Factoring vs. Forfaiting: A Guide for Exporters and Importers

Managing cash flow is one of the most persistent challenges in global trade. In fact, 80% to 90% of world trade relies on some form of trade finance, such as trade credit, insurance, and guarantees, mostly to address short-term liquidity needs and mitigate the risk of non-payment.

With payments often delayed or stretched over long periods, businesses are forced to find ways to accelerate cash flow without taking on additional risk.

This is where factoring and forfaiting come into play. Both methods allow businesses to sell their receivables for immediate cash, but they differ in structure, terms, and risk distribution.

In this blog, we’ll break down these two trade finance options to help you determine the best fit for your business needs.

Key Takeaways

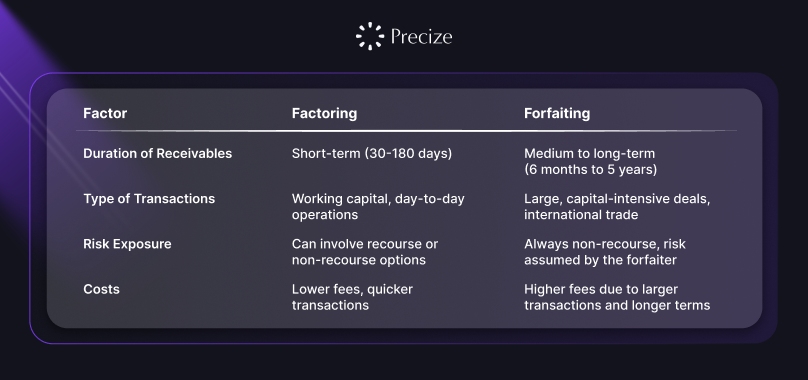

Factoring is best for businesses needing quick liquidity from short-term receivables (30-180 days) and is ideal for smaller transactions with frequent sales.

Forfaiting is suited for large, long-term transactions (6 months to 5 years) and is commonly used in international trade to transfer the risk of non-payment to the forfaiter.

Factoring can involve recourse or non-recourse options, with businesses potentially retaining some risk, whereas forfaiting is always non-recourse, making it more secure for exporters.

Factoring typically has lower fees and faster transactions, while forfaiting carries higher fees due to larger, long-term deals and the assumption of greater risk by the forfaiter.

What Is Factoring and How Does It Work?

Factoring is a financing solution in which businesses sell their receivables (outstanding invoices) to a third party, called a factor, in exchange for immediate cash.

This allows companies to improve their cash flow and continue operations without waiting for customers to settle their invoices, which can often take 30, 60, or even 90 days.

Instead of waiting for payment, they receive a percentage of the invoice amount upfront, minus a fee for the factor’s services. Key features of factoring include:

1. Recourse vs. Non-Recourse Factoring:

Recourse Factoring: The business remains liable if the customer fails to pay the invoice.

Non-Recourse Factoring: The factor assumes the risk, meaning the business is not liable if the customer defaults.

2. Short-Term Receivables:

Factoring is typically used for receivables with payment terms of 30 to 90 days, making it ideal for short-term liquidity needs.

3. Small to Medium Businesses:

Factoring is well-suited for businesses with frequent, smaller transactions that need fast cash flow without taking on debt.

Example: A small business sells ₹500,000 in receivables to a factor for ₹450,000. The factor collects the full ₹500,000 from the customer, keeping the difference as their fee.

Benefits of Factoring:

Quick Access to Cash: By selling receivables, businesses can instantly access the funds they need to keep operations running smoothly without waiting for customer payments.

Outsourced Credit Management: Factoring often includes services like credit risk assessment and collections, which can save businesses time and resources.

Reduced Risk of Non-Payment: In non-recourse factoring, the business is protected against customer non-payment, with the financial risk transferred to the factor.

Also Read: Common Methods of Payment in International Trade

Next, we’ll explore forfaiting, another important trade finance option that offers distinct benefits for businesses, especially in international trade.

What Is Forfaiting and How Does It Work?

Forfaiting is a trade finance solution in which a business sells its medium- to long-term receivables (typically associated with large transactions) to a forfaiter in exchange for immediate cash.

Unlike factoring, forfaiting is usually used in international trade, where receivables have longer payment terms, typically 6 months to 5 years. By selling these receivables, exporters can remove the risk of non-payment and gain immediate liquidity.

Key Features of Forfaiting:

Non-Recourse Agreement: In forfaiting, the forfaiter assumes the risk of non-payment, thereby protecting the exporter from the buyer's default.

Medium to Long-Term Receivables: Forfaiting is suited for receivables with longer payment terms (6 months to several years), commonly used in large export transactions like machinery or capital goods.

Used for Large Transactions: Ideal for businesses involved in international trade or capital-intensive deals requiring long-term financing.

Example: A manufacturer in India exports machinery worth ₹5,00,000 to a buyer in another country with a 12-month payment term.

The exporter sells the receivable to a forfaiter for ₹4,80,000, receiving immediate cash and transferring the non-payment risk to the forfaiter.

Benefits:

Immediate cash flow for long-term receivables.

Non-recourse financing which eliminates the risk of non-payment.

Enables exporters to focus on production and growth without worrying about customer payments.

Also Read: Different Types and Benefits of Factoring in Financial Services

Understanding the differences in risk distribution between factoring and forfaiting is crucial for determining which option provides the best protection for your business.

How Does Risk Distribution Differ Between Factoring and Forfaiting?

Risk distribution is a key factor when deciding between factoring and forfaiting. Both methods provide businesses with immediate cash by selling receivables, but they handle the risk of non-payment differently.

Understanding these differences is crucial for businesses, particularly exporters, when deciding which option provides the best protection and financial stability.

Factoring: Risk Retention vs. Transfer

In factoring, the seller may still bear some risk, depending on the type of agreement chosen.

Recourse Factoring: The business remains responsible if the customer defaults on the invoice. If the buyer doesn’t pay, the business must repay the factor, making this a riskier option for the seller.

Non-Recourse Factoring: The factor assumes the risk of non-payment, meaning if the customer defaults, the business is not liable. However, non-recourse factoring often comes with higher fees because the factor assumes the credit risk.

Forfaiting: Full Risk Transfer

In forfaiting, the risk is always non-recourse. The forfaiter assumes full responsibility for the buyer’s default, meaning the exporter is not liable for non-payment.

This makes forfaiting particularly attractive for exporters involved in international trade, as it removes the risk of foreign buyers defaulting on large transactions.

Example:

Imagine an exporter in India selling machinery worth ₹50,00,000 to a buyer in Europe with a 12-month payment term. If the exporter uses factoring, they may still be liable for the payment if the buyer defaults (in recourse factoring).

However, with forfaiting, the exporter sells the receivable to the forfaiter and transfers all the default risk, meaning they’re protected against the buyer’s non-payment.

Also Read: Boost Business Funds with Permanent Working Capital

Now that we've discussed the basics, let’s compare factoring and forfaiting to highlight their key differences and help you better evaluate which method suits your business needs.

What Are the Key Differences Between Factoring and Forfaiting?

Factoring and forfaiting are both trade finance methods that allow businesses to convert receivables into immediate cash. Still, they differ significantly in terms of duration, transaction size, risk exposure, and cost structure.

Understanding these differences is crucial for companies to choose the right option based on their business needs and financial goals.

At Precize, we offer innovative solutions for managing your pre-IPO shares and global trade finance investments. Whether you're looking to invest in high-growth pre-IPO companies or seeking short-term returns through global trade finance, our platform makes it easy to get started with as little as ₹10,000.

Which Option Is Right for Your Business?

Choosing between factoring and forfaiting depends on your business size, the nature of your transactions, and your liquidity needs. Here’s a breakdown of which option suits different types of businesses.

For Short-Term Needs: Factoring is the Best Choice

If your business regularly needs cash quickly and deals with smaller transactions, factoring is likely the better option. Factoring allows you to sell your short-term receivables (usually with 30-180 days payment terms) to a third party in exchange for immediate cash.

Best for Small, Frequent Sales: Ideal for businesses with lots of small transactions, like retailers or service providers.

Quick Cash: Factoring offers fast access to working capital without waiting for customers to pay.

Simple Setup: It’s easier and quicker to arrange, making it a good choice for businesses that need cash flow flexibility.

Example: A local retailer that sells goods on 30-day terms can use factoring to quickly get cash by selling those receivables, ensuring they have the liquidity to cover inventory and operating costs without delay.

For Large, Long-Term Transactions: Forfaiting Works Best

If your business deals with larger, international sales or long-term transactions, forfaiting is more suitable. With forfaiting, you sell medium- to long-term receivables (typically 6 months to 5 years) to a forfaiter, who assumes the risk of non-payment.

No Risk of Non-Payment: In forfaiting, the forfaiter takes on the risk, which makes it a good option for exporters and businesses with large contracts.

Long-Term Deals: Forfaiting works for longer receivables, which are typical in big, capital-intensive transactions.

International Trade: It’s commonly used in international business where payment terms are longer and the risk of foreign buyer defaults is higher.

Example: An Indian machinery exporter selling equipment to a foreign buyer with a 12-month payment term might prefer forfaiting.

The exporter receives immediate cash while transferring the risk of non-payment to the forfaiter, allowing them to continue business without worrying about customer defaults.

Conclusion

Factoring and forfaiting both offer solutions to address liquidity challenges, but they cater to different business needs. Factoring works best for businesses seeking immediate cash flow from short-term receivables, especially for smaller firms or transactions with frequent sales.

Forfaiting, in contrast, is better suited for larger businesses engaged in international trade or capital-intensive industries. This method offers more security, especially for exporters dealing with long payment cycles or foreign buyers with higher credit risk.

At Precize, we provide businesses with the tools to manage trade finance effectively, including pre-IPO shares and global trade finance investments. Whether you're seeking immediate cash flow or long-term financing options, we offer flexible solutions to support your growth.

Reserve access with Precize today to optimize your trade finance strategy and secure your next opportunity.

FAQs

Q: How do I decide whether to use factoring or forfaiting for my business?

A: The choice depends on the size and duration of your receivables. Use factoring if you have short-term receivables (30-180 days) and need quick access to cash. Opt for forfaiting if you are dealing with larger, longer-term international transactions where risk transfer is important.

Q: What types of businesses benefit most from factoring?

A: Small to medium-sized businesses, especially those with frequent, smaller sales (like retail or services), benefit the most from factoring. It allows them to maintain liquidity without waiting for customer payments, supporting day-to-day operations.

Q: How does forfaiting protect against international payment risk?

A: In forfaiting, the forfaiter assumes the full risk of non-payment by the buyer. This is particularly useful in international trade, where exporters often face higher risks due to longer payment terms and unfamiliar markets.

Q: What are the costs involved in factoring and forfaiting?

A: Factoring generally involves lower fees because it’s for short-term receivables and smaller transactions. Forfaiting, on the other hand, involves higher fees due to the larger amounts, longer payment terms, and the risk transferred to the forfaiter.

Q: Can factoring and forfaiting be combined for one business?

A: Yes, businesses can use both factoring and forfaiting depending on the nature of their transactions. For short-term needs, factoring can be used, while forfaiting is ideal for longer, larger contracts. Combining both allows businesses to optimize cash flow management across different transaction types.

Stay in the Loop

Join our newsletter for exclusive access to thoughtfully curated content and we promise, no spam

Company

Our Office

Office No. 1219, The Summit Business Park, Andheri Kurla Road, Andheri East, Mumbai, Maharashtra - 400093

Find us on Googlesupport@precize.in

+91 7738336457

All trademarks and logos or registered trademarks and logos found on this Site or mentioned herein belong to their respective owners and are solely used for informational and educational purposes.

The material presented in this advertisement is for informational purposes only and should not be construed as investment advice or investment availability. It is not a recommendation of, or an offer to sell or solicitation of an offer to buy, any particular unlisted share, security, strategy, or investment product. Investing in the private market and securities involves risks, including the potential loss of money, and past performance does not guarantee future results. Market trends, data interpretations, graph projections are provided for informational and illustrative purposes and may not reflect actual future performance. Nothing on this website should be construed as personalized investment advice or should not be treated as legal, financial, or any other form of advice. Precize is not liable for financial or any other form of loss incurred by the user or any affiliated party based on information provided herein.

Precize is neither a stock exchange nor does it intend to get recognized as a stock exchange under the Securities Contracts Regulation Act, 1956. Precize is not authorized by the capital markets regulator to solicit investments. The securities traded on these platforms are not traded on any regulated exchange.

The website will be updated regularly.

Copyright © 2026 - Precize - All Rights Reserved