contributed to stronger profitability.

Profit After Tax (PAT)

The company has also moved from significant losses to sustained profitability.

OYO reported a loss in FY23 but returned to profit in FY24, improved further in FY25, and recorded a sharp increase in profit during the first nine months of FY26.

This turnaround suggests that the business is beginning to convert operational improvements into net earnings, strengthening investor confidence ahead of the IPO.

Margin Improvement

Another encouraging trend is the expansion in EBITDA margins.

Improving margins indicate that the company is becoming more efficient in generating profits from its revenue. Rather than chasing growth at any cost, OYO now appears focused on profitable and sustainable expansion.

Overall, OYO's financial performance reflects a shift from an aggressive startup mindset to a more disciplined hospitality platform with stronger operating leverage.

Why the Motel 6 Acquisition Matters

One of the biggest strategic developments for OYO has been the acquisition of Motel 6 and Studio 6, two well-established economy hotel brands in North America.

This acquisition goes beyond simply adding more hotel rooms. It fundamentally changes OYO's business mix and geographic exposure.

Earlier, OYO's business was largely dependent on revenue-sharing arrangements with hotel owners. Motel 6 introduces a franchise-driven model where OYO earns royalty income from franchise operators.

This is important because royalty income is generally more predictable and less dependent on day-to-day hotel occupancy. As a result, it provides a steadier source of earnings compared to traditional aggregation models.

The acquisition also strengthens OYO's position in the United States, one of the world's largest hospitality markets.

Another notable change is OYO's geographical revenue mix.

In FY23, India contributed over one-fourth of the company's revenue. By the first nine months of FY26, the share from India had declined to around 16%, while the United States contributed more than 27% of revenue.

This demonstrates that OYO has evolved into a genuinely global hospitality business rather than one primarily dependent on the Indian market.

Why is OYO Raising ₹6,650 Crore?

Unlike many technology startups that raise fresh capital primarily to fund aggressive expansion, OYO's stated objective is more conservative.

A significant portion of the IPO proceeds will be used to repay or prepay existing borrowings.

Reducing debt can lower interest expenses, improve profitability, and strengthen the company's balance sheet. A healthier financial position also gives the company greater flexibility to invest in future growth opportunities.

The remaining funds will be allocated towards general corporate purposes, supporting long-term business expansion and operational requirements.

This indicates that the IPO is not just about raising growth capital but also about creating a stronger financial foundation.

Investment Positives

1. Proven Turnaround

The company has moved from heavy losses to profitability while improving operating margins, demonstrating greater financial discipline.

2. Asset-Light Business Model

Since OYO generally does not own hotel properties, it requires comparatively lower capital expenditure to expand into new markets.

3. Diversified Revenue Sources

Revenue now comes from hotel partnerships, franchise fees, management services, vacation rentals, subscriptions, royalty income, and value-added hospitality services.

This reduces dependence on any single business segment.

4. Global Presence

Operations across more than 35 countries help diversify revenue and reduce concentration risk.

International brands such as Motel 6, Studio 6, Belvilla, and DanCenter further strengthen OYO's global footprint.

5. Stronger Focus on Profitability

The company's strategy has shifted from rapid expansion to improving margins, optimizing partner quality, and generating sustainable earnings.

Risks Investors Should Consider

No IPO is without risks, and OYO is no exception.

Dependence on Hotel Partners

Since OYO does not own most of the properties listed on its platform, maintaining strong relationships with hotel owners remains critical.

If partners leave the platform or service quality declines, customer satisfaction and bookings may be affected.

Highly Competitive Industry

OYO competes with hotel chains, online travel agencies, vacation rental platforms, and regional hospitality brands.

Maintaining market share requires continuous investment in technology, pricing, and customer experience.

Economic Slowdowns

Travel demand is closely linked to economic conditions.

Any slowdown, pandemic, geopolitical event, or decline in tourism could negatively impact occupancy and bookings.

International Operations

With business spread across multiple countries, OYO also faces regulatory, currency, taxation, and integration risks.

Managing operations across diverse markets requires consistent execution.

Final Thoughts

OYO's latest IPO represents a different company from the one investors saw a few years ago.

Rather than pursuing expansion at any cost, the company is now focused on profitable growth, stronger operating margins, diversified revenue streams, and international expansion.

The acquisition of Motel 6 has strengthened its North American presence while introducing a more predictable royalty-based income stream. Combined with improving financial performance and plans to reduce debt through the IPO, OYO appears better positioned than during its earlier listing attempt.

That said, investors should continue to monitor execution risks, competitive pressures, and the company's ability to sustain profitability over the long term.

The OYO IPO is not merely a comeback story—it is a test of whether one of India's best-known startup brands can successfully transition into a mature, globally diversified hospitality company.

To compare companies, documents, and availability explore unlisted companies on Precize. For ongoing IPO and private-market updates, browse the Precize blog. Stay updated with unlisted companies through our Precize Community. If this article was useful, you can share it with other investors through the Precize Referral Program.

Frequently Asked Questions (FAQs)

1. What is the OYO IPO?

The OYO IPO is the proposed public offering of Oravel Stays Limited, comprising a fresh issue of equity shares worth ₹6,650 crore.

2. What will OYO use the IPO proceeds for?

The company intends to use a significant portion of the proceeds to repay or prepay borrowings, with the balance allocated toward general corporate purposes.

3. Does OYO own its hotels?

No. OYO primarily operates an asset-light business model by partnering with independent hotel owners.

4. How does OYO generate revenue?

Its revenue comes from hotel revenue sharing, franchise fees, management fees, vacation homes, royalty income from Motel

6 and Studio 6, subscriptions, listings, and value-added hospitality services.

5. Why is the Motel 6 acquisition important?

The acquisition strengthens OYO's presence in North America while adding recurring franchise royalty income, making earnings more diversified and predictable.

6. Is OYO profitable?

According to its DRHP, OYO has transitioned from losses in FY23 to profitability in FY24 and FY25, with further improvement during the first nine months of FY26.

7. What are the biggest risks for OYO?

Major risks include dependence on hotel partners, intense industry competition, fluctuations in travel demand, and challenges associated with international operations.

8. Is OYO only an Indian company?

No. OYO operates across more than 35 countries and has significant operations in Europe and North America in addition to India.

Disclaimer: This article is for informational purposes only and should not be considered as investment advice. Investing in unlisted shares carries risks including illiquidity and potential loss of capital. Please consult with a qualified financial advisor before making investment decisions. Precize is not a stock exchange and is not authorized by any capital markets regulator.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved