Mutual Fund Lock-In Periods: Essential Investor Insights Before You Invest

Have you ever wondered why some mutual funds or financial instruments don’t allow you to access your money for a certain period? That period is called a lock-in period, and understanding it can make a big difference in managing your finances wisely.

In this blog, we will explain what a lock-in period is, how it works across different instruments, why it matters, and how it affects your financial choices. You will also learn tips to choose instruments while tracking lock-in periods effectively.

Keep scrolling!

Quick Summary

Lock-in period is the minimum time your money stays in a financial product before it can be withdrawn.

It helps maintain stability, prevents impulsive withdrawals, and supports disciplined financial decisions.

Different products have different lock-in periods, from 3 years in ELSS to 15 years in PPF.

Being aware of lock-in periods helps plan timelines, manage liquidity, and align with tax benefits.

What is a Lock-In Period?

A lock-in period is a specific time frame during which you cannot withdraw your money from a financial instrument. In mutual funds, certain types come with a fixed lock-in period to ensure that the funds remain untouched for a set duration. This period can vary depending on the type of fund or scheme, and it is usually clearly mentioned at the time of purchasing the instrument.

Knowing what a lock-in period means is just the first step, understanding how it applies across different options helps you plan your finances better.

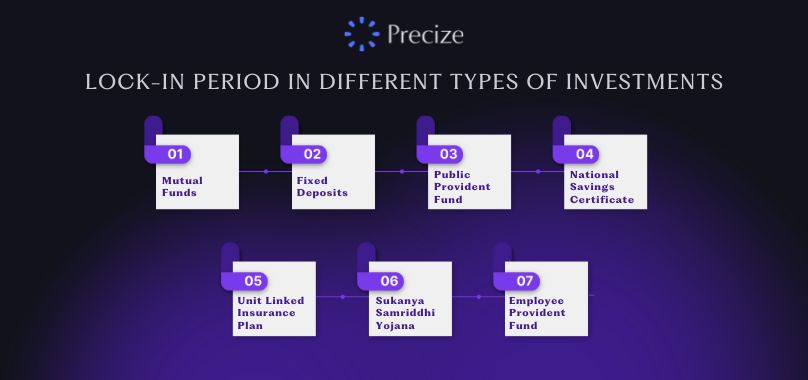

Lock-In Period in Different Types of Investments

The lock-in period varies depending on the type of financial option, and understanding these differences helps you know when your money becomes accessible.

Mutual Funds (ELSS)

Equity Linked Savings Schemes have one of the shortest lock-in periods for tax-saving options, fixed at 3 years. You cannot withdraw before this period, but after 3 years, the units can be accessed freely.

Fixed Deposits (Tax-Saving FD)

Special tax-saving FDs from banks come with a 5-year lock-in. Early withdrawal is not allowed, and the amount becomes accessible only after 5 years.

Public Provident Fund (PPF)

This long-term option has a 15-year lock-in. Partial withdrawals are allowed from the 7th year onwards, but the full amount can only be withdrawn after 15 years.

National Savings Certificate (NSC)

NSCs have a fixed lock-in of 5 years. The money remains unavailable until the period ends.

Unit Linked Insurance Plan (ULIP)

ULIPs come with a minimum lock-in of 5 years. Withdrawals are not permitted during this time, but partial withdrawals may be allowed once the period is over.

Sukanya Samriddhi Yojana

The lock-in lasts until the girl turns 21. Partial withdrawal of up to 50% is possible after she turns 18, but the account matures fully at 21.

Employee Provident Fund (EPF)

The EPF balance is generally locked until retirement. However, partial withdrawals are permitted under specific conditions such as buying a house, marriage, or medical needs.

Being aware of these durations helps you see the benefits and role of lock-in periods in financial planning.

Why Lock-In Periods are Important

Understanding why lock-in periods matter helps you see how they protect your funds and support better financial planning.

Maintains Stability: The lock-in period ensures your mutual fund units are held for a minimum duration, helping maintain stability in the fund’s overall performance.

Prevents Impulsive Withdrawals: It stops you from making sudden decisions when market conditions change, giving the fund time to perform without disruption.

Supports Fund Management: Lock-in periods give fund managers the necessary time to manage the portfolio efficiently, without the pressure of frequent withdrawals.

Encourages Discipline: This period discourages short-term trading and promotes a more disciplined approach to holding mutual fund units.

Linked to Tax Benefits: For certain mutual funds, the lock-in period is connected to tax benefits under Indian laws, making it important for financial planning.

Reduces Liquidity Pressure: It protects the fund from sudden liquidity challenges that can occur if many units are withdrawn at the same time.

Allows Thoughtful Decisions: After the lock-in period ends, you have the chance to review your holdings calmly and decide whether to continue holding or redeem, avoiding rushed choices.

With the benefits of lock-in periods clear, let’s explore how they shape the way your funds perform over time.

How Lock-In Period Affects Your Financial Planning

The lock-in period affects your financial planning and fund stability in several ways. Here are the pointers you should be aware of:

Minimum Holding Time: The lock-in period is the required duration you must keep your money in a mutual fund before you can withdraw or sell it.

Applies to Specific Funds: It is mostly relevant for instruments like ELSS, closed-ended funds, and some fixed maturity plans.

Encourages Discipline: This restriction prevents impulsive decisions, especially during market fluctuations, and promotes financial discipline.

Supports Fund Management: Lock-in periods provide stability, allowing fund managers to focus on long-term performance without frequent redemption pressure.

Options After Completion: Once the lock-in period ends, you can choose to retain your units, move them, or redeem them based on your needs.

Tax Implications: Some periods, like the 3-year lock-in for ELSS, also align with Indian tax rules, making certain tax benefits available only after the period ends.

Once you understand how the lock-in period impacts your planning, the next step is to choose options that fit your timeline and goals.

Tips to Choose Investments Considering Lock-In Period

To make the right choices, consider how the lock-in period fits with your financial timeline and needs. The following are key points to keep in mind:

Check Duration First: Know the lock-in period before selecting any mutual fund or financial product, as this is the time when withdrawals are not allowed.

Match Your Timeline: Pick options with a lock-in period that aligns with your financial timeline to avoid liquidity issues during emergencies.

Shorter Lock-In for Quick Access: Consider products with shorter lock-in periods if you may need access to your money in a few years.

Longer Lock-In for Stability: Longer lock-in periods can provide stability and help avoid rushed decisions during market fluctuations.

Understand Fund Type: Review the type of product carefully, as some, like ELSS, have a mandatory three-year lock-in, while ULIPs may require five years.

Balance Flexibility: Maintain a mix of options with and without lock-in periods to meet both short-term and longer-term needs.

SIP Considerations: Each installment in Systematic Investment Plans (SIPs) may have its own lock-in period starting from its individual investment date.

Check Rules and Penalties: Be aware of exit rules, charges, or penalties that may apply for early withdrawal after the lock-in period.

Emergency Planning: Keep a separate emergency fund to avoid breaking locked-in products prematurely.

Reassess After Lock-In: Once the lock-in period ends, review your financial situation and options before making any changes.

Conclusion

As discussed, understanding the lock-in period allows you to plan your financial decisions with clarity and stability. It helps maintain discipline, prevents sudden withdrawals, and aligns with important tax benefits under Indian laws. Being aware of lock-in periods across different products ensures better timing and management of your holdings.

Platforms like Precize facilitate access to leading private companies, allowing you to buy and sell unlisted shares and pre-IPO shares. They also provide global finance opportunities, helping diversify your portfolio with alternative fixed-income options.

Reserve access to explore these opportunities!

FAQs

What should I do when the lock-in period expires?

Once the lock-in period ends, you can review the fund’s performance and decide your next step. You may redeem some or all units, switch to another fund if your goals have changed, or keep the units invested to stay on track with your objectives.

How can I check the lock-in period of a mutual fund?

You can check the lock-in period on the fund house’s official website, in the Scheme Information Document (SID) or Key Information Memorandum (KIM), or on trusted financial portals. If the information is not available, the fund’s customer care can provide details.

Do all mutual funds have a lock-in period?

No. Only specific types, such as tax-saving ELSS funds, have a fixed lock-in, usually three years. Most open-ended mutual funds have no lock-in and allow redemption anytime.

Disclaimer

This blog is meant to provide general information about lock-in periods and related financial topics. Readers should consult with a professional before making any financial decisions. The author or platform is not responsible for any outcomes based on the information shared in this content.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved