Fractal Analytics Valuation: A Complete Breakdown

Fractal Analytics has become one of the most closely watched names in India’s AI and analytics space, and its public-market move has drawn attention to one question: how is the company being valued across different stages? With news reports citing a potential US$3.5 billion reference point and a recent private transaction placing the Fractal Analytics valuation near US$2.44 billion, many readers want clarity on what these numbers mean, how they differ, and which one matters during the IPO phase.

In this guide, you’ll find a clear, structured explanation that helps you understand these valuation checkpoints without speculation.

Key Takeaways

Primary Valuation Checkpoints: Fractal’s valuation has moved through verified milestones, including its DRHP filing, ₹4,900 crore IPO structure, FY25 financial disclosures, and the US$2.44B private secondary transaction.

Different Valuation Frameworks: Valuation shifts across 4 stages, secondary transactions, filing-based assessments, IPO pricing, and post-listing trading, each relying on different disclosures and equity structures.

How the $2.44B Figure Fits: The US$2.44B valuation represents a private negotiated transaction and serves as a historical reference, not a predictor of IPO or listing-day valuation.

Scenario Models Behind 2025 Estimates: Analysts examine pre-offer equity, post-offer dilution, revenue mix, subsidiary outcomes, and balance-sheet structure to build non-speculative valuation scenarios.

Factors That Influence Interpretation: Revenue scale, margin patterns, client concentration, subsidiary performance, and capital structure shape how market participants may interpret valuation once full disclosures are reviewed.

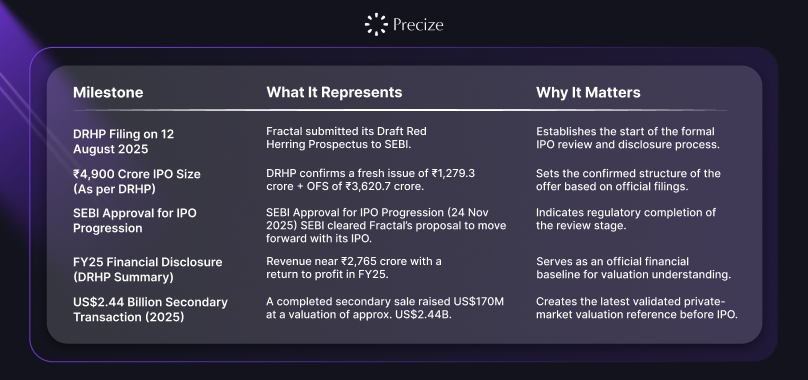

Quick Facts: Fractal Analytics Valuation Milestones So Far

Fractal Analytics’ valuation has moved through several clear checkpoints across private transactions and regulatory activity. These events form the reference points that analysts, institutions, and private-market participants rely on when discussing how the company may be valued in 2025.

These milestones set the backdrop for how valuation is interpreted across different stages, which makes it useful to break down what each valuation type actually represents in practice.

Fractal Analytics Valuation Basics: What Different Types Mean

A company’s valuation transforms as it moves through private transactions, regulatory filings, and public-market pricing. Each stage uses a different calculation method and relies on a different information set. For Fractal Analytics, these stages are now easier to track because the company filed its Draft Red Herring Prospectus (DRHP) with SEBI on 12 August 2025 and received SEBI approval on 18 November 2025, establishing the official disclosure baseline.

Here is a detailed breakdown built around Indian regulatory practices and how valuation is actually computed at each stage.

Secondary Valuation: Calculated From a Share-Transfer Price

A secondary valuation is derived directly from the per-share transfer price when existing shareholders sell equity to a new party.

How the valuation is computed:

Take the agreed per-share transfer price

Multiply it by the company’s fully diluted share count at that time

The result becomes the implied private-market valuation

Why this matters technically:

Only existing shares change hands

The valuation reflects the price insiders accepted

Fully diluted share count includes ESOPs, preference conversions, and outstanding commitments

Example structure (illustrative, not using repeated numbers): If a buyer acquires shares at ₹X during a secondary transfer, valuation = ₹X × total diluted shares.

Key insight: Secondary valuation reflects negotiated pricing inside a closed transaction, not a market-wide bid.

Filing-Based View: Built From SEBI-Mandated Disclosures

A filing-based valuation is not a “number” inside the DRHP. Instead, it is constructed by analysts using information that SEBI requires companies to disclose.

What this view includes:

Total equity before the offer

Total equity after conversion of CCPS and ESOPs

Fresh issue size

OFS volume

Segment-level performance

Revenue concentration by customer

Debt positions

Subsidiary-level results

Auditor observations

Cash-flow structure

Geographical contribution

Why this matters technically:

These inputs allow analysts to model scenarios

No price is set yet

This is the only point in the process where audited information and operational detail are available before a public offer

Key insight: A filing-driven view is built entirely from SEBI-reviewed disclosures and forms the baseline for subsequent valuation work.

IPO Valuation: Determined Through the Book-Building Framework

IPO valuation in India is calculated only after the price band is released.

It comes from two components:

A. Issue Price (Final Offer Price)

Set after analysing:

Institutional demand

Investor bids inside the price band

Allocation rules under SEBI guidelines

Market conditions during the bidding window

B. Total Outstanding Equity After Fresh Issue

This includes:

Pre-offer equity

Newly issued shares from the fresh issue

Converted CCPS, if any

ESOP pool adjustments

Formula: IPO Valuation = Final Offer Price × Total Outstanding Equity After Fresh Issue

Key insight: This is the first valuation directly shaped by public demand rather than private negotiation.

Post-Listing Valuation: Determined by Live Trading

This valuation is built from:

Real-time market trades

Opening auction on listing day

Buy/sell quantity at each price level

Institutional participation on listing day

Retail trading volume

Free-float available to the public

Formula: Post-Listing Valuation = Market Price × Total Outstanding Shares

Why it matters technically:

It reflects the first broad-market consensus

It may diverge sharply from the IPO valuation, depending on trading interest

It becomes the reference point for future institutional entry

Key insight: Post-listing valuation is the only form driven entirely by market activity without influence from negotiated or regulatory processes.

With the milestone events mapped out, the natural progression is to see how each valuation type is defined and calculated across Fractal’s funding and regulatory stages.

If you want to deepen your market knowledge before reviewing upcoming offers, take a look at what is IPO grading?

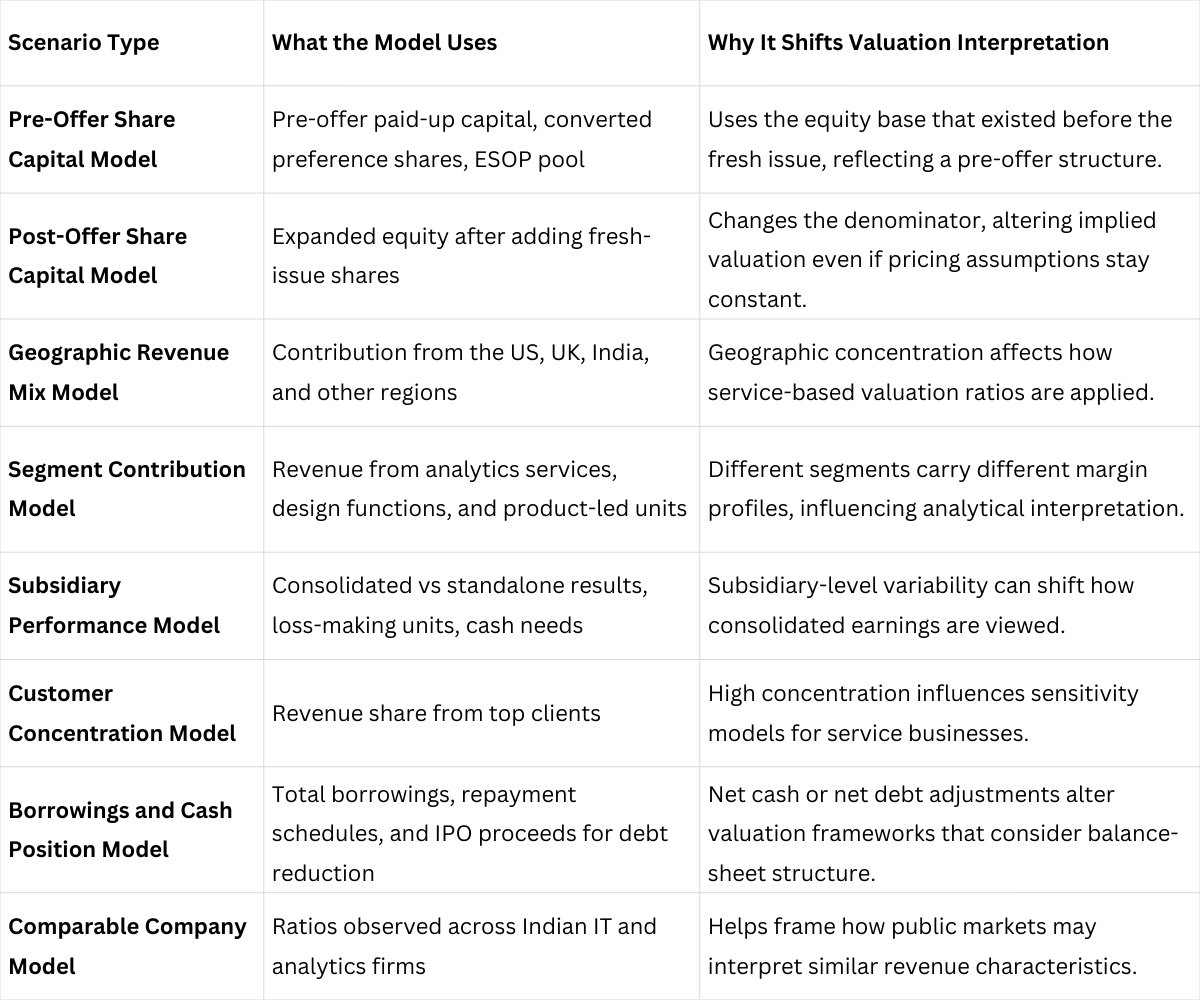

Scenario Models for Fractal Analytics Valuation (Core: Non-Advisory, Analytical)

Valuation outcomes shift depending on which inputs analysts use after a company files its DRHP. Since no official price band is available yet, scenario modelling helps clarify how different elements of the filing influence valuation. These are analytical structures, not forecasts.

Once the scenario structures are clear, the focus shifts to how valuation frameworks are compared across similar companies in the analytics and AI-services segment.

If you're comparing valuation signals across upcoming offers, you may find added clarity by reviewing structured methods discussed in IPO investment strategies: maximizing returns with informed decisions

Peers and Comparable Multiples: Cautious Benchmarking

Comparing an analytics and AI-services company during the IPO stage requires careful classification because Indian and global markets group such firms based on delivery structure, contract depth, and revenue patterns rather than broad sector labels.

Public analysts typically create peer brackets using DRHP disclosures to avoid mismatching business models that may look similar on the surface but differ materially in execution and earnings.

Revenue Composition–Based Peer Grouping: Benchmarking begins with how revenue is split across analytics services, engineering work, design capabilities, and platform-led functions. A company with a higher share of recurring analytics programs falls into a different analytical bracket than firms driven mostly by short-cycle engineering assignments.

Engagement Depth and Renewal Patterns: Peers are grouped based on the length and nature of client engagements, multi-year analytics mandates, managed-services contracts, and continuous decision-support programs are benchmarked separately from project-based or outcome-linked assignments.

Delivery-Center Cost Architecture: Public-market analysts consider delivery location mix (India vs. outside India), average employee cost, and utilisation patterns. This allows comparability with firms that follow similar talent pyramids rather than those operating with materially different cost structures.

Geographic Revenue Dependence: Companies generating a high share of revenue from the United States are usually compared within a bracket that reflects North America-led demand cycles, while firms with a broader regional distribution are grouped differently due to varying macro cycles.

Operational Cash Generation and Balance-Sheet Structure: Peer comparison also considers whether earnings translate into cash consistently, how much working capital the business requires, and how debt or cash reserves influence valuation ratios that depend on capital structure.

These milestones set the stage for a clearer view of how valuation frameworks operate at different points in Fractal Analytics’ journey.

What Fractal Analytics Valuation Means for Pre-IPO and Unlisted Shareholders and Platforms

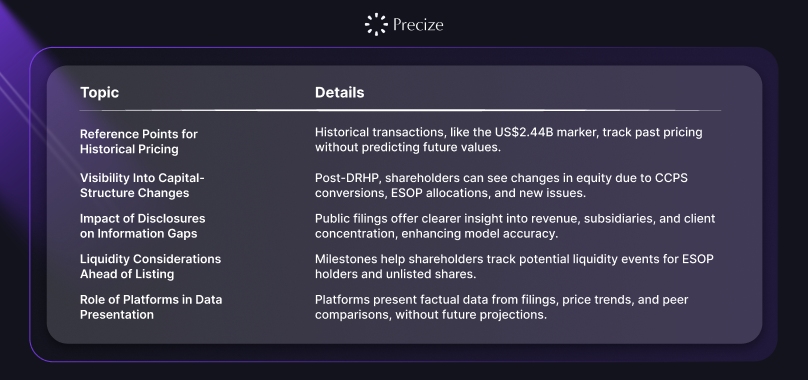

Valuation milestones influence how unlisted shares are viewed in private-market settings, but they do not dictate future pricing once a company enters the public-offer stage. This section explains how different stakeholders, employees, early shareholders, and private-market platforms interpret valuation updates using publicly available information without treating them as signals for future outcomes.

Reference Points for Historical Pricing: Earlier secondary transactions, including the US$2.44B marker, act as chronological checkpoints that help shareholders understand how the company has been priced over time, without implying where future pricing may land.

Visibility Into Capital-Structure Changes: Once the DRHP is filed, shareholders can see how CCPS conversions, ESOP allocations, and fresh-issue components modify the total equity base, which is relevant when tracking how ownership percentages grow.

Impact of Disclosures on Information Gaps: Public filings provide updated data on revenue distribution, subsidiary outcomes, and client concentration, giving unlisted shareholders clearer visibility into factors that shape analytical models used by institutions.

Liquidity Considerations Ahead of Listing: For individuals holding ESOPs or long-standing unlisted shares, valuation milestones clarify where the company stands in its listing process, helping them track when liquidity windows may become accessible through regulated channels.

Role of Platforms in Data Presentation: Private-market platforms use official filings to present structured financial information, historical price movements, and peer context, giving users a factual overview without projecting future values or offering directional guidance.

If you want to review opportunities outside traditional listings, you can refer to our detailed explainer on investing in private market startups online.

Conclusion

Fractal Analytics’ valuation story reflects how private transactions, regulatory disclosures, and IPO structures create distinct reference points rather than a single definitive number. Each checkpoint, from the US$2.44 billion secondary sale to the ₹4,900 crore offer outlined in the DRHP, adds clarity on how the company has been assessed at different stages.

This provides a more informed foundation for understanding how valuation frameworks may be interpreted as the public offer process progresses, without assuming the final market outcome.

If you want to evaluate more businesses at the pre-IPO stage, Precize helps you go beyond surface-level information with structured data, research-backed insights, and access to select unlisted opportunities. This allows you to analyse companies earlier in their growth journey, well before they enter public markets.

Reserve your access on Precize to explore early-stage opportunities with greater clarity.

Disclaimer

The information in this blog is based on publicly available disclosures, regulatory filings, and credible news sources. It is intended for educational use and should not be treated as financial, legal, or investment advice. Market conditions and company-specific details may change, and readers should refer to official documents and professional guidance for any financial decisions.

FAQs

What stage is Fractal Analytics in after announcing its IPO date process?

The company has completed key regulatory steps, including filing its DRHP and securing SEBI approval. The final Fractal Analytics IPO date will be confirmed once the price band and subscription schedule are published in the RHP.

How does the recent secondary sale influence the Fractal Analytics IPO valuation?

The 2025 secondary transaction valued the company at approximately US$2.44 billion. This acts as a historical checkpoint, but the Fractal Analytics IPO valuation will depend on the price band and post-offer share count disclosed closer to the listing.

Why are multiple valuation references seen in discussions around Fractal Analytics' valuation 2025?

Different figures appear because they come from different events, the US$2.44 billion private sale, DRHP-linked assumptions, and media-quoted expectations. This is why searches for Fractal Analytics valuation 2025 show varied numbers.

Does the DRHP provide enough information to understand the Fractal Analytics valuation?

Yes. The DRHP includes revenue trends, OFS structure, fresh-issue size, and key operational data. These inputs allow analysts to interpret the Fractal Analytics valuation using publicly reviewed information.

Can the Fractal Analytics IPO valuation be compared directly with previous private valuations?

Not directly. Private transactions use the pre-offer equity base, while IPO valuation is computed using the post-offer share count. This is why comparing private numbers with the final Fractal Analytics IPO valuation requires adjustments.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved